A Crash Course in 401(k) Planning (Part 2): An Intro to Stocks, Bonds, and Funds

The following is a guest post from Dr. Jeffrey Keimer. Dr. Keimer is a 2011 graduate of Albany College of Pharmacy and Health Sciences and pharmacy manager for a regional drugstore chain in Vermont. He and his wife Alex have been pursuing financial independence since 2016.

You got your diploma, passed your boards, and landed that job. You’ve gotten your first big paycheck. Maybe you bought something ridiculous with it. All in all though, you feel like you’re adulting pretty well at this point. So, one morning you decide to make a cup of coffee and do something truly adult: log in to your retirement plan for the first time.

At first, things go pretty well. You make a username. You make a password that makes you laugh a bit. Once you’re in, a dashboard says you have a little over a grand invested! Sweet! But you’re just a bit curious, what is it invested in? You scroll over to the link titled “Investment Options” and click it. The page loads.

Expense Ratios!? Large Cap!? Prospectus!? These aren’t real words!

But they are.

Even though being responsible for your own retirement seems like a daunting task (it is), understanding what you are investing your money in doesn’t have to be. In this post, part 2 of our series on 401k planning, we’re going to talk about the investment products you’re most likely to find in your retirement plan: mutual funds, index funds, target date funds and exchange traded funds. But before we can get into that, we need to talk about the types of financial assets (securities) they’re made of: stocks and bonds.

Stocks

Stocks (aka equities) are your opportunity to become a part owner of a business. By purchasing a portion of a business, known as a share, you have equity in that business, which entitles you to some of that business’s profits. Those profits come to you through an increase in the value of the share you purchased, known as capital gains, or through a direct distribution known as a dividend. Taken together, capital gains and dividends give you, the investor, a return on the money you invested in shares of the company.

For the most part, owning stocks is the main way most people grow wealth through investing in financial assets. Over long periods of time, the potential to grow your wealth by investing in the stock market far exceeds your potential to grow it in something like a bank savings account.

However, there is a trade off.

Unlike a savings account, where the balance will never go down, the value of your investment in a stock (your principal) can go down. Sometimes with a drastic decrease and for no good reason! Don’t believe me? Let’s talk about Snapchat.

From Bloomberg, 2/22/2018:

“In One Tweet, Kylie Jenner Wiped Out $1.3 Billion of SNAP’s Market Value”

That day, if you held shares of Snapchat (ticker symbol SNAP), they would’ve lost 6% of their value in a day from something as small as a tweet from a member of the Kardashian clan. That wasn’t even the worst single day drop for a stock that year! Facebook took the crown for 2018 (and history) with a 12% loss in a day which eroded almost $120 BILLION from their market value. For perspective, that’s almost the entire GDP of Ukraine lost in one day.

But what does all that mean? I thought stocks were supposed to be awesome. Well, over the long term, they can be. But over the short term, they carry substantial risk in the form of ups and downs to share price known as volatility. And, in the case of individual stocks, share prices can actually go to zero if the company goes out of business (cue Enron).

Bonds

Bonds belong to a group of assets known as fixed income. When you buy a bond, you’re not buying ownership but are instead buying debt. Bonds offer you the opportunity to collect interest from someone else, just like Navient gets from you.

In the world of bonds, money is made primarily from the interest you collect, known as yield. For a typical bond investor, this yield is meant to provide a steady source of income and predictable return on investment.

But again, there’s a trade off.

In general, when you take less risk by investing in bonds, there’s generally less opportunity for growth. Over long periods of time, the difference in growth can be monumental.

Bond investing does have its own risks, though, as they also experience volatility.

When interest rates change, bond prices change. This is because when you buy a bond at one interest rate and the interest rate changes the next day, you need to reprice your bond accordingly to make it marketable for sale to other investors. In short, when interest rates rise bond prices go down. And, when rates drop, bond prices go up.

Your bond can also lose value if the people you’re lending money to fail to pay up (they default) or there’s a perceived risk of them doing so. This will drive up the interest rate on the bond and lower the value of the bond you hold. With the exception of US Treasury bonds, this type of risk (credit risk), is said to apply to all bond investments.

Mutual Funds

So with all the risks associated with stocks and bonds, how do you stand a fair shot at making money over the long term? You work in a pharmacy, not a hedge fund. Thankfully, the financial services industry came up with a solution for the layperson a long time ago: the mutual fund.

With a mutual fund, you outsource the job of picking stocks and bonds to people that know what they are doing (or at least, say they know what they’re doing). These funds collect investor money and invest it according to a strategy that they lay out in a statement called a prospectus.

Aside from reducing risk by investing in multiple stocks or bonds (diversification), mutual funds can also make it much easier for you to choose what you want to invest in. Just like how learning drug classes instead of individual drugs made pharmacy school a lot easier, mutual funds make investing easier by breaking the wide world of stocks and bonds into categories called asset classes. For stocks, funds will typically focus on company size (market cap) and investment style (growth vs. value). And, for bonds, credit worthiness and term (length of bond repayment) are the main factors.

So by now we’ve established that mutual funds make investing easier by helping you with diversification and grouping securities into asset classes. So what’s the catch?

Well, there’s a big one: fees.

Since you’re outsourcing the legwork of investing to someone else, they need to get paid right?

But what’s a fair price?

Should you pay them upfront?

Over time?

What about when you cash out?

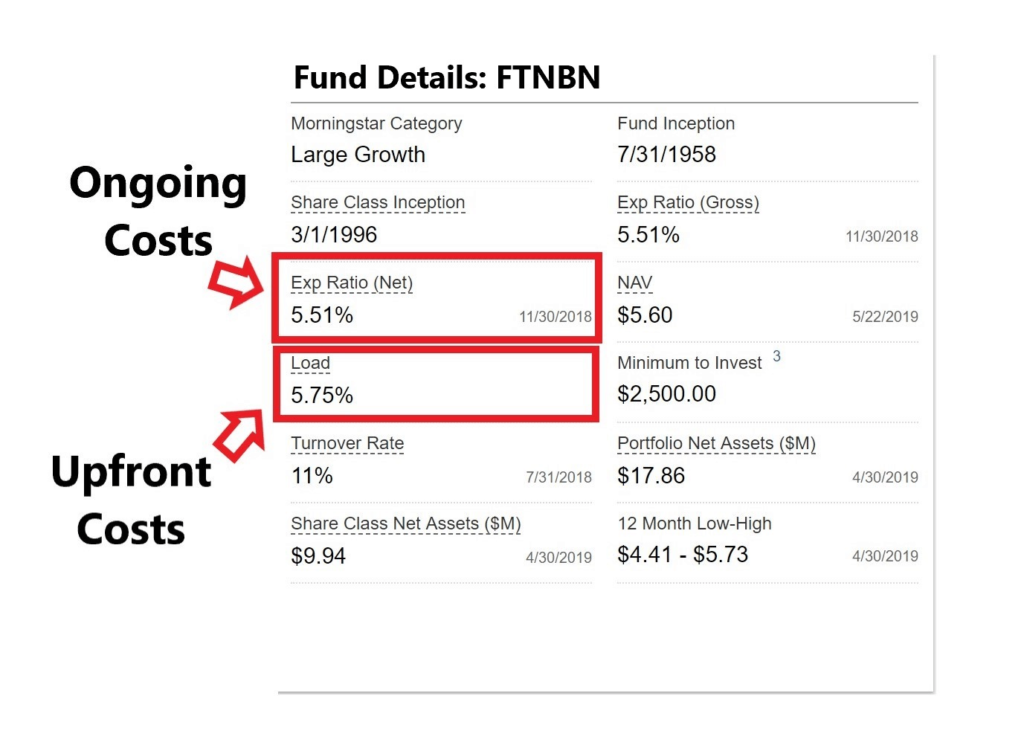

Well, depending on the fund, you might get hit all 3 ways. And, if you’re not careful, these fees can make a massive difference in your success as an investor. So what do they look like? For that, let’s look at a really bad fund which shall not be named (fake ticker symbol: FTNBN) and it’s snapshot from the site Morningstar.

Compared to most mutual funds out there, the fees on this fund are really high but, for the sake of argument, let’s say you want to invest $10k in this fund. If you were to give these people your money, you’d find yourself $575 poorer in an instant from their sales load. OK…but they are going to make me money in the long run and “beat the market”, right? Wrong!

If you put your money in this fund 20 years ago, not only did its managers fail to beat the market (measured by the S&P 500 index), but you actually lost money over this time period. How? Poor management probably played a role, but you can be sure the ongoing fees they were charging were the main culprit.

You see, that number called the expense ratio is the amount they take out of your investment every year for the privilege of having your money in the fund. If you were in this fund, you were paying a whopping $551/yr for every $10k you had invested with them. The fund managers don’t just get this money when the fund does well; they get it regardless.

You, the investor, just get bigger losses and smaller gains.

Imagine if this fund charged the 3rd type of fee, the redemption fee, where they actually charge you another percentage of whatever you take out. Ridiculous!

To be fair, this fund was one of the most egregious I could find. Many funds today do not charge sales loads or carry heavy expense ratios. But, chances are, they would if it weren’t for a man named Jack Bogle and a crazy idea he had back in the ‘70s.

Index Funds

Remember how I mentioned that fund above failed to beat the S&P 500 index? They’re not alone. It turns out the majority of funds that rely on professionals actively picking stocks don’t beat their benchmark indexes. This is as true today as it was back in the 1970s when Jack Bogle, the founder of Vanguard, decided to open the world’s first S&P 500 index fund.

The premise was simple. If you can’t beat ’em, join ’em.

Instead of relying on “active” stock picking, his fund would simply track the S&P by investing in every company within the index proportional to their size, a process called “passive management.” This did two things:

1. Gave investors a diverse basket of US stocks

2. Cut down on costs since he didn’t have to hire stock pickers

That last one was a game changer. The success of Bogle’s index fund set off an arms race in the fund industry to lower investor costs. So much so that today you can even invest in some of these funds for free. No load, no expense ratio, nothing. Free. Heck yes!

And it’s likely you have some of these funds in your retirement plan!

But wait, there’s more! Not only are they cheap, they make picking investments easier. When investing in index funds, or indexing as it’s called, all you are looking for is an index to track and a cheap fund to do it. Want to own every publicly traded company on the planet? There’s a fund for that. What if you want to target only real estate investment trusts (REITs)? Yeah, you can do that, too! What about bonds? Yes, there are indexes out there with funds you can buy, too. With index funds, it’s easy to make a portfolio that invests in the mix you want.

But, believe it or not, things can get even simpler.

Target Date Funds

Also known as lifecycle funds, target date funds are a lazy investor’s dream. Chances are, you might be invested in one of these already and not even know it. Many retirement plans have an auto enrollment that puts a percentage of your income into a target date fund as the default investment strategy.

Traditionally, as you get closer to retirement you want to shift your portfolio from more risky assets such as stocks into safer assets such as bonds. While this is a pretty straightforward process, many people are uncomfortable with making changes to their nest eggs themselves. So uncomfortable, in fact, that many people hire someone else to do this for them and pay them an ongoing fee. The mutual fund industry took note, and because they also liked money, worked on a solution they could keep in house.

Their bright idea? The target date fund (TDF).

Basically, a mutual fund company markets a number of funds with names looking like this:

As you can see, there’s a date in the name. All you have to do is pick a fund with a date that best matches when you plan to retire, give that fund money, and…go do something else. Maybe brew some beer. You’re done playing money manager.

How?

A TDF is designed to be an all-in-one, set it and forget it, type of product. Over time, the makeup of the fund (its asset allocation) will shift automatically into a mix that’s more appropriate for your expected retirement date using a formula called a “glide path.” To do this, a TDF is typically comprised of other mutual funds and the TDF’s glide path dictates the mix of those funds within the TDF.

But remember, the fund industry likes money. Since TDFs serve as a convenient wrapper for the mix of funds they contain, you may pay a premium for that convenience. So if you’re someone who hates the idea of having to change or rebalance your portfolio, or spending time on it in general and you just want to keep contributing, these can be a great option.

Exchange Traded Funds

Lastly, you may encounter the newest type of fund in your retirement plan, the exchange traded fund (ETF). An ETF is not all that different than a mutual fund. You get a diverse basket of stocks, you can track an index, and you get charged an expense ratio. But, they are very different in how they’re traded. With a mutual fund, if you want to buy or sell shares you put in an order and that order gets completed by the next day. With an ETF, you can buy or sell your shares instantly just like a stock.

Also, with most mutual funds you need to make an initial investment of a couple thousand dollars. With an ETF, you can invest for whatever the price of a single share costs. This can allow a beginning investor to make a portfolio of many funds without needing a lot of money.

There is one extra “fee” to be aware of though. When you trade a security, be it a stock, bond, or ETF, there’s a cost to facilitate that trade known as the bid-ask spread. In essence, there’s a higher price you can buy a security for and lower price you can sell it for. The difference between those two values, the spread, is the cost paid to the exchange that facilitates the trade. The more something is traded, the more liquid it is said to be, and the lower the spread will be. While not especially important for something you intend to hold long term, it adds a cost to buying and selling that you should keep in mind.

What’s Right for Me?

Now that you have a better understanding of what types of investments are lurking in your retirement plan, the question now is “which one(s) to choose?” Well, just like the decisions surrounding your contributions were very personal, these will also be.

And, there’s no one size fits all approach.

When building your portfolio, there are many factors to consider. Some of the main ones:

- Retirement Plan

- Do you plan to retire early or at a traditional age?

- How much do you need to fund your retirement?

- Risk Tolerance

- How much risk you’re able to take

- Usually related to your age and expected time to retirement

- Risk Capacity

- How much risk you need to take

- Related to your current wealth, savings rate, retirement time frame, etc.

- Investment Strategy

- Do you want factor exposure?

- Who’s Managing It?

- Are your investments something you want to DIY or are you more comfortable with a professional managing them?

That last point is extremely important because statistically speaking, Americans are horrible at investing on their own.

Why?

Because much of your success as an investor is going to be driven by how you behave in different conditions. If you’ve ever heard the old adage “buy low and sell high” you may be surprised by how many people do the exact opposite. While there are many benefits to the DIY approach in managing your investments, it can sometimes help to have a professional help manage you. Aside from having the knowledge to build a portfolio that meets your needs, a financial planner can help you navigate the ups and downs of your investing career in a way that keeps you on track. If you feel like having that guidance, support and expert knowledge in helping you navigate your investments and portfolio, schedule a free discovery call to see if YFP’s fee-only financial planning services are a good fit for you.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]