These Tax Benefits Get Unlocked When You Have or Adopt a Child

The post is for educational purposes and does not constitute financial advice.

Everyone talks about how much it costs to have or raise a child, and for good reason! Having or adopting a child is not an inexpensive thing to do. You may be surprised at how much you spend after factoring in the accumulated costs of necessities like healthcare, food, housing, and clothing on top of activities, sports, and the toys that they have to have. According to a 2015 report from the U.S. Department of Agriculture, middle-income married couples could spend $233,610 to raise a child until they are 18. After adding in inflation, the cost rises to $284,570!

That’s obviously no small chunk of change.

The good news, aside from the immense amount of joy they can bring into your life? Having or adopting a child can unlock several key moves you can make that can help to lower your tax bill and allow you save for future tuition expenses.

1. Child Tax Credit

Taxpayers who claim at least one child as a dependent on their tax return may be eligible to receive the Child Tax Credit (CTC). The Child Tax Credit is different from a tax deduction. A tax deduction reduces your taxable income, but a credit actually lowers your tax liability or the amount that you owe the IRS. For example, if you have a $5,000 tax bill and are eligible for the Child Tax Credit, you’d owe $3,000 instead. Another amazing feature of this credit is that you’re eligible to receive a refund for up to $1,400, so if the credit brings your tax liability below zero, you could receive a refund up to that amount. Woohoo!

For 2020, the Child Tax Credit is capped at $2,000 for each qualifying child and begins to phase out for those earning $200,000 filing single and $400,000 married filing jointly. To qualify for this credit, you must have earned at least $2,500 in the tax year.

Check out this IRS tool to see if you have a child that would qualify for you for this credit.

2. Child Care Credit

Paying for childcare is a huge expense that parents and caregivers have to face. According to the Center for American Progress, the average cost of center-based child care for an infant in the United States is $1,230 per month. With a family care center or in-home daycare, average costs are around $800 per month. If you have multiple children, you’re obviously looking at a larger bill.

Fortunately, there is the Child and Dependent Care Expenses Credit to hopefully provide some relief to families that are paying for out-of-pocket child care expenses come tax time. The Child and Dependent Care Expenses Credit is designed as a non-refundable tax credit that can cover 20% to 35% of your expenses. Qualified expenses include babysitters, preschool or nursery school, day camp or summer camp, daycare costs, and before and after school care. There are no income restrictions for claiming this credit, however it is capped at $3,000 for one child and $6,000 for two or more dependents that live with you for more than half of the year.

The caveat is that you can only claim this credit if you are working or are looking for work during the time of care, so babysitter expenses for date nights out (or in, thanks COVID!) don’t count. Additionally, you can’t claim payments to your spouse, the parent of the dependent child, a dependent listed on your tax return or your child who is 18 years or younger whether they are listed as a dependent on your return or not. Additionally, you can’t combine this credit with expenses that were paid with pre-tax money from a dependent care flexible spending account. To use the Child and Dependent Care Expenses Credit, Form 2441 must be filled out when filing your taxes. In order to claim payments made to a care provider, you must provide their name, address and Taxpayer Identification Number or a Tax ID number for a preschool or daycare.

3. Adoption Tax Credit

Adopting a child today can cost up to $50,000. The cost is dependent on the country you are adopting the child from, the type of agency or adoption professional you work with, and medical, travel, or other adoption expenses you may incur.

The Adoption Tax Credit is in place to help relieve some of the expenses you may have during the adoption process. This tax credit is non-refundable meaning that it can help lower your tax liability, however you won’t receive a refund because of it. The credit is also only available for the tax liability for that year, although if you have a remaining balance on the credit you’re able to carry that excess forward for up to five years. For 2020, the maximum credit adoptive parents are able to claim is $14,300 per eligible child (child has to be under the age of 18 or mentally or physically incapable of caring for himself or herself). Additionally, there is an income limit and phase-outs on the credit. If your MAGI is below $214,520 then you’re able to claim the full credit. If your income falls between $214,520 to $254,520 you can receive partial credit. However, if your income is above $254,520 then you’re unable to claim the credit.

According to the IRS, the Adoption Tax Credit can be used for the following adoption-related expenses: necessary adoption fees, court costs and attorney fees, travel expenses including meals and lodging, and other expenses that are directly related to the legal adoption of a child. These expenses can count toward the credit even before a child has been identified for the adoption. You can still use this credit for qualified adoption related expenses even if the adoption falls through and never finalizes.

Additionally, some employers offer employer-provided adoption benefits to pay for qualified adoption expenses. These benefits can be excluded from your taxable income for up to $14,300 in 2020, however, you cannot double-dip by using the same expenses in the exclusion as you’re claiming in the credit.

The timing of using the Adoption Tax Credit can vary depending on when you pay the expenses, if and when the adoption was finalized, and whether it’s a domestic or foreign adoption. It’s best to consult with a tax professional to ensure that you’re claiming the credit correctly.

4. Dependent Care Flexible Spending Account

You may have heard of a Flexible Spending Account that allows you to save pre-tax dollars from your pay into an account that can be used for qualified medical expenses, but did you know that a similar account is available to pay for child care costs?

A Dependent Care Flexible Spending Account (DCFSA) is an account offered through your employer where you can use the funds to pay for qualified child care costs. You authorize your employer to hold a certain amount of money on a pre-tax basis each pay period that is then deposited into this account. Unlike an HSA, you cannot spend the money directly from the account. Instead, you have to pay out-of-pocket for the expense, submit the expense and then receive reimbursement.

Qualified expenses that can be covered with a DCFSA include before and after school care, babysitting or nanny expenses, daycare/nursery/preschool costs or summer day camp. It’s important to note that the child or children receiving care must be under 13 years old. You can also use this account to pay for care for your spouse or another adult that is claimed as a dependent on your taxes, who cannot take care of themself and that lives in your home.

Expenses that do not qualify include paying for education or tuition fees, overnight camps, expenses for children over 13, field trips, or transportation to or from the dependent care provider.

You can contribute up to $5,000 per year if you’re married and filing jointly. If filing single, you can contribute $2,500 per year. This can be a powerful way to save money for expenses that you know you’ll need to pay for. Because the money comes out of your paycheck pre-tax, you’re lowering your MAGI and ultimately your tax bill.

However, this money doesn’t rollover. Like the healthcare FSA, you have to use it or lose it, so only contribute an amount that you know you’ll use throughout the year.

5. 529 Plan

Depending on your financial goals and plan, saving for your child’s or children’s education may be a top priority for you. One of the most popular ways to do so is with a 529 plan.

There are two types of 529 plans: 529 college savings plans and 529 prepaid plans. 529 college savings plans are the most widely used. Money is contributed after tax, grows tax-free, and is distributed tax-free as long as it’s used for qualified expenses. 529 plans are generally run by your state, however, you don’t have to use that plan and can choose another plan instead.

529 prepaid plans allow you to prepay for a partial or total amount of tuition, but this type of plan isn’t available in every state. While 529 prepaid plans are also tax-deferred, it often doesn’t cover as many expenses as the 529 college savings plan does. According to Saving for College, if you opt for the prepaid plan you may have to pay a premium for tuition and you may not have enough money saved for future tuition costs.

You’re able to open a 529 plan at any time and there aren’t any income phaseouts or age limits on contributions or when the funds have to be used. In the past, 529 plans were only available for undergraduate, graduate, medical, and law school, but that changed in 2018. Now 529 plans can also be used for tuition costs for K-12 education (up to $10,000 per year per child) in addition to higher education costs. Qualified expenses for 529 college savings plans include tuition and fees, books, supplies, equipment, room, and board (if the student is enrolled at least half time), and computer or software equipment, among a few others. However, 529 prepaid plans often only cover tuition and room and board.

Another feature of the 529 plan is that you can choose from a few dozen investment options and can mix funds depending on your risk tolerance. Many plans also have age-based options where the money is invested more aggressively when the child is younger and moves to more conservative allocations as the child gets closer to college age. Another perk of the 529 plan is that many states also allow you to take a tax deduction or tax credit for your contributions which could in turn lower your modified adjusted gross income (MAGI) and tax liability.

When it comes time to fill out FAFSA (Free Application for Federal Student Aid), as long as the 529 plan is owned by a dependent student or a dependent student’s parents, it’s reported as a parent’s asset and the distributions are ignored. This allows you to receive more favorable federal financial aid than if it were added to the student’s assets.

But what if your child decides not to attend college? You have the option to change the name of the beneficiary on the account to someone else in the family, like a brother, sister, cousin, or parent. Remember, there is no age limit on using money from a 529 plan so you can pass this money through your family for as long as you want. If you don’t want to give the money to another family member or save it for a future grandchild, you can withdraw it but you’ll have to pay taxes on any growth earnings as well as a 10% penalty.

6. Coverdell Education Savings Account (ESA)

If a tax-advantaged 529 plan doesn’t seem like a good fit for you, there is another option to save for your child’s education. Formerly known as the Education IRA, the Coverdell Education Savings Account (ESA) is a tax-deferred trust or custodial account designed to help families pay for education expenses. Money contributed to a Coverdell ESA grows tax-free and is distributed tax-free as long as the money is used for a qualified expense. The ESA can be used to cover the cost of tuition, fees, books, and sometimes room and board for higher education as well as elementary and secondary education (K-12).

Anyone can create a Coverdell ESA account through a brokerage account, bank, credit union or mutual fund company, however the beneficiary must be younger than 18 years old at the time it’s opened. Depending on your income, you can contribute $2,000 total per year to a beneficiary.

Your contribution limit begins to phase out if your modified adjusted gross income (MAGI) is between $95,000 and $110,000 for single filers or $190,000 to $220,000 for joint filers. If your MAGI is more than $110,00 (filing single) or $220,000 (filing jointly) then you can’t make any contributions. You also can’t make any contributions to the account after the beneficiary is 18.

Unlike a 529 plan, the funds must be dispersed by the time the beneficiary is 30 years old (except for a special needs beneficiary). If the distributions are higher than the education expenses of the account holder then a portion of those earnings would be taxed to the beneficiary. If the funds aren’t used in their entirety there are options to either roll them over to a family member’s Coverdell ESA account, transfer them to a 529 plan or withdraw them. If the funds are withdrawn and not used to pay for a qualified expense, the earnings would be counted as taxable income and an additional 10% would be changed as a penalty.

One of the benefits of choosing a Coverdell ESA comes down to investment options. With this account, you can self-direct your investments and choose from a range of individual, international or domestic stocks, bonds, mutual funds, exchange-traded funds (ETFs) and real estate investments. These options vary depending on where the account is opened. You’re able to adjust your investment portfolio as many times as you’d like.

Conclusion

Between dependent care flexible savings accounts, child care or child tax credits, and options to grow your money while you save for your child’s education, there are a lot of powerful tax moves that should be considered once you have or adopt kids. It’s important to take a step back and analyze your tax strategy so that you can decide which options are going to work best for your financial plan.

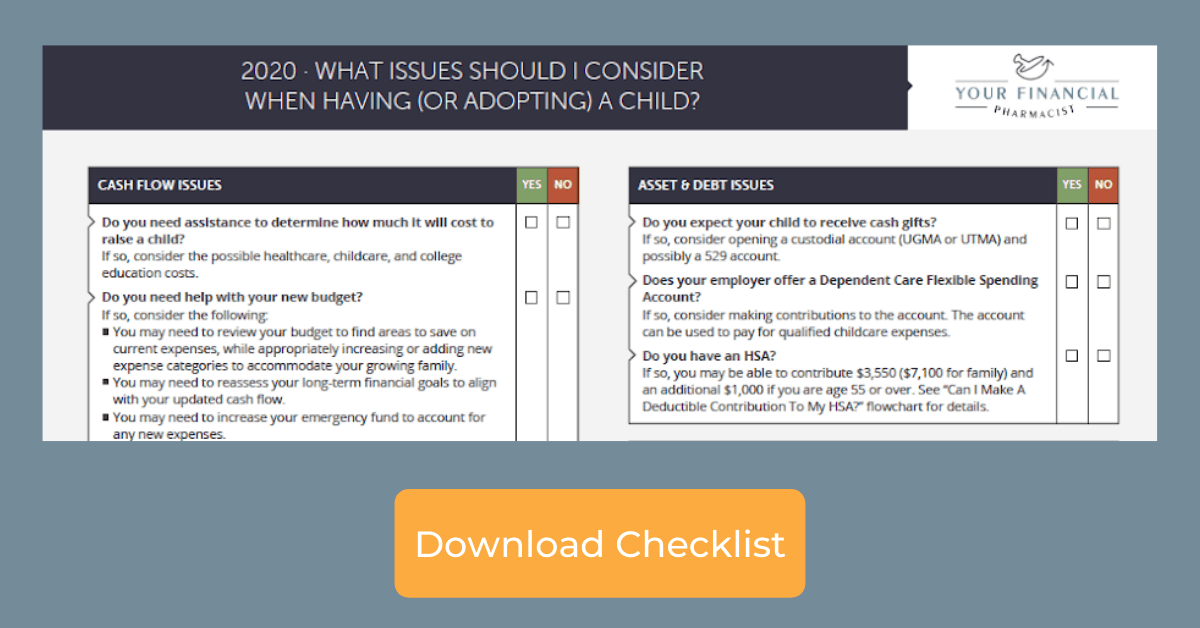

If you want to check out more money tips to consider when having or adopting a child, check out the comprehensive checklist below.

Need Help Trying to Determine Which Tax Moves to Consider?

Trying to navigate the possible tax moves for your situation can be overwhelming. If you need help analyzing which moves work best for your family, how you can get the most out of saving for your child’s education or with your overall financial plan, you can book a free call with one of our CERTIFIED FINANCIAL PLANNERSTM.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]Recent Posts

[pt_view id=”f651872qnv”]