How to Reduce Costs During the Residency Application Process

Sarah Cummins, a PGY2 Emergency Medicine Pharmacy Resident, joins Tim Ulbrich to talk about specific strategies to make the residency application process more affordable.

About Today’s Guest

Dr. Sarah Cummins is a PGY2 Emergency Medicine Pharmacy Resident at the University of California Davis Medical Center in Sacramento California. Prior to this position, she completed her PGY1 residency at Thomas Jefferson University Hospital in Philadelphia, PA and earned her Doctor of Pharmacy degree from Purdue University in West Lafayette, IN. Dr. Cummins’s clinical/research interests include trauma resuscitation, acute pain management, optimizing healthcare access to underserved populations, minimizing healthcare disparities in BIPOC, and emergency department transitions of care. When she isn’t working, Dr. Cummins enjoys hiking, caring for her blind dog named Muffin, reading novels, and any sort of activity that takes place on a patio.

Summary

Sarah Cummins, a PGY2 Emergency Medicine Pharmacy Resident at UC Davis, is passionate about helping other pharmacists reduce the cost of the pharmacy residency application process. Although Midyear and interviews may look a bit different during the COVID-19 pandemic, the tips Sarah shares are still powerful ways to save money.

Sarah breaks her tips into six categories: how to save money before interviews, Midyear, travel, eating, where you should spend your money and some general advice.

Prior to sending in applications or going to interviews, Sarah says that you first have to figure out your goals and create and execute a budget to help you reach them. For example, she suggests beginning to save during your P3 year and to ask for gift cards from family and friends in lieu of material items so that you can purchase professional clothes or other necessities.

Midyear is virtual and free this year due to COVID-19, however it’s normally $340 for a student member and $480 for a non-member. Sarah explains that Midyear is usually in an expensive city, meaning you should really do your best to save money on other expenses like food costs.

Sarah explains that there is the potential to save the most money with travel expenses if you’re willing to put the time and work into doing so. She shares that you have to put all methods of travel into a side-by-side comparison so you can see which method or hybrid of methods is going to be the cheapest. It’s easy to spend a lot of money on food and coffee while you’re traveling. Instead, Sarah suggests packing granola bars, packaged foods and drinking the in-room hotel coffee to save some money and time.

While there are many aspects of this process that you can save money on, Sarah explains that you should spend money on things like professional clothes you feel confident in and to make sure you’re staying at a comfortable and safe location.

Mentioned on the Show

- Compare Multiple Lenders and Refinance Your Mortgage with Credible

- Sarah Cummins’ Tips for Making the Residency Process More Affordable on Twitter

- ASHP Midyear 2020 Clinical Meeting & Exhibition Registration Information

- ASHP: Become a Member

- Gas Price Calculator

- Tollsmart

- SpotHero

- MegaBus

- Follow Sarah Cummins on Twitter: @sc_pharmd

- Join the YFP Facebook Group

Episode Transcript

Tim Ulbrich: Sarah, thank you so much for taking time to come on the show.

Sarah Cummins: Thank you so much for inviting me. I’m happy to be here.

Tim Ulbrich: So our conversation began over the summer on LinkedIn, and I knew what you shared would fit so well in the fall as P4s are gearing up for the residency application process and really also for preceptors that are listening, faculty members that are listening, that they can also share some of this information with the students that they may be mentoring, coaching, helping along the way. And before we dig into your tips and tricks for making the residency application process affordable, I’d love for you to share a little bit about yourself. So tell us about your pharmacy career, what led you ultimately into pharmacy and how you’re able to determine the path that you want to take in terms of residency training.

Sarah Cummins: Sure. So I started out at Purdue University in Indiana, which is where I’m from.

Tim Ulbrich: Go Boilermakers.

Sarah Cummins: Yes, yes. So I grew up in Indiana, went to school there, then I did my PGY1 residency in Philadelphia, Pennsylvania at Thomas Jefferson University Hospital. Then I drove 3,000 miles across the country to go the UC-Davis in Sacramento for my PGY2 in emergency medicine. I think I originally got into pharmacy because the same reason that many of us do — because we’re nerds and we like science and we like helping people. And I really liked the aspect of this career where I felt like I could make a difference in patients’ lives face-to-face, talking to them and helping them manage their diseases versus some of the other healthcare professionals where you don’t get as much face time as you do with pharmacy. And I really liked that.

Tim Ulbrich: And when did you know emergency medicine was the path that you wanted to take?

Sarah Cummins: That one was a little bit of a quick decision. So I had originally thought I was an infectious diseases person all the way. I love ID. I did my bachelors in microbiology and biochem. I had done ID research. I love bacteria. I think they’re so cool. But then I did an APE (?) in the emergency room, and I was a little shocked at how much I really enjoyed it. So then I started second-guessing myself, wondering if maybe I was an EM person instead of an ID person. I did an EM rotation during my PGY1, and that kind of sold it for me that I was actually an EM person instead of an ID person. I think I made the right decision. I feel very at home, I feel like this is my niche. And I’m really excited to go to work every day, and I think that that’s all we can really hope for with careers is just being really happy with what we do.

Tim Ulbrich: Absolutely. And the irony — you know, we’ll talk obviously about mindset around spending and frugality — and the irony that you ended up in California where cost of living is high, but thankfully you had some behaviors and strategies in place that could help you manage some of that. And really, what I want to spend our time on today is that you had tweeted an amazing list of topics about how to make the residency application more affordable, where folks should consider spending money, where it’s worth it, cutting where it’s not, and some general advice to those that are starting this process. And you know, I should mention, disclaimer here, we are obviously fall 2020, given the situation with COVID-19, you know, this residency recruitment-application-interview cycle, it’s going to look different than any other one that we’ve had before. And so some of that we don’t yet know at this point, some of it we do in terms of things like ASHP Midyear of course being virtual. Will all interview be remote? Will some be on site? I think it’s probably leaning towards remote but certainly that’s a ways off as we think about the February and March timeframe. So for those that are listening, you know, P4s applying this year during the spring 2021, going into the match that starts July 2021, obviously we’re a unique situation, but we expect others in the future, we might be back in more that traditional environment. So before we get into these strategies that you mentioned, one of the things I was asking you before we hit record — and really, one of the things that impressed me when I first ran across what you shared on this topic is I could tell you had really an intentional mindset around your finances, but specifically, you had a mindset around being frugal. And I think here, it’s important that we’re talking about places where it’s important that we think about cutting but also places where we think it might be important to spend some and that that’s OK where it’s worth it. So where — my question is where does that frugal mindset come for you? Where did that start?

Sarah Cummins: That is such a great question, and I don’t actually have an answer for you. I don’t really know. There isn’t one pivotal moment in my life where I learned this. No one really taught it to me. I think it came from pressure of not having financial resources as a student and not having support with family, friends, and whatnot financially going through this process. I’ve always been the kind of person that I don’t do anything halfway. If I’m going to do it, I’m really going to do it. And I put a lot of work into figuring out exactly how I could afford this because my resources were very limited. I made a goal to go to Midyear, I made a goal to apply to the programs I wanted to all over the country, and I planned accordingly to make sure I could do that. And I think the skill that I learned from that that was very difficult for me to understand at first and I think very difficult for a lot of people who are financially limited is to plan ahead. So many times, you know, when we don’t have resources, we don’t have a lot of money, we just think about the here and now. How am I going to afford my bills this week, this month? Where can I cut costs on my groceries this week? But I’m not thinking about what I’m going to be paying for eight months in advance. And that’s something that’s kind of a difficult mindset for people to adopt when they’ve never really had to do it or where they’re always in this fight or flight mode on how they’re going to survive each week. So that was something I really had to push myself to do.

Tim Ulbrich: Yeah, and that’s great input. As we talk often on the show about the intentionality of the financial plan, thinking ahead, planning ahead, thinking long-term, which is hard, especially when you think about in the position of a student where you obviously have a limited income and certainly may be in a debt accrual with student loans. And so as you put together the time and the effort to share this list out, what were some of the motivations of doing that? Obviously it was near and dear to you and your own plan, but did you also see others that were struggling with it?

Sarah Cummins: Absolutely. So I saw a lot of students posting on Twitter, residents posting on Twitter, just kind of venting how frustrating it is that this process is so expensive, sharing how difficult it is to afford this, sharing their fears. And I really just wanted to provide a little bit of hope and a little bit of encouragement to those students who are in the same situation that I was in where you have to really work a real full-time — or I mean part-time job to fund your expenses. And I think that the post definitely achieved that. A lot of people messaged me, sharing their thanks for just reaching out and saying, “Hey, it’s possible. It’s hard, but it’s possible.”

Tim Ulbrich: And I’m so glad you did, Sarah, because as you know, as I know living through it, as our listeners know living through it, P4 year, that final year is often when things fall off the tracks financially, right? So you’ve got — you know, obviously you’re in a transitionary year, so depending on where you’re doing your rotations, you may be going out of the area, you have additional transportation expenses, additional housing expenses, you may need additional professional clothes, other things. Expenses add up. Obviously busy hours, you tend to maybe have to eat meals on the go, so you have lots of expenses that come with rotations. But then you also have many schools, the tuition and fees are higher in the fourth year when you’re doing experiential rotations and then on top of this, you have — whether it’s residency, a job, combination of both — you’ve got the additional expenses that are associated here. So I think sometimes I see — and I don’t know if you saw this with your classmates where — you know, I see this among students where they’re like, my gosh, I’m already $160,000 in debt, like what’s it matter at this point, right?

Sarah Cummins: Yeah, just add it to the tab.

Tim Ulbrich: Yeah, and I think again, what we’re talking about here is whether it’s $100, $1,000 or $10,000, the intentionality and the mindset and having really the processes, whether it’s a budget, this long-term thinking, to really be able to see the benefits of this and other parts of your financial plan in the future are really important. Do you — just as a general ballpark, what do you think on average students are spending when you think about the residency application process? I mean, you’ve got the applications, you’ve got Midyear, you’ve got travel, you’ve got professional clothes. Like what do you anticipate that number is?

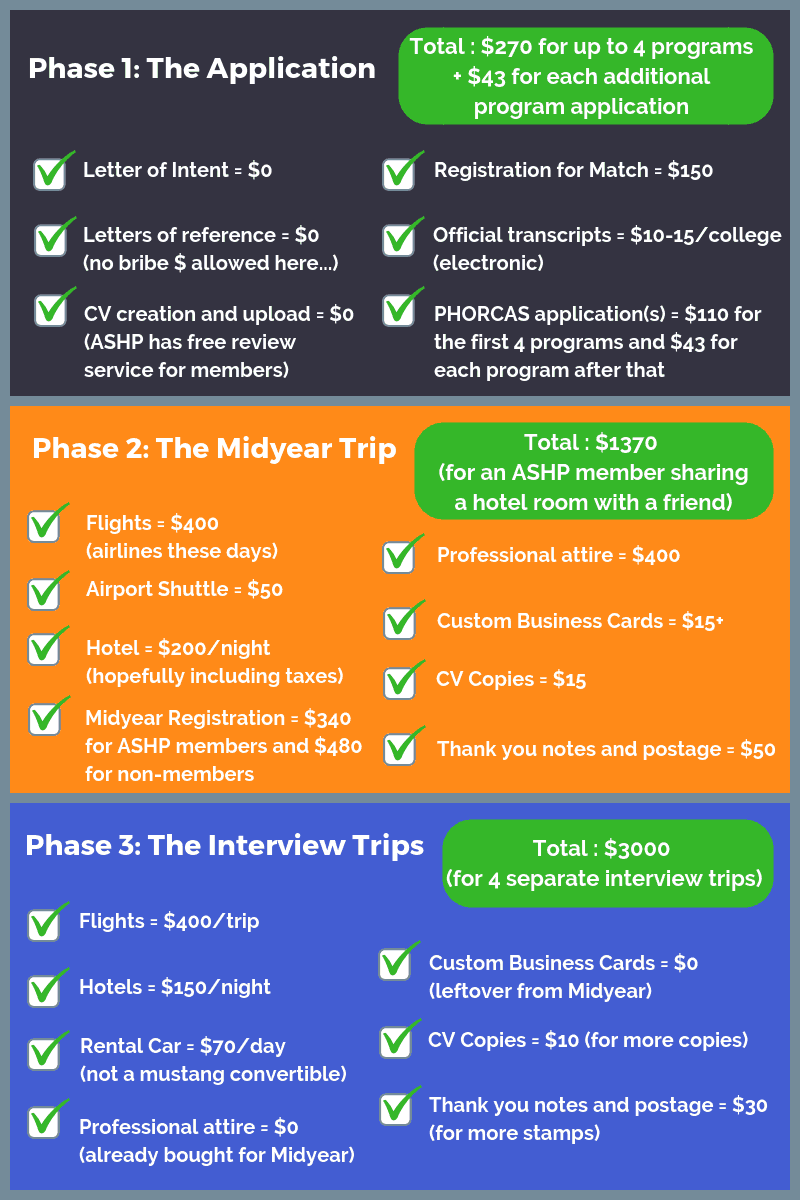

Sarah Cummins: Thousands. I know it’s thousands. It’s definitely different for each person, so going to Midyear in and of itself is very expensive. So if for whatever reason you don’t go to Midyear, you can cut a large portion of that out. But even the application is expensive. So the NMS match fee is $160. The forecast fee is $110. That gets you four applications included. So if you want to apply to more than four programs, you’re going to be paying $43 apiece for every additional program. So just to submit your applications, if you want to apply to 10 programs, which is what I feel like a lot of students do on average is $528 just to try.

Tim Ulbrich: Yeah, and as we know, if that is borrowing money, it’s going to cost more at some point, right? It just accrues and things into the future. So we’re going to go through, as I mentioned, you put together this list and you broke up these tips into six main categories. No. 1, how to save money before interviews. No. 2, things to think about at Midyear. 3, on the traveling side. 4, eating while you’re traveling. 5, where you should spend your money, so essentially permission granted, where it’s worth it. And then 6, some general advice. So let’s start with this first category, prior to interviews. And you start off by sharing some advice for people before they even send applications in or have interviews lined up. So what’s some of your advice here? And why is this important?

Sarah Cummins: So I think that this is actually probably the most important part and where you could potentially have the most cost savings because I think the first thing you need to do is figure out what your goals are. You need to figure out if you are going to be applying to programs near home, if you’re going to be looking all over the country, and then you need to make a plan on how to budget for that, how much money you can expect to have to pay and then execute that plan. So I think for a student that is — I’m going to just pick the most expensive example. So let’s say you just, you really want to do it, you’re going to apply all over the country, you’re going to go to Midyear, you’re going to go all out. Start saving early, like P3 year early. One thing I did, if you have anybody in your life that likes to buy you birthday gifts or holiday gifts, ask for gift cards. So I asked for gift cards to Macy’s department store because I know that they have a pretty good selection of suits and business clothes. And they also have pretty good sales sometimes. So I asked for gift cards early on during P3 year so that way I could start to collect a wardrobe, some nice shoes and some other things to wear to Midyear because if you wait until the last minute to do that, that’s just going to be another expense added on top of it if you don’t plan on anything to wear to these interviews and PPSs. Another thing is just registering for Midyear is expensive. So as a student this year, it is actually free because of COVID, which is incredible. Snaps to ASHP for that. But last year and every other year, it’s not free. So the registration fee is different depending on whether you’re an ASHP member or not. If you’re a student member, it’s $340. But if you’re a non-member, it’s $480. And this is a really easy place to save money because if you just register for a membership, it’s $54. So you can save like almost $80 if you just do the membership and then apply as a student member instead of not being a member and applying as a non-member. So do your research on that, make sure that you aren’t paying more money for registration than you need to. The other thing with planning to go to Midyear is once you have everything that you need to wear and you have your plan, what kind of programs you want to start looking at and you are starting to think about flights and hotels and stuff, then that becomes a lot more work. And I think that is the most time-intensive part of this.

Tim Ulbrich: Great advice, Sarah. And one of the things I wanted to add here as you think about number of applications, in my experience working with students going through this process, you know, I’ve worked with some students that applied to one or two sites and to 22 sites and everything in between. You know, you mentioned 10 is a pretty good number that you see out there. I would agree with that. I mean, I think most students are probably applying to somewhere between 8-12 sites. But where I really am encouraging the listeners to think about is you have to do some really serious self-reflection to really identify what factors might determine how many sites you need to apply at. So you’re looking at obviously things like the reputation of those programs, how many applications might they be getting, how selective are they, geographic types of things, the cost that’s going to be associated with the travel, how strong of a candidate are you, how well-networked are you with that, have you worked there, have you had a rotation there? And all of those things should have a significant impact on how many sites you’re applying to. And I think there can be a challenge, especially for the all-stars out there that are listening, you know, those that have really strong connections, have done all of their things along the way well to make themselves a strong candidate, there can be a feeling in the moment of oh my gosh, match is so competitive, they look at the national match statistics, and then they apply to a bunch of places. For some, that’s necessary, and for others, it’s not. So I think really doing some reflection to determine what that right number is or working with some advisors at the college or others that can help you do that is really important.

Sarah Cummins: Definitely.

Tim Ulbrich: Let’s talk about Midyear for a moment. You mentioned the registration fee, which of course, obviously this year in 2020, we have, again, somewhat of a unique situation. But we know that’s just one piece of the puzzle when it comes to costs associated with Midyear. So talk to us about other strategies here that people can be thinking about for how to save money as it comes to Midyear. And here, obviously we’re talking about more in the traditional sense of in-person Midyear.

Sarah Cummins: Yes. So Midyear, historically, takes place in one of four cities: New Orleans, Orlando, Las Vegas, or Anaheim. So those are the only cities that have enough conference space to hold the vast amount of pharmacists and students that are drawn to these conventions. So this has been done before. People have gone to all of these cities before, found the cheapest place to live, there’s probably a lot of people who have advice out there. So any students that are wondering where the cheapest spots are, where you can get a good deal at, feel free to just tweet it out and ask, “Hey, who went to Midyear in Anaheim? Who went to Midyear in Orlando? What did you do?” And those people might have a little bit of advice to contribute. But something that all of these destinations have in common is they are expensive to go to. So one thing that’s really hard to budget for is all the food and unexpected costs that you’re going to accrue there. So you think about, OK, I’m going to pay for my hotel, I’m going to pay for my flight, I get there, then what? Sometimes that airport is a substantial distance away from where your hotel is. And those Ubers, Lyfts, can be $50-60 one-way, especially in some of the bigger cities. And this counts for interviews too. So one thing that I do is I do my research on the public transportation system. So a lot of — some of these cities don’t have a lot of great options for public transportation. But most of them have buses. And buses are cheap. They do take a long time, however, so if you can plan to have an earlier flight where you have a little bit more time to get to your hotel, look into getting a bus ticket for $2.50 compared to spending whatever the surprise cost of the Uber or Lyft is going to be because that is not a discreet cost. It’s going to be a random number, depending on how busy they are.

Tim Ulbrich: Yeah.

Sarah Cummins: Another thing that I spent more money on than I thought I was going to spend, even though I planned for it, was food.

Tim Ulbrich: Yes, yes.

Sarah Cummins: So you wake up in the morning and you’re in your hotel room, you’re starving, you just traveled all day, so what are you going to do? You’re going to go down to the Starbucks, get a coffee, maybe a granola bar or a muffin or something. And then it’s $12 because that’s what it is in Las Vegas. I paid for a banana that was $9.

Tim Ulbrich: And you have no choice.

Sarah Cummins: Yeah.

Tim Ulbrich: Yes.

Sarah Cummins: And that’s it because you’re starving, you’re exhausted, and that’s what you need. So something that you can do to mitigate these costs is to plan for being hungry. I called ahead to hotels to see if they offer in-room coffee because some of them have that cheap coffee that you can make just in your room.

Tim Ulbrich: That’s right.

Sarah Cummins: That’s great because it’s $0. It’s a little bit of an appetite-suppressant, so it can tide me over until I can eat breakfast somewhere. Also, if you’re going to be going to Midyear for a couple days, you’re probably going to check a bag, which costs about $30. But it’ll save you money in the long run versus just trying to shove everything on a carry-on bag because you can fill that bag with snacks and food. I put a couple boxes of granola bars, I had some Easy Mac cups because I called and asked if my hotel room had a microwave. And those — just having that little bit of food available was really a life saver because it saved me a lot of money, and it saved me a lot of time from having to go to a restaurant or wait in the ungodly lines at the cafes.

Tim Ulbrich: Yes.

Sarah Cummins: And you don’t think about that cost when you’re planning your trips. You just think about the major expenses. But that really adds up. I think I would say I probably saved maybe $200 just by planning for the coffee and the food alone.

Tim Ulbrich: As you’re talking, Sarah, I’m just — I’m smiling as you’re talking because I’m thinking of all of the Midyear meetings that I’ve been at as a student, as a new practitioner, on the other side interviewing, where some things — it’s like, it takes so long to learn some of those lessons. But where you’re standing in those long lines and you’re not only waiting but then you’re spending $20 for coffee and a muffin, you’re frustrated, and then you’re still hungry and you’re off sync with how you normally are and all of these things. So I think preparation here and planning is so important.

Sarah Cummins: Yeah. And the — I don’t know if I’m using this word right, the opportunity cost of when you’re very, very hungry is different when you’re not very hungry. So you’re more likely to spend more money on food if you’re starving versus if you’re not starving because you have more time to plan for it. Another tip that I have if you’re going to go to Midyear is this thing called the industry showcase. So at first glance, you might not think that that’s for you as a student because it’s basically a bunch of pharma companies and tech companies that set up booths to showcase their products. But this is an absolute gold mine for hungry students. Last year, I got free espressos, like individually wrapped sugar cookies, snacks, they gave out water bottles. So basically you just go up, you get snacks and food and stuff and just take a pamphlet, pretend to be interested, and then just go on your merry way. It’s incredible. So most students don’t venture in there because they don’t see a need to. They’re not a hospital looking for new technology. But are you thirsty? Do you want a free water bottle? Go for it, it’s great. You won’t regret it.

Tim Ulbrich: That’s great. I mean, the specific advice you have here is fantastic. You know, for the preceptors that are listening, they’re probably smiling as well. But I hope the students are taking notes. And these things add up. It’s a combination of planning ahead, it’s a combination of getting creative, cutting expenses while you’re there, and hopefully together, some of these will have a real impact. We’re really just getting warmed up, right?

Sarah Cummins: Yeah.

Tim Ulbrich: So we talked about the cost of applications, we talked about the cost of Midyear, which even in this year is of course going to be significantly different. But we haven’t yet talked about traveling. So when it comes to traveling for interviews, you know, I know for many folks this can look very different if they’re maybe just applying in one region where they live and their college is versus those that are looking across the country. So what pieces of advice here do you have in terms of traveling for interviews?

Sarah Cummins: I have a lot. And I think this is the piece of this whole thread and podcast that is potentially the most cost-saving. So it takes a lot of time to do this. But it’s really worth it in the end. You need to do your thorough research on the cheapest way to get to and from an interview or Midyear. So you need to look at prices of driving, flying and public transportation. So driving, estimate your gas costs. And don’t just like guess. You can go online and Google “gas price calculator” and figure out for the exact make and model of your car how much money you can expect to pay for what the current gas prices are because those fluctuate each year. Sometimes it’s very expensive, sometimes it’s not. Additionally, if you’re going to be traveling for several hours to wherever your interview site is, a lot of people use toll roads. They’re much faster, it saves time, but it costs money. There’s this website called TollSmart.com. And you can use it to calculate toll fees anywhere in the country. You just type in your start address and then your destination address, and it’ll show you the route that you would take using toll roads to see how much money that costs because who knows how much toll roads cost off the top of their head? I’ve never met anybody. I have no idea.

Tim Ulbrich: No.

Sarah Cummins: It’s just a guess, it’s a surprise. Sometimes you need cash, sometimes you can use card. No one ever knows. It’s just a big mystery.

Tim Ulbrich: That’s right.

Sarah Cummins: So if you plan ahead for that, for the gas, another thing you need to plan for if you’re going to drive is parking because a lot of times, hotel parking is not free. $40 a night, $60 a night, depending on where you go. In some of the bigger cities — and even in some of the smaller cities, you can use this app or website, it’s called Spot Hero. So you can just go to spothero.com, and basically what it does is it shows all the available parking spots in garages, in lots, and you can compare prices of how much money you’re going to pay to leave your car in that lot or that parking garage from the time that you arrive to the time that you leave.

Tim Ulbrich: That’s awesome.

Sarah Cummins: And it can be substantially cheaper than parking at your hotel. Another thing to do if you’re planning on driving is try to pick an interview day on a Monday or a Friday so that way Sunday you have plenty of time to drive and you’re not going to be rushed, especially if you’re going to be driving like 10-12 hours or something crazy like that. And then Fridays, you’ll have plenty of time to drive that evening or even the next day if you need to. So that’s always nice. For flying, the best case scenario is always to find a flight that arrives the day before the interview and then have a return flight right after the interview has finished, the next day in the evening. But that’s usually not the cheapest flight. So again, you’ve got to do your research. It might actually be cheaper to stay an extra day and pay another $80 for your hotel or Airbnb and then take the early morning flight the next day. I did this, and it saved me over $200 for one interview. And then the last mode of transportation is public transportation. Some places, they have trains that go in between big cities if you’re someone that’s coming from a big city. I was not. But Megabus is a life saver. Megabus, I love Megabus. Shoutout to Megabus, you’re awesome. You can buy a bus ticket on one of this double-decker bus, and they are cheap. They are — you can ride on a bus for nine hours for as low as $3.50 after taxes and fees. And I did this for one interview. I rode the bus for nine hours one day, and then went to my interview and then flew home the next day with a one-way ticket.

Tim Ulbrich: Oh, cool.

Sarah Cummins: And that saved me over $150 compared to doing a round-trip and flying on Sundays. Because flying on Sundays is so expensive.

Tim Ulbrich: Yes.

Sarah Cummins: There are also seats, there are eight seats on each of these buses that are — have a table in front of them. So you can have like a little cup holder and a table, you can get your laptop out and do some schoolwork or whatever you want to work on, prepare for the interview, while you’re actually on the bus, which is what I did. So it was a great, great use of my time. So then you can do a hybrid of these options. So you can look into the price of a one-way car rental to drive on Sunday, show up for your interview Monday, fly home with a one-way ticket. It’s a lot of work putting all these side by side for every single interview, but trust me, it’s so worth it.

Tim Ulbrich: And one of the things, Sarah, I remember you wrote about, which really resonated and I want to make sure the students hear is not being afraid to ask the site — whether that’s the RPD or somebody that they have delegated that responsibility of coordinating interviews, I think generally speaking, the sites want to be amenable and want to work with folks if it’s going to help save them money, time, coordination. So whether that’s stacking interviews if you’re going to be in a certain area so you don’t have to travel twice or I remember you had written about just a schedule and by asking a question, they were able to move something around by a half hour so you could take a flight out that day that was cheaper. So you know, I think being open — and obviously there’s a respectful, professional way to do that — but not necessarily feeling afraid to have some of those conversations that could have cost savings depending on the mode of travel and where that interview is taking place.

Sarah Cummins: Definitely. So I feel a lot of students don’t want to be the person that looks like they can’t figure it all out themselves and aren’t completely independent and savvy and they don’t need any help from the RPDs. But you know, they want you to be there. They want you to be able to be comfortable and to have plenty of time. I remember I emailed an RPD and I asked, “I know my interview ends at 4. There’s a 5 o’clock flight at the airport. Do you think I would have enough time to make it from the hospital to the airport and make that flight? Because it’s $200 cheaper than all the other flights. And I would like to save that money if possible.” Every person can understand this, so she was great and she said, “Traffic is minimal. Security is minimal. And I can bump your interview date up half an hour just to give you a little bit of extra time.” And it was awesome. So they’re experts. They live in that city. They know their way around. They know like don’t take this rail from the airport to the hospital because it’s generally not very safe, or don’t stay in this area or fly into this airport instead of the main airport because it’s a lot cheaper or faster. They have all these tips. They live there, they travel there. And I don’t know if I’ve met one RPD that would not gladly share that.

Tim Ulbrich: I agree. And as someone who has served on both sides of this in terms of the applicant as well as an RPD, I think often if schedules are sent, people are busy, they’re trying to coordinate a lot of things, and sometimes just somebody asking that, and they’re willing to work with it. So don’t be afraid to ask that question. Next category, we talked a little bit about this with Midyear and packing food, but eating while traveling. And I think this is obviously a piece that is often missed when thinking about saving money in the residency process. But just like if you were at home, eating out can be really expensive. So give us some general tips or thoughts that you have on how folks can save on eating and food expenses while they’re traveling.

Sarah Cummins: Definitely. So one thing I noticed that I didn’t really prepare for I guess when I was interviewing is that sometimes I would be interviewing on one side of the country one day and then a few days later, be on the other side of the country the next day. And those time changes are different. So I got hungry at very odd hours. Like I would wake up in California at 4 a.m. ready for breakfast and there’s no places that are breakfast because I’m used to that being 7 a.m. on the East Coast. So I always packed some granola bars, some packaged foods. I’m not going to recommend you check a bag for interviews just because that’s a wasted expense. So you can’t like make food like a sandwich or something and bring that on the plane. It has to be prepackaged. So I’m a big fan of those little packs of Goldfish crackers, again, mac and cheese noodle cups, those kind of things are always not a bad idea to have on board. But just making sure that you’re not in a situation where you’re unprepared and you’re going to be tempted to buy food in the airport or buy hotel food or have to run out before your interview because you’re hungry and you really wish you had coffee and you didn’t think about that. And then it’s stressful, it’s expensive, and then you get home and you’re like, wow, how did I spend so much money? I didn’t even notice that that happened. Just being prepared for that is I think the best way to prevent it.

Tim Ulbrich: I agree. And as someone who likes to eat every hour or so when I travel, I swear, airports and hotels are like the death of me when it comes to food, options, costs. I generally eat more at home and am somewhat of a picky eater. So it’s not only expensive but it’s like ah, you can’t even always get what you want.

Sarah Cummins: I know. And don’t even think about that minifridge either.

Tim Ulbrich: No, no, absolutely not. Don’t even open it. Yeah. So we talked about where we can cut back. And I want to end by talking about where you should spend money. So there’s obviously there’s going to be some costs that applicants have to incur and some areas where maybe they shouldn’t try to cut corners. So talk to us about those areas where you have felt like, you know what? This is an area where you don’t necessarily want to invest a bunch of time and resources to try to cut back but rather give permission to spend.

Sarah Cummins: Definitely. So I think the one area that I felt personally I was going to spend the money was on my interview suit. So I feel most confident when I’m wearing clothes that fit me very well, that I think look nice, and when I’m going to an interview, I don’t want to be uncomfortable, I don’t want to be worried that my outfit looks weird or just something doesn’t — just doesn’t look very put together. So I saved up and I got a very nice suit. So I guess my definition of very nice might be a little bit different than everybody else’s definition of very nice. But I got a matching suit and had it tailored to fit me. And what I did basically is just rewore that one suit instead of getting a bunch of less nice outfits, less expensive outfits. One thing that’s a life saver if you’re going to be rewearing suits, instead of getting it dry cleaned between each interview, that can be really expensive: hotel steamers. So if you call ahead to the hotel and ask them to put a steamer in your room, pretty much every hotel I’ve ever called have steamers available. You just have to ask for it.

Tim Ulbrich: Ah, I didn’t know that. OK.

Sarah Cummins: Yeah, yeah. So also starch spray is your friend. So if you just like want to iron it out and put a little starch spray on it, fold it very gentle inside your carryon and take it out first thing and then steam it, it’ll look brand new. And you won’t have to get it dry cleaned over and over again because it’s free to use a steamer versus getting it dry cleaned. So I think that spending money on my outfit helped me feel more confident and I think probably in the long run helped me be more relaxed during the interviews. Additionally, I think another place to feel OK to spend a little bit more money is if there aren’t many hotel options or perhaps the hospital that you’re interviewing at isn’t in the best part of town is to make sure that you feel comfortable and safe where you’re staying. One of my interviews, I remember specifically the hotels were like over $200 a night, some $300 a night really close to the hotel. And I opted to get a cheap Airbnb instead, and that was a huge mistake. It was not a safe part of town. I felt very uncomfortable. And the Airbnb did not have any of the amenities that I needed. I usually don’t pack hair dryers because most places have them. But I did not realize or did not look for the hair dryer until after I had showered in the morning before my interview. But there was a space heater, so I just was pressing my wet hair up against the space heater to try to dry it. Oh, it looked horrible. But spend the money on somewhere that you’re going to feel safe, somewhere that you’re going to feel comfortable because you don’t want to be stressing right before the interview. You don’t want to be worried about it or not get a good night’s sleep because that’s definitely going to show in your interview performance the next day.

Tim Ulbrich: And Sarah, these are fantastic tips. They’re specific, they’re actionable, they’re ones I’m thinking, man, I wish I would have known some of this. But I’m glad we can share this with students that are out there, again, preceptors that are helping coach or mentor students, hopefully they’ll be able to find this information valuable. And I want to close by coming full circle to where we started tonight. And I mentioned I think the mindset piece is something that I hear as you’re talking, I know I read it when I first came across your content. I know you said, yeah, I’m not really sure exactly where I can pinpoint that. But I can tell you through our conversation, it is clear to me that you have an intentionality around your spending, around your money. We talk all the time on the podcast about the importance of that intentionality, of finding your why, of really aligning your spending and spending money where it’s important and not spending money where it’s not important. And I can tell that you have that. And I am so excited to see where not only your professional journey goes but where your financial journey and the impact that you’re going to have on the trainees that will work with you, whether that’s students on experiential training, residents, peers, and the others that you will be able to influence. So I appreciate you taking the time to come on the show to share this information and the tips, the advice that we’ll be able to share with the group applying this year as well as in the future. And my last question for you is where can our listeners go to connect with you further and perhaps follow your journey along the way?

Sarah Cummins: Thank you for all of those kind words. I really, really appreciate it. As far as where students can contact me, I do have a Twitter that I’m fairly active on. I’ve had quite a few students DM me with question about Midyear or my experience or just how to afford this crazy process in general, and I’m more than happy to answer any questions from anybody. You can find my Twitter at @SC_PharmD. And that’s probably the easiest way to reach me.

Tim Ulbrich: Awesome. We will link to that in the show notes as well as some of the other sites that you mentioned throughout the episode. Again, appreciate your time coming on the show. I know this information is going to be valuable. And for our listeners, if you like what you heard on this week’s episode of the podcast, please leave us a rating and review on Apple podcasts or wherever you listen to this show each and every week. And if you haven’t yet done so, I hope you will join us in the Your Financial Pharmacist Facebook group, over 6,000 pharmacy professionals across the country committed to helping each other on their path towards achieving financial freedom. Have a great rest of your week.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]Recent Posts

[pt_view id=”f651872qnv”]