6 Boring Financial Moves Worth Making

The following is a guest post from Dr. Jeffrey Keimer. Dr. Keimer is a 2011 graduate of Albany College of Pharmacy and Health Sciences and pharmacy manager for a regional drugstore chain in Vermont. He and his wife Alex have been pursuing financial independence since 2016. Check out Jeff’s new book, FIRE Rx: The Pharmacist’s Guide to Financial Independence to learn how to create an actionable plan to reach financial independence.

Today’s the day.

You’ve spent the better part of a decade getting your PharmD, passed your boards, and got the job. But today’s the day it’s supposed to all pay off; for today, you finally get that sweet first paycheck as a pharmacist.

Welcome to the club!

But now what?

Well…whatever you want, right? After all, the world’s your oyster now that you’re making good money. Live it up! And even if you don’t have the money on hand to do what you want right now, you’ve got a big income to support a big credit limit. Charge it!

Unfortunately, a lot of us (myself included) buy into this mindset and fall into a financial quagmire because of it. What starts as something innocuous like “I’ve worked hard for a long time and now I’m going to treat myself” has a funny way of becoming “Wow, I make six figures and live paycheck to paycheck!” And if you don’t believe that’s a thing, tell that to the majority of high-earning Millennials who report living that life.

It doesn’t have to be that way though. There are moves you can make to protect yourself from such first-world problems. But here’s the rub, most pharmacists (and people in general) don’t like making some of these financial moves because they can be boring, tedious, and might be outside your comfort zone. If you can get past that though, these moves could pay off in the long run.

So with that, let’s dive in!

1. Make and Keep a Budget

This one’s probably the most essential thing you can do to keep your finances on track. Knowing how much money’s coming in, how much is going out, and what can be saved is elemental to the financial plan. If you aren’t budgeting, I’d dare say that you’re going to find it very difficult, if not impossible, to meet most of your bigger financial goals.

So why does this one top our list?

In truth, budgeting can be one of the most boring activities that fall under the broad umbrella of things considered “adulting.” It requires you to take an accurate accounting of not just the money you have coming in, but the money that’s going out and where it’s going. Poring over pay stubs, bank statements, and credit card bills to get all this data isn’t just recommended, it’s required. Oh, and you’ll probably need to make a spreadsheet or two.

Sounds like fun, doesn’t it?

And that’s just what goes into making an initial budget. To make budgeting work for you, you need to get in the habit of sitting down with all these numbers regularly (usually once a month, if not more often). Like a diet, success with budgeting is only going to occur when you practice it consistently for the long run. Fortunately, budgeting isn’t that hard to do and there’s even more than one way to do it.

For most of us, the thought of budgeting invokes a picture of sitting down with your finances once a month, going over your income and expenses, and seeing if there’s money left over to put toward goals. This kind of process, known as “zero-based budgeting,” is the most basic form of budgeting you can do and will likely be the first budgeting style you try. It can also be a pretty tedious process as you need to dissect each month’s spending and see how it compares to the goals you set for yourself ahead of time. For instance, say you want to set a budget of $150 a month for clothes, and this month you only spent $135. Great! The extra $15 can be added to the amount you can save this month. Conversely, if you went over budget in that category by $15, hopefully, you underspent in another category. If not, you’ll need to dip into existing savings to cover the shortfall.

Given the fact you need to repeat this process for every spending category, month after month, it’s not hard to see why many people don’t care for it. Still, it must be done. Don’t fret though, there are plenty of tools available to help you out along the way. For starters, you can avoid having to make a budget spreadsheet yourself and get one for free right here at YFP. This template will walk you through the steps required to make your first budget. Beyond that, there are some excellent platforms available to keep you on track. I was a big fan of the app Mint when I was getting started as it automatically drew all the data I needed from my accounts, aggregated it, and presented it to me on a clean interface.

Using that app, I was also able to get a handle on my spending trends over time and better predict my spending in the more variable categories (ie. food, clothes, entertainment, etc.) which allowed me to pursue a more convenient budgeting style. By knowing what I usually spent in those variable categories and seeing a consistency over time, I could also (in theory) treat the whole lot of them as a single line item. This led me to create a budget for myself which is sometimes referred to as a “reverse budget” in which money for savings is taken out first (in my case every pay period), and then you live off what’s leftover. It’s kind of like living paycheck to paycheck, but without worrying about how you’re going to pay the rent. For me, this style has worked very well as it involves little work beyond the initial setup. I get paid, my spreadsheet tells me how much extra I should have, and I send that money toward goals. The only time I revisit the numbers on the spreadsheet is when they change. That’s it! If you’ve been using a zero-based budget for a while or happen to have a few years of data showing relatively consistent spending, migrating over to a reverse budget might help you keep things going long term.

However you decide to do it, the bottom line here is you need to budget. Full stop. All of the other things we’re going to talk about in this post can be crucial to the financial plan, but they pale in comparison to the importance of budgeting. If you’re not already doing it, get started today!

2. Protect Thyself!

Ok, I tried to give this one a more exciting title, but this section encompasses the most boring things you can do as part of the financial plan. In this bucket, you’ll find riveting topics such as insurance policies, designating a power of attorney, and even writing a will! Hoo boy!

Pumped? Yeah, I didn’t think so.

But the truth is, taking steps to secure yourself against life’s uncertainties is never a fun exercise, and sometimes the process can even be a little uncomfortable. It’s worth it though, and you really should consider taking action here. After all, stuff happens in life and even the best-laid plans can get torn to shreds by the unforeseen.

When it comes to insurance, most of us are pretty familiar with health, home, and auto policies, and these are all essential and may even be legally required to have in some cases. But what about insurance that protects your income and those who depend on that income? Life and disability insurance policies typically aren’t given the kind of attention and essential label that the above do, but for many of us, they probably should. After all, your income is the lifeblood of you and your family’s financial plan, and securing it is important! It’s tough to think about dying prematurely or losing the ability to work, but preparing for the worst is always a good move.

Life insurance can be a pretty complicated topic, especially when you consider the fact that many policies out there combine insurance with investing. Rather than getting into the weeds on the pros and cons of different types of policies (for that, check out my other post Life Insurance for Pharmacists: The Ultimate Guide), I’ll just say that the most important thing to consider here is getting a death benefit sized to your situation for the lowest amount of premium from a reputable insurance company. And given the importance of getting that sizing right, it’s probably not a bad idea to work with an advisor or agent when getting a policy.

Be forewarned though, policies that have investing components such as whole life or universal life tend to have MAJOR financial incentives for the agents selling them. As such, those agents (who may also call themselves financial advisors) may not be acting in your best interest when pitching them to you. For most new pharmacists, these types of policies are rarely the best option. In general, term life policies that meet your basic need for insurance are what to look for.

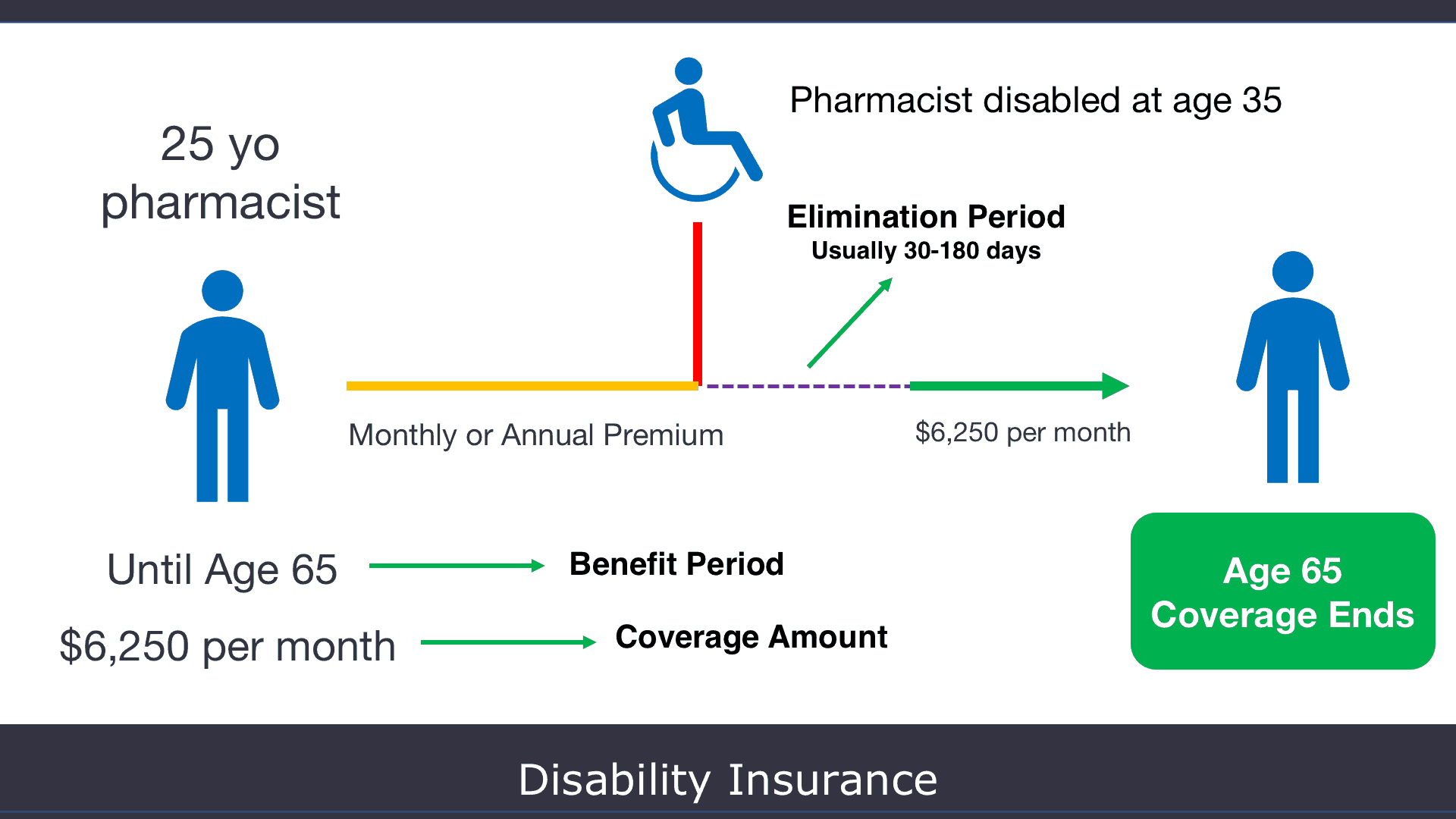

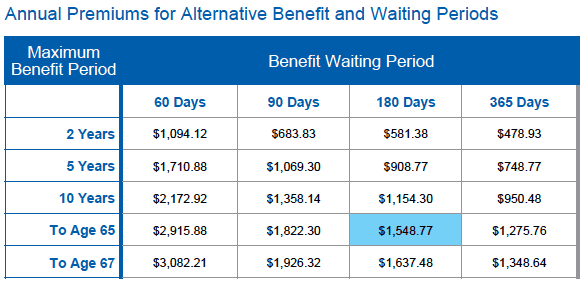

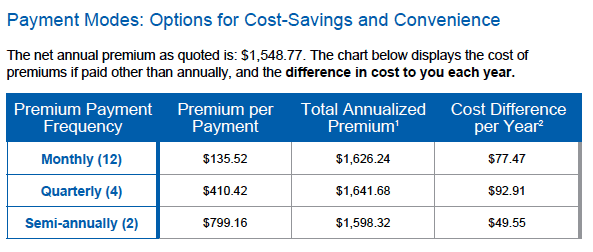

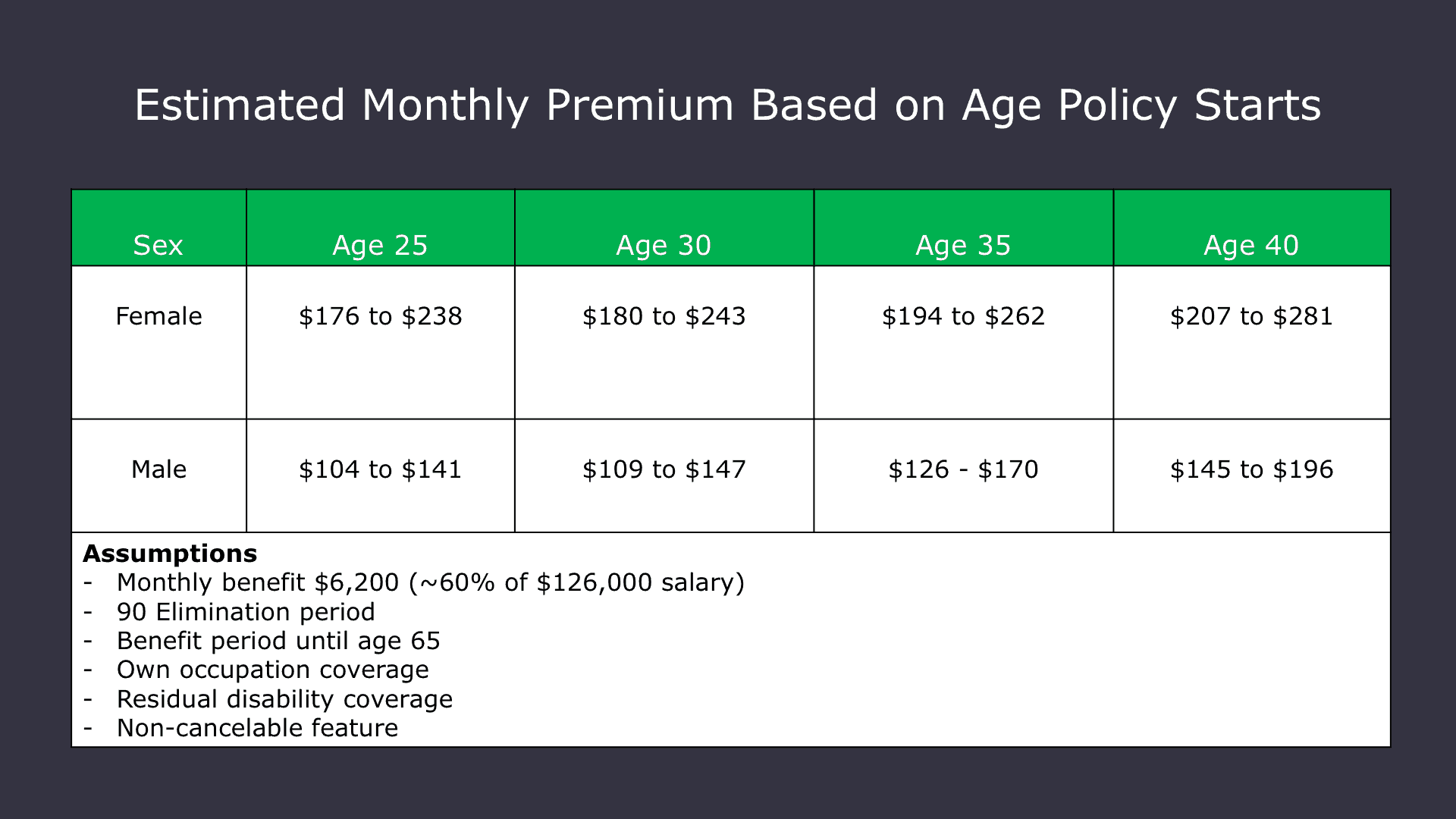

If life insurance is a good fit for your financial plan, then you’ll want to consider getting disability insurance as well. Thankfully, disability insurance is a little more straightforward. At a basic level, you need to choose how long you want to receive benefits, the amount you’d receive, and how long it will take before benefits kick in (also known as the elimination period). In addition, you may want to get a policy that’s specified as “own occupation” disability insurance because receipt of disability insurance otherwise is predicated on the idea that you can’t work, period. Unless you have an own-occupation policy, disability payments can be denied if you could reasonably work in a different capacity, even at a much lower rate of pay. For more on disability insurance, be sure to check out this must-read on the YFP blog, Disability Insurance for Pharmacists: The Ultimate Guide.

Finally, when it comes to protecting you and your family in the event of the unthinkable, having other plans in place such as a durable power of attorney, will, and/or estate plan can go a long way. These things can make your wishes known in the event you’re unable to say them yourself. For more on this, be sure to listen to YFP Podcast Episode 222: Why Estate Planning is Such an Important Part of the Financial Plan.

3. Tackle Debt

Once you’ve started to budget, getting out of debt tends to be one of the first financial goals people set for themselves. After all, being debt-free is pretty awesome.

So why does this one make the list? Because while being debt-free can be exciting, getting there can be a pretty boring process. On top of that, if you have student loans you are trying to pay off, an optimal strategy may involve a suboptimal amount of paperwork to boot.

For most of us, eliminating a substantial amount of debt boils down to following a budget and applying the savings from that budget consistently. Put in the work, grind it out, and the debt will eventually be gone. That said, there are ways to optimize the process.

There are two main strategies for straight debt pay off: the avalanche and the snowball. The avalanche strategy involves you paying off debts in order of smallest to largest. With the snowball method, you’ll pay off the debt that has the highest interest rate first, eventually working your way down to the lowest interest rate. There probably won’t be much of a difference between the two in terms of how quickly you’ll pay off the debt, but these strategies do provide a roadmap to get you from start to finish.

But while the path to get rid of most types of debt can be straightforward, the best path to get rid of your student loans can be a little less clear. Depending on the type of loans you have, your employment status, and your level of discretionary income, you may find that the optimal strategy for addressing your loans is a lot different than simply grinding them away. For more on that, be sure to check out Tim Church’s comprehensive book, The Pharmacist’s Guide to Conquering Student Loans as well as the excellent post The Ultimate Guide to Pay Back Pharmacy School Loans.

If, after carefully considering all of the payoff strategies available to you, you decide that simply paying them off is the best course of action, visit the refinancing hub at YFP so you don’t pay a dime of interest more than you need to. You might be able to get some extra cash too!

4. Avoid More Debt

Once you get out of debt, it’s only natural to feel that your financial picture has relaxed a bit. After all, these are bills you’ve likely eliminated from your life forever. But now that they’re gone, it’s incredibly important that you don’t replace them with new ones. Believe me, keeping up with the boring grind that got you out of debt after paying everything off is easier said than done.

There’s a theory in economics known as the “wealth effect” which shares that as the value of people’s assets rise, they tend to spend more. I would argue that the same can be said when you get rid of debt. Your net worth rises and the cash flow available from your biggest asset (your income) increases. Taken together, the pressure to upgrade your lifestyle goes up as well. After all, you can afford nicer things now, denying yourself these pleasures would be on you alone, not the fact you have a loan payment due.

This is something I started to struggle with once the only debt I had in my life became my mortgage. With all the other big monthly bills gone, the amount of extra cash available every paycheck seemed to give me license to spend a lot more than I had previously. While my experience in personal finance taught me to avoid credit card debt like the plague (and I do), it’s a lot harder to keep thoughts of buying a nicer car or considering a home upgrade at bay; both of which have a nasty habit of getting you back into debt. Add temptingly low-interest rates into the mix and, well, you get the picture.

5. Force Yourself to Save More

Going hand in hand with keeping yourself out of debt is then using that money to save more. This can be tough because unlike getting out of debt, saving money doesn’t have a well-defined endpoint and the goal you set for yourself can shift over time. In addition, unless you’re in a group that likes to share financial successes, getting external validation (and motivation) about your savings habits is unlikely. After all, people see nice stuff, not nice balance sheets.

Thankfully, there’s a concept I’m going to borrow from the Financial Independence, Retire Early (FIRE) movement that we can use here to make savings a little less boring and give you a better-defined goal to work with. It’s called the “four percent rule.” In a nutshell, the four percent rule sets the amount you need to save to be considered financially independent as 25 times your annual expenses.

How does that make saving less boring? Easy. With a defined goal in mind, you can give your savings journey milestones to get excited about! For example, getting to a point where you have $100,000 in your investment accounts can sound pretty good on its own, but it can be much more meaningful in the context of where you are in your journey to financial independence; arguably the end goal for everyone taking charge of their financial futures.

6. Be Honest With Yourself as an Investor

Finally, I wanted to touch on this one not just because it fits the theme of boring things to do, but because I think as pharmacists (like other highly compensated professionals), we can easily fall into the trap of thinking we’re smarter than we are when it comes to investing. I’ve been guilty of this. But despite what you may hear in the news about small “investors” making scads of money on the latest meme stocks or cryptos, the truth is that day trading the market is a great way to lose money over the long run, or worse. For most investors, following a boring, buy-and-hold style of investing using a diversified mix of quality assets that aligns with your risk tolerance is typically a much better play.

Conclusion

The bottom line is that the path to long-term wealth and financial prosperity isn’t always sexy. Along the way, there are things you’ll need to do that are, frankly, quite boring. But if you can get past that and put in the work to make and keep a financial plan that allows you to build wealth in a secure, consistent way, you’ll be well on your way to reaching financial independence.

Need help figuring out which financial move to make next?

If you’re interested in having support on your financial journey, I encourage you to book a free discovery call with the team at Your Finanial Pharmacist. Your Financial Pharmacist is a fee-only, comprehensive, high-touch financial planning firm that’s dedicated to serving pharmacy professionals like you.

You can book a free call to see if Your Financial Pharmacist is the right fit for you.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]