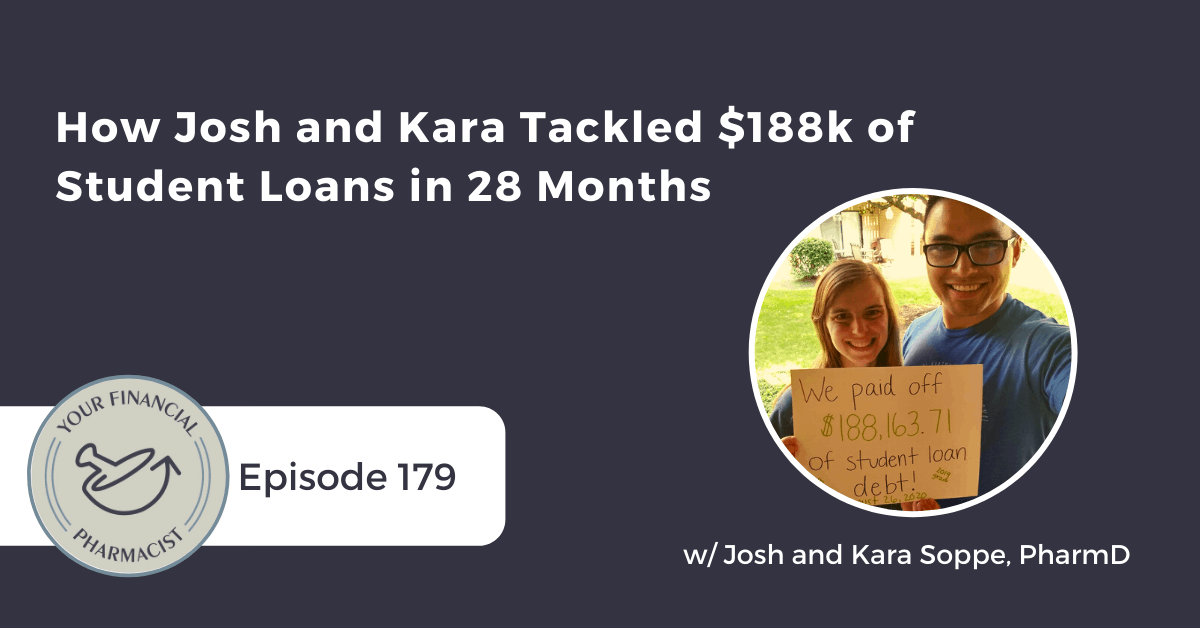

How Josh and Kara Tackled $188k of Student Loans in 28 Months

Pharmacists Josh and Kara Soppe join Tim Ulbrich to share their journey of paying off $188,000 of student loan debt in 28 months. Josh and Kara dig into why they chose to aggressively tackle their student loans, their strategy for paying them off, how they created and implemented a budget, and their plans now that their student loans are paid in full.

About Today’s Guests

Josh and Kara Soppe met at Ohio Northern University in 2013 and now reside in Dayton, Ohio. Josh graduated from ONU in 2018 and is a Clinical Informatics Pharmacist with the Kettering Health Network. Kara graduated from ONU in 2019, completed a PGY1 Pharmacy Practice Residency at Kettering Medical Center (KMC), and stayed on at KMC as a Staff/Clinical Hybrid Pharmacy Specialist.

In 2017, they attended Tim Church and Tim Ulbrich’s book launch for Seven Figure Pharmacist: How to Maximize Your Wealth, Eliminate Debt, and Create Wealth. Josh and Kara read the book together and were intrigued by the aggressive student loan pay-off strategy. During pharmacy school, they started developing a plan to eliminate student debt within 2.5 years of Josh’s graduation. Freedom from student debt allows them to focus on their goals to become foster parents, own real estate properties, and save aggressively for retirement.

They are excited to share with you the steps they took to pay off $188,163.71 of student loan debt 27.5 months after Josh’s graduation.

Summary

Josh and Kara Soppe share their incredible journey of paying off $188,163.17 of student loans in 27.5 months. Although their debt load is more modest than many pharmacist couples graduating today, $188,000 is still a lot to tackle. Josh explains that he was aware of student loan debt before he started applying for colleges in high school. While in college Josh found scholarships and grants and took a position in residence life to reduce his debt load. Kara became really aware of how much she was taking out in student loans when her first loan installment dropped. She became proactive in reducing her debt by working as a pharmacy intern and taking a position in residence life.

Josh and Kara were motivated to pay off their debt quickly because of a few key principles they wanted to instill in their lives: tithing and giving, growing their family through biological children, adopting and fostering, and real estate investing. They had these conversations while they were still in college and knew they had to make sacrifices along the way so that they could reach those goals quicker.

Josh shares that they took a mathematical strategy to pay down their debt and went after the higher interest rates first. They also refinanced their loans multiple times to get lower rates and cash bonuses. They were paying, on average, $6,700 a month and had to give up luxuries like new furniture, new cars and eating out to reach their debt pay off goal. Josh and Kara share how they were able to make such large payments each month and what their plans are now that they are debt free.

Mentioned on the Show

- YFP Planning: Financial Planning for Pharmacists

- Connect with Tim Ulbrich on LinkedIn

- Refinance Your Student Loans

- Mint

- The Pharmacist’s Guide to Conquering Student Loans by Tim Church, PharmD

Episode Transcript

Tim Ulbrich: Josh and Kara, welcome to the show.

Josh Soppe: Hey, thank you. We’re excited to be here.

Kara Soppe: Yeah, we’re very thrilled.

Tim Ulbrich: I really appreciate you guys taking time to come on to share your debt free journey. And Josh, I appreciate you reaching out. I was happy to read your message you sent me on LinkedIn about how you and Kara were able to aggressively pay off your debt, $188,000, in 28 months. Actually, $188,163.71 — in case anyone was counting — of student loan debt in 27.5 months and were able to do this even while Kara was finishing up her PharmD at Ohio Northern University — go Polar Bears! — and completing her PGY1 residency. So appreciate your willingness to share your story as I’m sure it will be impactful for many of our listeners that are facing perhaps a similar situation. So before we dig into how you paid off the debt, what worked, what didn’t work, what’s ahead for you, what was the motivation, I’d like to hear from both of you about your backgrounds and careers in pharmacy thus far since graduating as I think we’re going to see some crossover as we talk about how that has impacted your financial plan. So Kara, let’s start with you. Tell us about your journey thus far since completing your PharmD at Ohio Northern.

Kara Soppe: So I graduated from Ohio Northern University in 2019, so it was a little over a year ago. And I landed a PGY1 pharmacy practice residency at Kettering Medical Center in Dayton, Ohio. So I completed that over the last year. And then fortunately, during COVID, I was able — there was an open position at Kettering, and I was able to stay on as a staff-clinical hybrid pharmacy specialist there. And that is the role that I’m continuing in. I’ve been in that role for about 4-5 months now.

Tim Ulbrich: Great. And Josh, how about you?

Josh Soppe: I graduated from Ohio Northern University in 2018, so a year before Kara. And I opted against a residency at the time and took a pretty unique job working on the pharmacy billing or insurance claims side of things and did that for almost two years. And then took on this new job working in the hospital on clinical informatics.

Tim Ulbrich: Very good. So you guys have been out of school for a couple years now, a little over a couple years, Josh, a little over a year, Kara, finishing up your PGY1 residency and now in your hybrid clinical specialist role. And so I think when folks hear that and they’re like, wait a minute, 2018, 2019, and you paid off what? How much? And how were you able to do that? So we’re going to dig into that. I first want to start with — and I’d love to hear from both of you. Josh, let’s start with you and then Kara, we’d like to have you follow up as well, when you talk about and think about that kind of a debt load, $188,000, which to be fair, for two pharmacy graduates, if we were to add together what would be the median debt load today for a class of 2020 grad, $175,000, and put that together, that’d be a little over, of course, $300,000, about $350,000. So here, together, you know, it’s a big number, but it’s a number that our audience is certainly familiar with probably from their own situation. So Josh, when you think of that number and that journey, talk to us about what your feelings were towards the debt, not only during repayment but also while you were in school and while you were in that accrual phase, whether or not it was something that was really, really top of mind for you.

Josh Soppe: I can say that being aware of that debt load — oh I guess first of all, I want to say that for us each being at about, well, together at about $180,000, we’re very fortunate to be in that position. No, I do want to say that speaking of the debt, I was aware of it before I even started applying for colleges back in high school. And I didn’t really have a full understanding. I just knew that student debt could be a big problem for a lot of people. And I took that into account when I was choosing careers and choosing university. And so throughout college, I paid very much attention to some scholarships or grants, tuition raises through every year, and made sure that I was working all the way throughout all six years of university. I took on a position in residence life and did my best to put myself in a position to get paid more and compensated more so I could minimize that debt load throughout school.

Tim Ulbrich: And Josh, I can’t remember if we talked about this before, but I also had some time in residence life at Ohio Northern. So fellow RA nerds here talking personal finance. So exciting times. Kara, as you looked at that debt scenario — and obviously as you guys began to tackle that as a couple — tell us about your feelings toward the debt, both while you were in school and then as you went through active repayment.

Kara Soppe: Yeah. When I started college, I don’t think the number had hit me quite yet. When I was in high school, you know, I’d seen the numbers, it didn’t really impact me that much until that first loan installment dropped. And I was like, oof, yikes, now I have this behind my name. So I thought it would be really important at least — and I always heard that your interest that you get in school will capitalize with your principal when you graduate after a few months, and that terrified me a little bit. So kind of similar to Josh, I had that mindset as like, I need to do stuff now to try to reduce my debt load and to make it easier when I graduate. So when I graduated, I was ready and I was prepared and the number didn’t scare me so much. And just like Josh, I also worked. I was a pharmacy intern throughout school, and I also was in residence life as well, which significantly helped us reduce the amount of debt load that we would have had because we were able to get some of our room and board paid for by those needs.

Tim Ulbrich: Yeah, so what I heard there, Josh and Kara, which I think is a good reinforcement is you know, yes, you had a big number to work with, $188,000, but through work, through residency life, through minimizing some of the housing expenses, through scholarships and other opportunities, you’re able to do whatever you could to keep that amount in check or I guess as at least in check as possible just given the reality of two individuals going through a doctorate pharmacy program. And that’s one of the messages that I often will try to reinforce to students is that as I’ve said on the show before, this can easily feel like Monopoly money. And there’s a certain point when you get to what can look like or feel like a point of no return where hey, I’m already $150,000 in debt, what’s another $10,000? What’s another $15,000? Or what’s another $20,000? And I think you see this often happen with experiential training year where expenses go up, may not be able to work as much, housing expenses might go up, travel expenses, interviews, and so on. And so I think this is a good reinforcement in your story of trying to do everything that you can, even if it’s multiple things that may not feel like any one of those has a significant impact in and of itself that collectively, they can help give that student loan debt number and keep it as low as possible. So Kara, I want to start with you — and Josh, please chime in as well — you know, one of the things that I always like to ask folks before we talk about OK, what was the budget, how did you do it, tell us about the strategy, is what was the reason? What was the rationale? What was the why? What was the motivating factor for you guys to say you know what, we want to go after this $188,000 of debt, and we want to do it really aggressively. Here again, we’re talking about 27.5 months. And so you could have taken this out 20 or 25 years, have a low monthly payment, probably refinance to a low interest rate, and moved on with other priorities. So what was the motivation? What was the why behind your aggressive repayment?

Kara Soppe: There were a few key principles for us that are very important, especially when it comes to our values that contributed, just aside from goals. So we had to consider our goals and our priorities. I mean, that was huge. So during school, as Josh and I were working toward a marriage, we were having open conversations about what our goals were going to be, and we both are actively involved in our church, and that was huge as well. We wanted to be able to be financially free from debt so we can be able to tithe and to give. We also wanted to make sure that we would be in a position to be able to support a family and to one day we want to — we felt like on our hearts, it was a calling to not only have biological kids but we also want to get involved with foster care and adoption. And then something more recently that we had discussed in order to maximize our income a little bit is we want to get into real estate investing. So these are goals and priorities that we had started developing in school. And now we have further developed those. But the key underlying principle for us to make sure that those things happen is that we didn’t want to be — there’s a phrase in Proverbs of the Bible that says, “The borrower is a slave to the lender.” And although we had lower interest rates on some of our loans, financial advisors probably would advise us to maybe take a step back, it was more important for us to be able to have flexibility in the end versus having some of the luxuries that we could be having now, which there’s nothing wrong with that. It just wasn’t necessarily a goal of ours was to be able to right now, you know, save up for a house or to get a new car or things like that. So it was flexibility was big for us. We wanted to have that flexibility to be able to do the things we want to do.

Tim Ulbrich: And Josh, were you and Kara always on the same page about that? Or how did you as a couple work through to identify what the shared goals were, which ultimately determined how you were going to handle these student loans.

Josh Soppe: These conversations really started while we were dating. And we were generally on the same page as far as yeah, we don’t want to be strapped with student loans. And I guess the only difference we had to deal with was how we were going to get there and how aggressive we were going to get there. We kind of had to tune in and sync up with the exact steps that we were going to take to tackling the debt.

Tim Ulbrich: Tell me more about that, Josh, when you say kind of determining how aggressive we may or may not be. Are we talking about, you know, big differences of low monthly payments, long repayment? Or it’s a matter of hey, 27 months versus 36 months and being able to prioritize some other things if we cool off the aggressiveness of that?

Josh Soppe: I think a lot of it just had to do with the sacrifices, really, the sacrifices we would have to make and what level of standard of living that we were agreed to live with during the amount of time that we would be in loan repayment.

Tim Ulbrich: And then talk to us, Josh, about the strategy. Did you guys stay in the federal system and just make extra payments and cut down that amortization table and obviously get them paid off? Did you refinance them? What was the strategy to actually execute on this aggressive repayment.

Josh Soppe: As far as the actual repayment goes, we went after the mathematical approach. So we went after the highest interest rates, which were also the largest portion of our student debt. And so we refinanced basically all of our student loans, and we did it multiple times. We went after the rewards that YFP gives when we sign up for the student loan refinances. And we were able to take out some other expenses and throw some more money right back into these loans using those bonuses.

Tim Ulbrich: I call that the Tim Church refinance strategy, the multiple refinances. And you know, just so our listeners are aware — and I always like to make sure people understand that when it comes to choosing your loan repayment strategy, there is no one right path. And it really comes down to, you know, determining all of the options that are out there and available to you, then aligning with your goals, with the math, evaluating those options, evaluating the current scenario. So here we are in November of 2020 where we have kind of a uncharted territory with the COVID-19 pandemic and the CARES Act where there’s a freeze on federal loans and interest rates, so obviously refinancing in the moment for those that have federal loans doesn’t make a whole lot of sense, if any sense at all. But obviously for you all, that decision had already been made and re-refinancing obviously could have had a positive impact. And so you know, Kara, as you reflect back on this journey, $188,000 in 27.5 months, there had to be sacrifices that were made in being able to do that. So talk to us about what those sacrifices were and then how you were able to evaluate and determine that ultimately was worth those things to be able to get these off your back.

Kara Soppe: Sure. I had mentioned before that for us, we wanted to — flexibility was more important than having certain luxuries. So when we were developing our budget, which we started doing that once Josh knew where he was going to be after graduation. We were able to get his salary, so we knew how much money we had to work with. But we had determined that we would get a lot of like — because we needed to somehow get stuff for an apartment and we needed to find a place to live, and we had to determine what our rent was going to be. But ahead of time, we had determined how much we had wanted to spend on rent. So we were able to do that. But just some other sacrifices we had, like we didn’t really get entirely new stuff for our apartment. We got a lot of furniture for free. So we had looked — luckily, Josh’s parents had a lot of stuff in their basement. So although it wasn’t the nicest stuff, we were able to furnish our apartment that way. And the stuff worked, so that’s what mattered to us. So that was one sacrifice we made was not buying brand new stuff to furnish our apartment. Another sacrifice that we made included how we decided we were going to spend money on groceries. Instead of eating out, which is definitely convenient, those costs can get really expensive. So although it’s more convenient, it’s cheaper to buy groceries, especially when you shop at Aldi. And we are huge Aldi shoppers. We still shop at Aldi, even after paying off our debt, because we had seen the food’s still good there, and it’s cheaper, and it helps being able to not eat out as often and be able to spend that money on those groceries. We’re able to use our money for other things. So those are two big things that we did. A couple other limitations that we had were to limit our costs on entertainment, and then we wanted to make sure that we maintained cars we already had. So I still have my first car that I ever had. It’s a 1999 Saturn SC2.

Tim Ulbrich: Wow.

Kara Soppe: And it’s still going strong.

Tim Ulbrich: Do they make those anymore?

Kara Soppe: No.

Josh Soppe: No.

Tim Ulbrich: OK, yeah.

Kara Soppe: So I had bought it for a good price, and it’s still running. And although the mirror on the side is taped up, actually both mirrors are taped up, I still drive it around, and it still works. And then Josh drives a 2009 Honda Civic, and that has about 187,000 miles on it. But that car is going strong as well.

Tim Ulbrich: So Josh, you’re driving around the — what looks like relatively the brand new car, 2009, relative to a 1999.

Josh Soppe: Right. Spankin’ new.

Tim Ulbrich: Brand spankin’ new. So what did that look like, Josh, you know, in terms of for the two of you, the budgeting process. So you know, we often talk about when one is choosing a student loan repayment strategy, especially if you’re going this route where it’s aggressive debt repayment, you’ve gotta be able to know how much can we put toward these loans each and every month? Because obviously you want to know if you can make the minimum payment but here, also make extra payments, to then be able to determine what is the payoff timeline and so forth. So in order to do that, you’ve got to have some type of budgeting system, whether that’s very well defined or more loose in nature that can help you determine what that number is. So talk to us about the system that you and Kara used for budgeting and then how that ultimately led to determining what you were able to put towards your student loans each and every month.

Josh Soppe: We used a tool called Mint you can find on Mint.com to help us with the budgeting. And as far as the approach that we took for paying off our student loans and reaching our financial goals, we first kind of looked at obviously our big life goals, right? We started there and looked at the big picture and started whittling away and going into more and more detail. So we specifically for paying off student loans, we thought, we figured out, OK, so how soon do we want to have these paid off? And of course, the answer is as soon as possible. So after that, then we looked at the budget and kind of looked at, OK, so how much does it cost to at least get by with the minimal standard of living that we’re willing to have and kind of estimated everything from there. And as far as looking at the budget, the best thing to do with at least lowering costs is to start with the biggest expenses and move down to the smallest expenses. So the biggest one would be housing. That’s typically the biggest one for most people. Second is transportation or a car if that’s something that you do. And then third for us, at least, was food. So that was the next highest one. And of course, charity you can throw up there if you decide to do that. And then whittle around from there with utilities and bills, gifts, and other things after that. So we kind of, we started with those large expenses and tried to whittle those down as much as possible. And that’s when we had a better idea, OK, so this is — these are probably the expenses that we’re going to have per month. And once we get that number, we’re able to project how soon we could pay off our loans and then we decided whether or not that’s something that we’re going to go with. And so eventually, it came down to that and came around to a projection of about two years, so about 24 months. And with changes over the two years, it ended up being 28.

Tim Ulbrich: And I like what you just said there, Josh, about being able to project the payoff date because I think when you’re trying to achieve any big financial goal, here we’re talking about debt repayment, the same could be true for saving for a house, the same could be true for saving for a longer term goal such as a wedding or an adoption of a child or whatever be a big monetary goal that’s off into the distance, it can be very easy to lose motivation along the way. And you can start on that journey, but you want to have some accountability to help you one, stay motivated, see progress, but also make sure you’re aligning and fitting it in with the rest of your financial goals and of course those things you’re having to spend money on each and every month so that you can make sure it’s prioritized. So Josh, you mentioned there at the end that you had a 24-month goal, obviously it went to 27.5 months, still incredible, but because of some circumstances along the way that may have impacted that. And one of the things that you shared with me is that you mentioned that as a part of this repayment plan or journey, of course we had a year of residency, which we all know — I know from firsthand experience, many of our listeners know — means a lower income period earning income for Kara during her PGY1 but also that you experienced a 40% pay cut while you were on this journey. So tell us about kind of the background of that story, where that pay cut come from, and how that may have derailed your plan but you were able to kind of reshift things back, even if it meant a little bit of a delay to ensure that you stayed focused on this goal of debt repayment.

Josh Soppe: So part of going back to looking at financial goals, what I mentioned, like looking at things big picture, thinking about life goals, right? I had always had a liking towards computers and IT, Information Technology. And with pharmacy, as many people know, right out of school, there really isn’t a place to go with that. It’s very difficult. And so when I first got out of school, I took a job that was like the closest thing that you could possibly get to it, get to working in IT, at least had opportunities for me to make some changes and make some moves using my IT skills. And so when an opportunity came up nearby, locally, for me to take to get into informatics, which I had taken a liking to, I applied for a pharmacist position there and ended up getting a position on the pharmacy IS team, not as a pharmacist but as an analyst with the goal of when they expand the team or a position opens up, I would at least — I would have the skills and the experience to move in that way. So in some way, you could look at it as that right there, what I’m going through now, is my residency. Taking that 40% pay cut, which ended up being about $50,000, that was I guess an obstacle that we were willing to take for me to be in a position that I could see a lot of growth in and a lot of satisfaction.

Tim Ulbrich: So Josh, as you share that 40% reduction in pay, obviously that’s a significant dollar amount, and you mentioned that your projected timeline of payoff was 24 months, obviously that got extended a little bit to 27.5, round up 28 months. But in the scheme of things, 3.5-4 months, no big deal. So did this change, which had better alignment of your interests career-wise although it resulted in a reduction of pay — did it have a significant impact on actually delaying your aggressive debt repayment? Or was it more of a mental mindset and a hurdle you had to get over to say, yeah, it’s a step back, but we’re going to stay on this path toward aggressive repayment?

Josh Soppe: I think for us, it definitely was a look into the future and looking at long-term investment into this kind of pay cut. And of course, the number — the way the numbers work out, it was going to take a little bit longer to pay off those loans. And we had looked at like is that something that we’re willing to do looking at the long-term payout from the potential of me moving into a position that I am in now. And I think for a lot of people and what we looked at it was to weigh the risks versus benefits. And we saw that the benefits of this job change to heavily outweigh the risks.

Tim Ulbrich: And speaking of benefits, Kara, you know, when I think of this type of debt load, $188,000 over 28 months, if anybody’s doing some quick math here — hopefully not while they’re driving — that’s a little over on average, $6,700 per month over 28 months. Obviously it may have been higher or lower some months to get that debt load paid off. So you know, one of my questions here, speaking of benefits, is well now you don’t have to make that payment. Now you don’t have to make a $6,700 a month on average payment, which means coming full circle, we can start to invest those monies towards the other goals and priorities you had mentioned in terms of your goals of your own family and fostering and real estate and saving for retirement. So how does that feel, Kara? And what is ahead for you guys, you know, kind of month by month here as you look forward of how you’re going to reallocate these dollars that were going toward student loans that you can now put towards other goals?

Kara Soppe: Yeah. I mean, it feels great now that we have that money freed up. It’s still — it took a couple months I think for it to fully hit us that we are able to use that money for other things and to finally start achieving some of those other goals. But we had to go back to thinking well, if we didn’t pay off our debt so early, we wouldn’t be here in this position to be able to start working toward these other goals. So out of those goals that I had mentioned earlier, we think the key thing first to be able to start getting those in place is we’re actually starting to save up for a down payment on a house. And we had a goal to start shopping around for a house by late winter, early spring. So the fact that we have about $6,000 freed up each month to be able to do that is huge. And now, since we went so aggressively toward our student loans, now we can kind of start not just focusing on one goal. We can start focusing on multiple goals at once, which is what most people do throughout their lives as they’re raising kids and they have a house to finance and they have other things they’re saving up for and then going on vacations, things like that. So that’s a huge thing. And then we also want to — which we haven’t started doing this yet — but we also want to contribute to an adoption fund that we had already gotten started. Instead of for our wedding, instead of doing a wedding registry, we actually set up an adoption fund. So we want to start contributing to that more. So we are going a little aggressively saving up for a house quickly. But we believe that doing so will allow us to open up the opportunity to own an investment property, to start having — we want to be able to have a good place where we have space to have a family. And then when we are considering — another thing that I want to mention in terms of what we are looking for in a house is it’s not our end-all, be-all home. We actually want to consider that using that property eventually as a rental property. So getting this house is one step to be able to do that. Now, we’re still talking about whether we want to purchase like a duplex where we live on one side of it and then we rent out the other side or we purchase a property where we live in it temporarily, we kind of remodel it a little bit to be able to rent out eventually, that we’re not entirely sure yet. We’re still having conversations about that. But this is a huge step for us to be able to reach that goal as well.

Tim Ulbrich: That’s awesome. And I love the intentionality of kind of what you guys have in mind, and I can tell there’s been lots of discussions about where you’re going to be putting that money and how you prioritize it. And I’m sure that will be an evolution over time, but nonetheless, the open communication and these conversations are so important, not only through debt repayment to stay motivated but also post-debt repayment to make sure that you’re being intentional with the dollars that were going towards debt that you can now allocate towards the rest of your plan. Josh, one of the questions I’d like to start with you — and Kara, I’d like to hear from you as well — I like to ask is, you know, we know, I know from being married for — we just celebrated, my wife and I, our 13-year anniversary — this topic is difficult to handle, even in the best of marriages. And I think for obvious reasons, we’ve all heard the statistics before about couples and finances and so forth. And so I’d like our listeners to get an inside look to for you and Kara, you know, the system that has worked for the two of you — and I always say there’s no right or wrong answer here in terms of, you know, is it shared decision-making, is it one person taking the lead, whatever that looks like for the two of you. But what has worked, perhaps, for the two of you? Obviously something has worked here. And if you’ve had any lessons you’ve learned along the way, maybe things that didn’t work and how you guys have pivoted.

Josh Soppe: Alright. So for the last two years, our approach obviously before we get married, we already started having these conversations. That was very important for us to agree, hey, this is kind of how we want to handle our finances in general, right? But as far as the details go, the last two years, I have mostly taken the lead on actually dealing with the numbers and looking at our options. And I would look at our options, the different ways that we could go or that we might be interested to go, kind of listening to what Kara is thinking, and I’d put that into numbers and projections. And once I get those numbers and projections, then I bring it back to her and kind of talk to her like, hey, is this — “I kind of want to take this route. Would you — what do you think about that versus this other route?” that she might want to work with. And so we’ve had to kind of just constantly have those talks either weekly or monthly. And it’s become less and less frequent as we have a better idea, like hey, here’s our big stuff, we’ve kind of got a routine with it. But that’s how we started and making sure that we come to an agreement with how we handle our finances.

Tim Ulbrich: Great. Kara, anything to add there?

Kara Soppe: I think in summary, we really wanted to focus on stewarding our finances proactively. So especially in the beginning as we were starting to join our lives together, a lot more of those conversations had to happen. And I think personally, I — Josh and I are both very frugal. But Josh is definitely more frugal than me. And I have a little bit more of a tendency to want to spend a little bit more money than he would. But I appreciate that we were able to have those conversations because if we didn’t, we wouldn’t have been able to hold each other accountable and keep each other on track. Intentionally setting aside time to discuss our financial plan was huge. And the earlier on that we did it, the better. And I say that for listeners, for students, for new grads, for even pharmacists out there who are trying to look to achieve this kind of goal and actually want to start aggressively tackling their debt, like it’s not too late to start. It can start now. But you know, the earlier, the better. It will definitely help you achieve your goal sooner. So I just want to encourage people to make sure that they have a level of communication with their spouse or their family; that played a huge role for us.

Tim Ulbrich: Great advice. And I appreciate you both sharing there. And I think your story, as I mentioned at the beginning, is going to be an inspiration to many. And so I appreciate your time coming on the show to share your story of paying off $188,000 of student loan debt in 28 months. And really, I’m excited for what that means for the two of you going forward. You mentioned obviously working on a down payment for a home, you mentioned the adoption fund, you mentioned the real estate investing is a priority, and I’m sure there will be other things that will come for you guys in the future. So again, congratulations. And we’re excited to be able to share this story with the YFP community. And to our listeners, we thank you again for joining us on this week’s episode of the Your Financial Pharmacist podcast. And for those that are hearing this wondering, you know, do I have the optimal student loan repayment strategy in place for my own personal situation, make sure to check out a lot of our resources that we have on the website but also the “Pharmacist’s Guide to Conquering Student Loans,” our newest book written by our very own Tim Church, available at PharmDLoans.com. And if you haven’t yet done so, please leave us a rating and review on Apple podcasts or wherever you listen to the show each and every week so that other pharmacy professionals can find the work that we’re doing and the community is doing here at Your Financial Pharmacist. Have a great rest of your week.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]Recent Posts

[pt_view id=”f651872qnv”]