19 ways to make extra money as a pharmacist in 2020

Updated 2/2020

The following post contains affiliate links through which YFP or its team members may receive compensation.

Within the past couple years, many pharmacists have unfortunately experienced pay cuts as multiple community pharmacy chains reduced weekly hours to be considered full-time (such as 32 hours). With this example, considering median pharmacist pay, it would result in about a $25,000 loss per year or more. That’s a big deal for anyone but especially those struggling to pay back pharmacy school loans and other debt.

Not only that, some pharmacists have experienced a job loss because of stores closing or companies downsizing.

Even if you’re fortunate and haven’t had a pay cut or lost a position, you still may be looking for ways to accelerate your financial goals, fund vacations, or just upgrade your lifestyle, etc. Obviously, you can cut and minimize your expenses up to a point, but eventually, you’ll reach a limit. This, combined with the pharmacist salary being relatively fixed in many settings, can lead you to find ways to make extra money as a pharmacist.

While there are a plethora of options to make extra money and many side jobs for pharmacists, some are not practical. Your time is important, right? With a median hourly pay around $60, doing something for less where you trade your time for money may not be the best use of your efforts unless it’s something you’re really passionate about. Other ideas such as starting a blog or podcast with the goal of eventually monetizing can work but they can take years to reach that point and take up a ton of time.

For this post, we are going to focus on some practical ways to earn some extra cash not in a year or five years from now, but this year. While most of these are focused on a pharmacy background, I have included some others as well that are relatively easy to get started and won’t necessarily take a lot of time to execute.

1. Take Extra Shifts

This is probably one of the easiest ways to earn extra money as a pharmacist if it’s available. While not likely for those working in community pharmacy, there may be some opportunities in hospitals and health systems especially when there is a temporary shortage.

One of my friends who recently switched from a community chain to a mail order specialty pharmacy was really concerned about the pay cut he was going to initially experience. However, even though the base salary was lower, he actually made more because of the ample opportunities for overtime.

2. Look for Additional Projects / Assignments

Throughout my pharmacist career, there have been several times when special projects required pharmacist intervention. Typically, these have been large volume medication changes that needed patient education either due to manufacturer backorders or formulary changes secondary to pricing changes. Because of the potential cost savings for these projects, employers can often justify overtime pay.

While these types of opportunities may not be blatantly advertised, I would encourage you to reach out to your supervisor or manager to see if there is anything available.

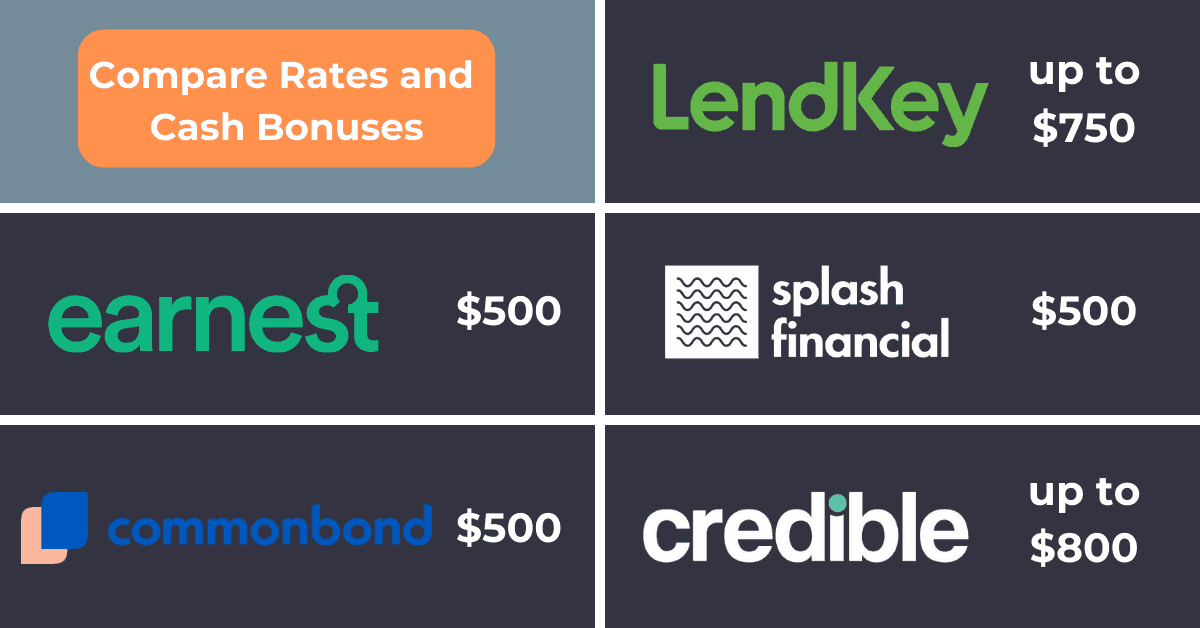

3. Refinance Student Loans…And Then Do It Again

Save money by paying less in interest each month because of a lower rate. That’s the typical reason why most people with refinance student loans. While saving money is great, why not also get paid. In a single year, my wife and I made $2,700 by refinancing our student loans multiple times. Each time we were able to get a lower interest rate through a different company and each time we were able to get a cash bonus.

Refinance companies will make money from you by the interest you pay each month. Because pharmacists typically carry high debt loads in the six figures, refinance companies will make more money over the course of the loan versus those with much lower student loan balances.

Therefore, as an incentive for you to use a particular company, they will offer a cash bonus or welcome bonus. As mentioned above, you’re not limited to doing this one time. With interest rates always changing, it’s not uncommon for another company to provide a better rate than what you refinanced to the first time.

Now, some big student loan review sites offer nothing to very little to their audience when they refinance in order to take larger commissions. But that’s not our style. We have partnered with several refinance companies that offer bonuses of $300-$800 to you and sometimes higher when they are running promotions. Yes, we receive a commission on each refinanced loan, but we have shifted most of the benefit to you.

If you’re pursuing the Public Service Service Loan Forgiveness (PSLF) program or non-PSLF forgiveness (taxable forgiveness after making income-driven payments for 20-25 years), then refinancing is off the table given it will disqualify you from these programs. If you want to refinance your student loans, check out our current offers below:

Current Student Loan Refinance Offers

Advertising Disclosure

[wptb id="15454" not found ]

4. Take a Moonlighting Position

A few years ago when I was gung-ho about getting rid of my student loans ASAP I was on a mission to figure out how to bring in extra income. At that time, I was limited to 40 hours per week with my full-time job without any overtime opportunities so I had to look for something else. Eventually, I was hired as a PRN pharmacist at a local hospital where I would work in the evenings and weekends allowing me to bring in anywhere from $500-$2,000 extra per month.

If you’re looking for a moonlighting position, consider inquiring at local hospitals and independent pharmacies. While they may not need a ton of help, even a couple of days a month could bring in a decent side income.

5. Earn another certification/credential

In the world of medicine and particularly pharmacy, there are credentials and certifications for everything now. They can be a great way to promote your additional qualifications and training and could even be required for specific academic and clinical positions. Some employers may actually incentivize you to get these as well either in the form of a one time bonus or even a permanent raise.

For example, federal employees who work for the VA are paid based on their grade and step and will have a GS or General Schedule status. The grade usually pertains to the position and the step is typically determined by initial qualifications at the time employment starts and also the years of service. Therefore the most common way to get to the next level is often just to keep your job.

Depending on the facility, one can also add a step or two by earning a board certification or special credential like a Certified Diabetes Educator (CDE). If your employer will also pay for the prep materials and the exam(s) itself, then that’s a double bonus! This is definitely something you want to ask prospective employers about if you are planning to start your pharmacist career or switching jobs.

Beyond raises, it’s possible that some paid opportunities could come knocking. Since getting his BCOP, my friend and colleague Brandon Dyson, PharmD is semi-regularly called by a consulting firm doing research on a new product to figure out the market and to see if this product would integrate into existing oncology practices.

These are usually a 1-hour consult call, and he usually gets paid $200 or $300 each. Although they are not consistent, he notes that once you get a relationship with a given firm, they start contacting you more.

6. Switch to a Higher Paying Job or One With More Opportunities

Many pharmacists express feeling stuck or burned out in their current job and that there’s no way out. It’s true that it can seem overwhelming to make a transition, especially if you’re someone who doesn’t like to step outside of your comfort zone and feel like you’ve lost some of your clinical skills and knowledge to pursue something else. Although it’s never usually easy, it’s definitely possible and making the move could result in more money or the potential to make more money.

My friend and colleague Alex Barker, PharmD, and the founder of the HappyPharmD, created an entire business around helping pharmacists create inspiring work and lives by primarily assisting them in transitioning to pharmacy and non-pharmacy jobs that they are passionate about. He does this through 1-on-1 coaching and also through his free training.

If you’re someone looking to make a job change, I highly encourage you to check out his free webinar on how to escape burnout, get job offers regularly, and take control of your pharmacist career.

7. Start Doing Medical Writing

Brittany Hoffman-Eubanks is a community pharmacist who started her medical writing career about four years ago. Initially, this was a side hustle that brought in a couple thousand dollars per year. It supported her obsession with traveling and need to see everything in the world. Now she is working on making the move to make this her full-time gig.

Medical writing can come in the form of continuing medical education, needs assessments, and research and grant proposals just to name a few.

Although the income from medical writing varies so does the method of compensation. It could be hourly with a huge range of $25-$180/hour, per word typically somewhere around $0.20-0.25 per word, or a flat fee of a couple of hundred dollars to a couple of thousand dollars depending on the scope of the project and writer experience.

If you have stellar writing mechanics and grammar use, and you want to get started with medical writing, Brittany has a few recommendations for you. First, there are several social media groups where you can network and find opportunities and encouragement from other writers. Joining applicable associations such as the American Medical Writers Association is another good idea.

You can also check out episode 126 of the podcast, where Brittany breaks down some other tips for getting started in medical writing.

8. Provide Continuing Education / Other Presentations

If you’re able to deliver an effective message, you could be turning that skill into dollars. Think about how many national, state, and local pharmacy organizations there are. Most of them are paying people to provide CE since it’s something that’s required.

But even beyond pharmacy, many other healthcare providers such as physicians, nurses, physician assistants are also required to maintain their license with ongoing education. Why not reach out and inquire about delivering medication-related programs?

The other great thing is that if you are an expert on a particular topic and have already done the work, you can essentially deliver the same content multiple times across multiple channels enabling you to minimize the time for any prep work.

Beyond continuing education, if you have a great story or possess knowledge on a topic outside of medicine that is needed, people will pay for this as well. Tim Ulbrich, PharmD, the founder of Your Financial Pharmacist, has made around $10,000 in the past two years telling his story about getting out of debt and delivering education on personal finance to pharmacy schools and pharmacy organizations.

9. Start a Consulting Practice

Have you ever thought about starting your own business by providing clinical services? Contrary to what you may have heard, you can get paid for doing MTM and other consulting work. You just have to know the keys to implementing services along with the mechanics of billing and reimbursement. It can be a great opportunity to work more closely with patients and directly impact their health and well-being.

Blair Thielemier, PharmD has set up an entire academy to help pharmacists get their consulting business off the ground. Besides an on-demand online training program, you get access to business coaching and live Q&A calls. You can get $50 off the first month of your membership by using code “YFP50”.

10. Complete Comprehensive Medication Reviews (CMRs) through Aspen RxHealth

Aspen RxHealth is a company with an app-based platform that connects pharmacists with patients to perform MTM. The app connects with Medicare plans and identifies patients who are eligible for a Comprehensive Medication Review (CMR).

What’s cool about their technology is you call the patient directly from the app and then perform all of the necessary functions of the CMR directly within the app. There’s no paperwork and once complete, the patient gets a copy of the review and any recommendations you have.

They currently pay $40/CMR and then typically throw in bonuses and incentives to complete a certain amount within a week or particular days. In one recent report, pharmacists were making around $72/hour based on the volume they were able to complete.

I went through the process myself to check it out and see what it was all about. The onboarding process was fairly easy and smooth and my application was approved within a week. They have a Learning Management System with videos to help get you acclimated to the app and the dos and don’ts of performing a CMR.

What I really liked is that you can work whenever you want and complete CMRs when it’s good for you as long as it is within the typical business hours that the company sets. This also includes being able to make calls on Saturdays.

Once I actually got trained and was prepared to make some calls, it was a little disenchanting because I had made about 15 calls and could not get a single person to answer. Apparently, I am not the only one who has had this issue as the last time I checked it takes an average of somewhere around that number before one typically gets a patient on the line. Because this took me about an hour or more just to make calls without any success, I decided not to continue.

However, I have heard from other pharmacists, that they have someone who makes calls for them to either transfer or set up a time to discuss their medications which could reduce a lot of the wasted time for a pharmacist just making calls.

At one time they were only accepting pharmacists registered in Florida, but you can learn more about the platform and opportunities at www.aspenrxhealth.com.

11. Write a book

With the expansion of ebooks and audiobooks and the tools for self-publishing, it has never been easier to write and publish your own book. While the thought of taking something like this on could seem grueling and years to accomplish, the reality is that it doesn’t have to be dissertation and you could take an idea to finished product in a matter of weeks to months.

When I wrote my first book that educates patients about medications for type 2 diabetes, I was able to get the whole project done within 6 months. It was a very short book but this was intentional in order to keep the reader engaged and not overwhelmed with too many details.

While the process for writing and publishing a book is relatively simple, making a meaningful income that not only covers your costs to create but also ongoing is not. Because everyone is doing this now and there are millions of books on Amazon and other marketplaces, the competition is high. Even if you have an awesome idea that is filled with great content, you can’t expect to just release something on Amazon and sit back and watch the royalties come in.

Marketing and the positioning of your book is really the key to actually make it a profitable endeavor. Yes, you need to have great content that people want to read, but you have to have a strategy on how you will get the message out. If you have a big audience through a blog, podcast, social media channel, or another outlet, that really helps and can be a great starting point. If not, you can partner with other influencers and people with large followings.

If the idea of writing a book sounds intriguing but you have no idea what to write about, here are a couple suggestions. For nonfiction, consider medical topics that are important or widespread that would be of value to patients or other medical professionals.

Test prep or study materials for exams and courses are another option. Outside of pharmacy and medicine, consider writing about a very profound story that involved you or someone you know. If you have a very creative and imaginative side, perhaps writing a fictional book could be up your alley. There are many possibilities out there!

Ok, one big tip I have, if you are going to self-publish, is don’t be cheap on creating the cover. People DO judge books by their covers and many people are turned off if they can immediately determine your book is self-published solely based on the cover. Spend good money on a quality cover!

99 Designs has a great service where multiple designers compete to get you the best cover. A couple of great books to help you get started with the writing and publishing process are Authority by Nathan Barry and Book Launch by Chandler Bolt. If you are interested in doing an audiobook, I would recommend reaching out to Tony Guerra, PharmD who has published and helped other pharmacists publish many books.

12. Teach a course / Become an adjunct professor

Brandon Dyson, the co-founder of TL;DR Pharmacy, author of 100 Strong Residency Interview Questions, Answers, and Rationales, and wizard of all things pharmacy, has been teaching a general pharmacology course for the past five years through Georgetown University School of Nursing.

Currently, the course is offered three times a year and he gets paid for each one, bringing in $4,000 each or $12,000 per year. Not bad for a side hustle, right? The best part is the course is online so he doesn’t have to worry about traveling and does all the teaching and mentoring from home.

If you enjoy teaching and are able to deliver great content in an engaging and professional way, there may be some great opportunities for you. Besides checking out the major pharmacy and non-pharmacy job sites, you could consider reaching out to a local pharmacy school.

Offering to do a free lecture or learning session can be a great way to show off your skills and could result in future paid opportunities. Also, don’t restrict yourself to just pharmacy school. Like Brandon, you should also consider other healthcare professionals like nurses, physicians, and physician assistants who are required to learn pharmacy topics.

13. Serve on an advisory board

An advisory board provides strategic advice to a company or organization and unlike a board of directors, they typically do not have any voting rights or decision-making powers.

Pharmaceutical companies and other healthcare organizations often have advisory boards and there are typically opportunities for pharmacists to get a spot. You often need to be an expert in a particular area or have the experience that can demonstrate your value.

Diana Isaacs is a pharmacist who is an expert in the diabetes arena and has often been asked to serve on advisory boards to provide her knowledge and insight. While the compensation varies, she has typically earned a couple of hundred dollars/hour in exchange for her time. You can learn more about her experience with this in episode 137 of the podcast.

14. Become an Expert Witness

In episode 112 of the podcast, Brent Rollins shared his story about becoming a pharmacist expert witness for law firms primarily focusing on marketing cases in addition to standards of care cases. He was able to get some experience while he was in school when his professor asked for assistance on a big case, he got his start and continued to receive casework.

Many criminal and civil cases involve medications and toxicology and quality of care/negligence where pharmacists can be positioned well to provide their expertise and testimony. While reports vary on compensation, according to a report by SEAK, an expert witness directory company, medical experts earn on average $350/hour.

You can serve as a witness by providing documentation or reports, answering questions by attorneys, depositions, and expert testimony.

Having a colleague as Brent did, to get an in is certainly a good way to get started but also consider your network of friends and family if they are attorneys or know attorneys who frequently take on cases that use pharmacists or other medical experts.

You can also check out some of the big expert witness directory companies/sites such as SEAK , The Expert Insitute, HGExperts. You can also get plugged in with the American Society for Pharmacy Law. which is a nonprofit organization that organizations of attorneys, pharmacists, pharmacist-attorneys and students of pharmacy or law who are interested in the law.

15. Monetize a non-pharmacy skill

In 2019, I made about $3,000 from building websites. Through my experience at Your Financial Pharmacist, I picked up the skill of basic web design and although I’m not an expert by any means, knowledge of the foundation has allowed me to monetize it. Plus, it’s really fun and something I truly enjoy so it doesn’t even feel like real work to me.

Through my podcast interviews with pharmacists who have unique side hustles, it’s evident how talented and creative those in our profession are. What skill or knowledge outside of pharmacy do you have? Is there something you are passionate about that can either help solve other people’s problems or bring incredible value?

Some ideas include photography and video editing, graphic design, IT, translation, voice production, social media management, and marketing. You can check out sites like www.upwork.com and see if there are any freelancing jobs where you have the skills to jump in.

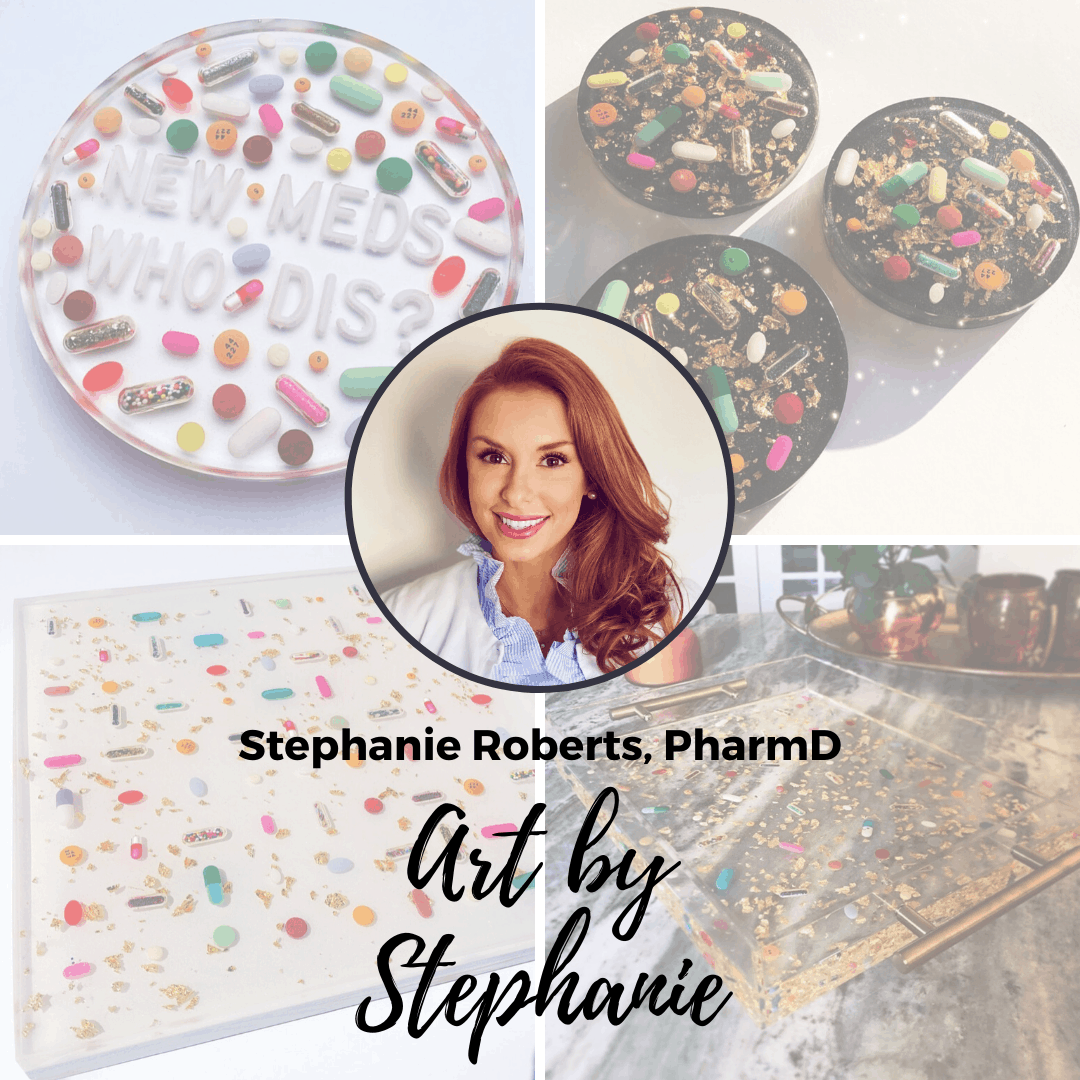

In 2020 I interviewed a pharmacist named Stephanie Roberts (episode coming soon) who had a passion for creating art and did this just as a hobby for a while until one day she had the idea of possibly selling some of her pieces. To her surprise, her pill petri dishes and trays using epoxy resin have been a huge hit and continue to sell out all the time.

She has become so successful that she now makes over six figures with her art alone and pharmacy has become her side hustle! You can see some of her work below.

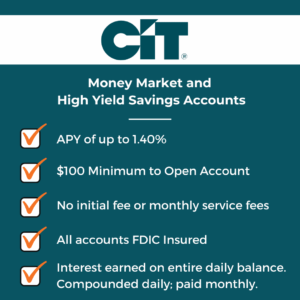

16. Switch to a high yield savings account or money market account

When you consider inflation, money sitting in regular checking or savings accounts can lose a lot of purchasing power over time given most interest rates are essentially next to nothing.

Sure you avoid market risk or the risk of keeping cash in other investments but there are other options that are less risky and can yield at least some return. These include high yield savings accounts and money market accounts.

If you are sitting on a bunch of cash that’s for an emergency or you are saving for a big purchase, these can be good options can earn a little extra money. Now if your savings amount is relatively low and you aren’t adding anything to it then it may not be anything substantial, but remember it’s better than 0.001%.

I recently did a review of my experience with CIT Bank which offers competitive interest rates from 0.85-1.40% for their high yield savings and money market accounts.

17. Become an Airbnb host

Tim Baker CFP®, team member on the Your Financial Pharmacist team loves to take his family on vacations around the country and the world. But frequent trips can get expensive. That’s one of the reasons why he and his wife became an Airbnb host. In just 1.5 years they have made $10,000!

Hilary Blackburn is a pharmacist in the Nashville area who rents out her primary residence about 14 times per year and has been able to earn about $8,000 per year or more. You can learn more about how she’s making it happen on episode 121 of the podcast.

If you’re not familiar with Airbnb, essentially it is an alternative way to lodge instead of the traditional hotel. As an Airbnb host, you list a property you own or rent on their platform for guests to book and stay. Airbnb only takes 3% of the total reservation so you keep most of the booking fee.

Some people host their primary residence when they are out of town or have additional rental property or space that they list. For some, the thought of having strangers stay in your house even if you’re not there may seem pretty overwhelming and concerning.

Sure there are some potential issues that could occur such as theft or vandalism but you have control over who is able to stay based on reviews and other factors on the Airbnb platform. Plus, as a host, you get access to up to $1 million of property damage protection if you ever need it.

If you want to find out how much you could earn by listing your space, you can check out the Airbnb estimator below.

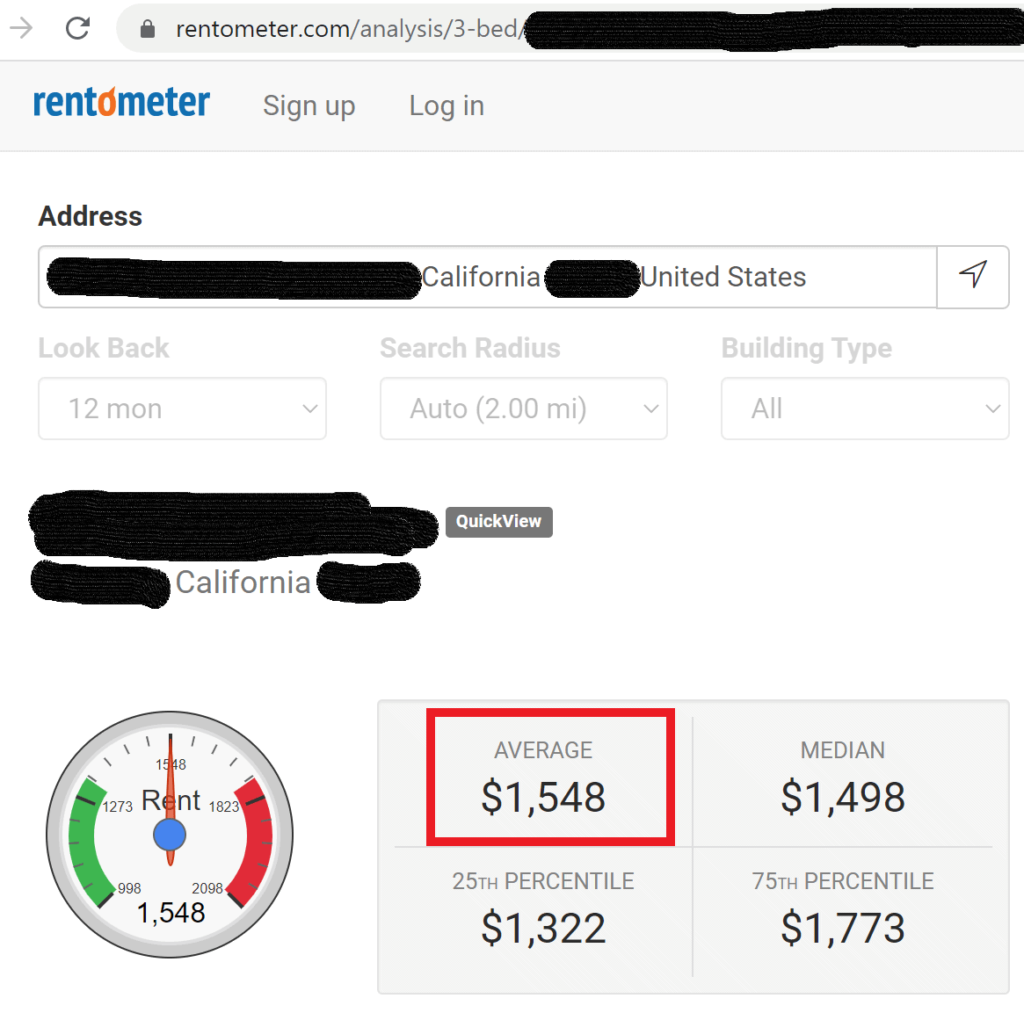

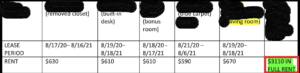

18. Buy a rental property / House Hack

Many people have built entire businesses around managing rental property. On one of our most popular podcast episodes, Carrie Calton, PharmD discussed how she achieved financial freedom by acquiring 18 rental properties! You don’t need a ton of cash in order to purchase a property as you can typically get approved with even a low down payment. However, that amount will be dependent on your risk tolerance and the equity you want to start with.

It may seem enticing to simply look at the potential mortgage payments vs. how much rent you could collect for a particular property. However, when you are doing an analysis to determine if the property would be cash flow positive and provide another stream of income, you have to consider ALL of the costs and maintenance involved such as insurance, HOA, taxes, repairs, capital expenditures, etc.

Along the lines of buying a rental property is house hacking. This usually involves buying a property with a low percentage down (generally 1, 3 or 5%), living there for a year (required), and renting out the other units or rooms. For example, if you purchase a single-family home, then you would rent out the other bedrooms.

Or if you owned a duplex or condo with multiple units, you can live in one and rent the others. Depending on the cash flow, you may be able to cover the mortgage payment and even make a profit. Check out episode 130 for more information on this.

Bigger Pockets is a great resource to get started and learn more about real estate and rental properties. Besides their podcast and online resources, they also have an awesome book: The Book on Rental Property Investing by Brandon Turner.

19. List your car on Turo

What happens to your car when you go on trips or the days when you don’t need it? It probably just sits in your garage or driveaway right? But what if your car could make you money? With Turo, you can!

Often referred to as the Airbnb of vehicles Turo is an alternative to a traditional car rental service. From the user standpoint, through their platform, you enter the date and location you are looking to use a vehicle, choose what you want, and book. You can pick it up or even have it delivered to you.

So how much can you earn? It varies from $40/day up to several hundred dollars per day depending on if you are handing the keys over to a Toyota Corolla or Mercedes E-class. Here’s an example based on Turo’s calculator. If you have 2018 Tesla Model X and live in the Miami area, you could earn approximately $1,724 or $180/day if your car was booked an average of 9.6 days per month. Not bad right?

You’ll earn 65% to 85% of the trip price, depending on the vehicle protection package you choose but you can also choose to just use your own commercial insurance which could get you a bigger cut.

Conclusion – How to Make More Money as a Pharmacist

There are many practical ways to make extra money as a pharmacist. Some are directly related to the profession while other opportunities exist by capitalizing on other skills and interests you have. Some need relatively little time and effort (i.e. refinance student loans) whereas others may require additional training and several hours of work.

With the pharmacist salary being relatively fixed, having a side hustle and earning additional streams of income can help you reach your financial goals faster and help pay back pharmacy school loans. It can also give you an added layer of protection from relying on one source of income, which is important as the profession continues to undergo changes and technology and innovation are disrupting traditional roles and positions.

Another Way to Find Side Jobs for Pharmacists or a Pharmacist Side Hustle

If you want some additional inspiration I would recommend checking out the side hustle series where I interview pharmacists who have businesses and gigs that bring in additional monthly income.

Recent Posts

[pt_view id=”f651872qnv”]