Key Tips For Refinancing Your Student Loans in 2019

On this episode of the Your Financial Pharmacist Podcast, Tim Ulbrich is joined by Tim Church, YFP refinance expert and student loan ninja. In addition to a quick recap of the process of refinancing your student loans, the benefits of refinancing, how to calculate your savings and what to look for in a refinance offer, Tim and Tim give you an update on a new refinance offer available that may save you big.

Summary

On this episode, Tim Ulbrich asks Tim Church about how to refinance student loans, the benefits of refinancing, how to calculate savings on refinancing your student loans and what to look for when analyzing which refinance company to choose.

Refinancing may not be the best option for everyone with student loan debt. First, you have to decide if you are going to pursue student loan forgiveness or not. If you are going to pursue PSLF or if there is a chance you could, then do not refinance as it will make you ineligible for forgiveness. Additionally, mathematically, refinancing may not make sense for some people, especially if they are needing an income driven repayment plan due to having unstable income or upcoming changes in income.

The main reason to refinance is to get a lower interest rate. On average, graduate or unsubsidized student loans have an interest rate of 6-8%. If you refinance with a lower rate, you have the potential to save thousands. When you refinance, it is possible to get out of debt faster as you may be able to pay more money toward your principal balance regardless of how long your term is.

Other benefits of refinancing student loans are that you can potentially remove a cosigner from a loan, lock in a fixed rate, and potentially receive a cash bonus. Refinance companies make money from the interest you pay on your loans. Your Financial Pharmacist has worked with several reputable loan companies to offer cash bonuses when refinancing with their companies.

Tim Church discusses the newest refinance company partner, First Republic. They are only in select cities, however, can offer (at the time of recording) 1.95% fixed interest rate for a 5 year term and up to 3.95% fixed interest rate for a 15 year term. There are several other requirements that need to be met to be able to refinance with First Republic, however, doing so could save you lots of money over the course of your loan.

If you have any questions regarding student loan refinancing, email the YFP team at [email protected] .

Mentioned on the Show

- YFP Student Loan Refinance Partners

- Costco Gold Star Membership Giveaway

- YFP 029: Refinancing Your Student Loans Part 1

- YFP 030: Refinancing Your Student Loans Part 2

- YFP 018: Maximizing the Benefits of Public Service Loan Forgiveness

- YFP 078: Is Pursuing the Public Service Loan Forgiveness Program a Waste?

- YFP 062: The ‘Other’ Forgiveness

- Annual Credit Report

- Better Business Bureau

- NerdWallet Watch List

- CommonBond

- Splash Financial

- Earnest

- LendKey

- Sofi

- First Republic

- YFP 044: How to Determine Your Life Insurance Needs

- YFP Blog: How to Refinance Student Loans Under 2% Through First Republic Bank

- YFP Refinance Calculator

- Email YFP With Your Refinance Questions

Episode Transcript

Tim Ulbrich: Hey, what’s up, everybody? Welcome to Episode 090 of the Your Financial Pharmacist podcast. Excited to be back on the mic alongside Tim Church. Tim, how you doing? It’s been awhile.

Tim Church: Yeah. Hey, Tim. I’m glad to be back on and just cool to be closer to that 100 mark.

Tim Ulbrich: So awesome. I was reflecting on that today, Episode 090, we’re 10 away. We’ve got some exciting things planned for Episode 100. And just so you know, Tim Church, while I am freezing here in almost sub-zero temperatures up in Columbus, Ohio, I happened to pull up my weather app today. And I still have Palm Beach Gardens on my phone from last time I visited, and it said it was about 80 degrees when you walked out of work today. So how’s that feel while we’re suffering in 0-degree temperatures?

Tim Church: It feels great. But I’m not looking forward to coming to Columbus in April.

Tim Ulbrich: Hey, hopefully by then, we’ll have turned a corner. So we’ll see what happens. Well, excited to have you on. I certainly, as I alluded to in the intro, you are our student loan expert. And when it comes to refi, you’ve had so much experience in this area, so I want to pick your brain a little bit. We’ll revisit some of what we talked about in episodes 029 and 030 around refinance. So certainly go back and listen to those episodes as well. But things have changed, there’s new offers that are out there. And so we want to make sure we’re revisiting this topic, probably one of the most common questions that we get is around this topic of refinance. Tim, before we jump in though, I want to say side hustle series, the work you’ve been doing with that, I have really been enjoying the episodes that you’ve been recording. So great work with that, looking forward to more of those coming in the future. Alright, here we go. Student loans, always a hot topic. As I mentioned, one of the most common questions we’re getting. Refinance. Should I do it? How should I do it? What companies should be used? So Tim, before we jump into some of these specific questions, let’s discuss specifically who should not be considering a refinance. So walk us through that component of who should not be refinancing.

Tim Church: Definitely. Well, I’ll be the first one to say that I made this huge mistake back a number of years ago. But I think the way that companies are marketing themselves and getting people to want to refinance that you have to really take a step back, and it’s not the best option for everybody. I mean, mathematically, it doesn’t make sense, even if you’re somebody that really wants to get rid of your loans as fast as possible, it may not actually be the best way or the best approach how to do it. So I think the biggest group, where refinancing is completely off the table is that if you’re pursuing the Public Service Loan Forgiveness program or you think you could be or that’s still in the running because if you’ve got typical student loans that pharmacists are facing, you know, $160,000 or more, then mathematically, PSLF is always going to win out just because of some of the strategies you can do to optimize it where you can simultaneously save in your 401k and other retirement vehicles while lowering those student loan payments and then not having to worry about a tax bill. So I think that’s really the biggest group where you’re just going to shut down from refinancing because once you do that, you’re going to make yourself ineligible. I think there’s some other groups too where you have to really look at this before you pull the trigger. And that’s really individuals who need an income-driven repayment plan. And there’s a number of different reasons why that may be. Now, one is obviously for PSLF, but it could be if you’re having an unstable income or you anticipate you’re going to have a change in your income and you really need to make sure that you’re able to cover at least that monthly bill. And you may not be ready to make whatever that payment is when you refinance, whatever that term may be. So I think those are some of the key ones that you really want to look out for.

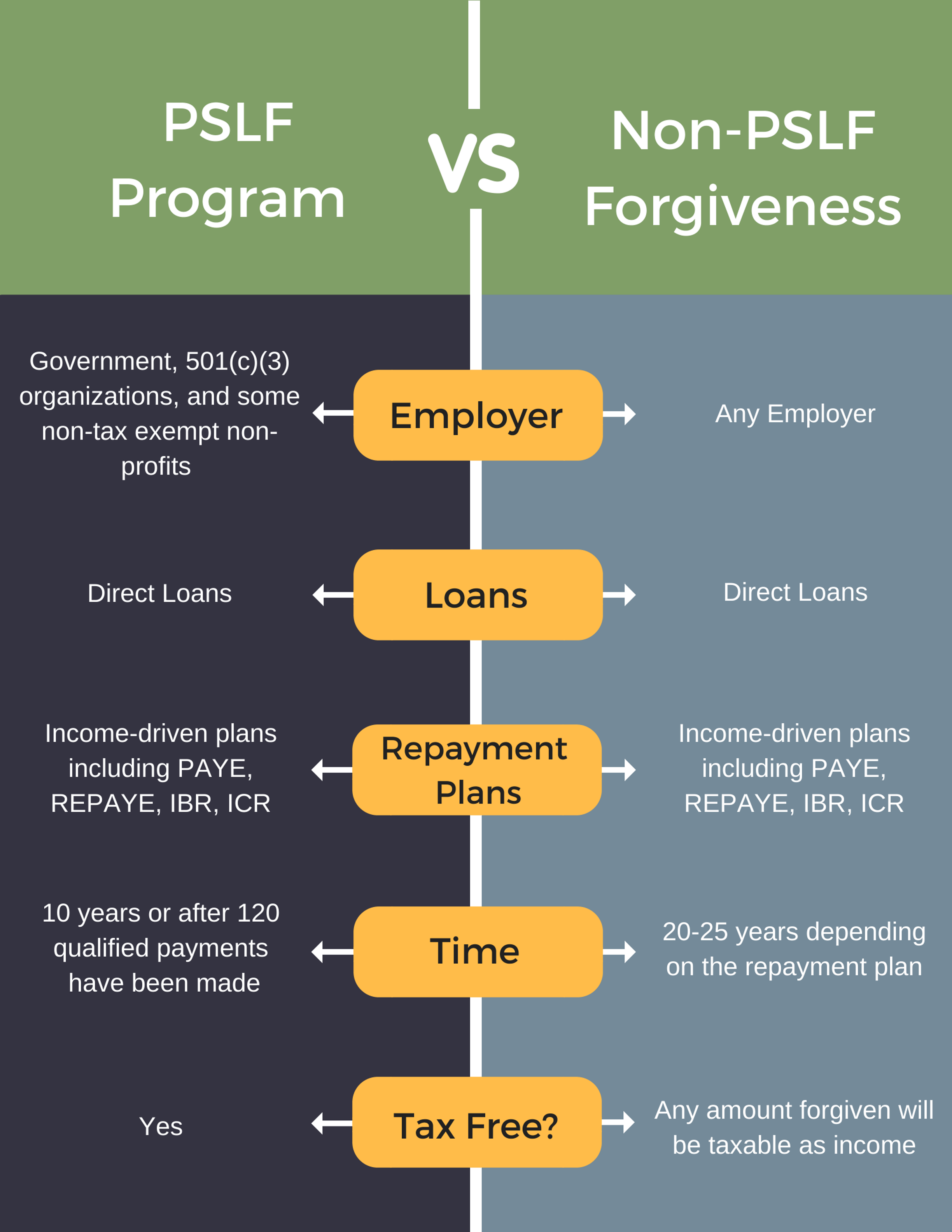

Tim Ulbrich: Yeah, and I think, Tim, just to elaborate a little bit on your PSLF comments, which I think are spot-on and certainly just to reemphasize that, if you’re even remotely considering Public Service Loan Forgiveness, the way we always teach the loan repayment option is you first have to decide forgiveness or no forgiveness. And if it’s a no forgiveness play, then you evaluate a refinance, among other options. And we talked about PSLF in Episode 018. We also came back and talked about it on Episode 078 after some of the news that recently came out that was really getting to the point that 90+% of people applying for loan forgiveness were not receiving the benefit, and we hopefully broke down some of the confusion around that. Tim, I want to ask, though, we talked about in Episode 062, we talked about non-PSLF, so the other loan forgiveness. So that’s also something that people need to be looking out for, right? Any forgiveness clause they may be pursuing in the federal repayment option, they should not be going through a refinance, right?

Tim Church: Right, because you have to keep your loans in the federal system in order to qualify for any of these programs. So once you make that move, you would make yourself ineligible. And there are people where using the forgiveness that’s not through PSLF, where it’s 20-25 years, depending on the repayment plan that you choose and then having to pay the tax bill on the amount forgiven actually can be a better strategy than refinancing. I know it may seem overwhelming to say, “Hey, I’m going to hold onto my loans for 20-25 years,” but even with having to plan for that tax bill, you could be in a better position, depending on how high your debt-to-income ratio is. So you really have to look at the math behind what your situation is and what the difference would be if you refinance and how much would your monthly payments be and what kind of buffer do you have to even put towards other financial goals? So we talk about sometimes the debt-to-income ratio of 2-to-1, but also some of the things that you’re feeling holding onto loans that long, there’s some other emotional aspects I think behind it as well. But it’s also important that you do the math and see what comes out to be a better option.

Tim Ulbrich: Yeah, just a great example of that, Tim: This past week I was at Ferris State University doing some work with their students, and we were walking through PSLF and non-PSLF forgiveness. And you know, I think we tend to focus on so many of the mathematical components, but when I talked to them about non-PSLF forgiveness, 20-25 years, the tax bill, I got this look on their faces like, “Who in the world would ever consider that?” But I think to your point is that it’s a combination of these variables. And if you’ve got a very high debt-to-income ratio, and you’re working for a non-qualified employer, you’re working for a for-profit employer, then you know, depending on how you feel about it, it’s at least probably an option to evaluate. So again, just to be clear here, anybody who’s considering loan forgiveness through the federal loan repayment options, whether that’s PSLF or non-PSLF, certainly refinance would make you ineligible because you’re pulling yourself out of the federal system into the private system. The other question I get here, Tim, is — and you alluded to this a little bit about income-driven repayment plans and anybody who needs that, but what if I’m anticipating changes in income or I’m unsure about cash flow I’ll have month-to-month? I mean, is this something similar to the federal loan repayment options where I can make extra payments? So I could start with a longer term, say 20 years, and then eventually come down if I have more? Or do you recommend if somebody’s in that period of I’m not exactly sure the stability of my income, I should just stay in the federal system and then wait to do a refi?

Tim Church: Yeah, I mean, I think the conservative play is better in this situation that you want to have stable income and know what’s coming in because you’re not going to get that flexibility with most refinance companies like you get with the federal government. I mean, the option to do income-driven repayment plans and at the very worst, to temporarily stop making payments, whether it’s a qualified deferment or forbearance, you know, that’s something that you have to consider that you’re giving up. Now, some of the companies, they have variable options. I think at least one has an income-driven repayment plan option, and some allow you to make interest-only payments, but I think that you have to be pretty confident in your financial position before you make this switch.

Tim Ulbrich: Yeah, we’ve definitely seen a transition, I would say over the last five years where these plans very much are starting to look and be as competitive as the federal options, just hopefully with a lower rate, which I’ll talk about here in a minute. So I think we’re going to see more of that shift toward offering income-driven repayment plans, especially knowing how popular those are among borrowers when they go into active repayment. So before we transition and talk about the main benefits of refinancing, obviously, there are benefits because you have done this — how many times now have you gone through the refi process?

Tim Church: Um, let me see. I’ve refinanced my loans three times. And I think my wife has also done three times. So like a total of like six times.

Tim Ulbrich: OK. So let’s come back to that because I think that when I mention to people, you can refi more than once, I think there’s some concern about the impact on credit scores and just not being aware that you can do that. So let’s come back to that. But let’s first start with the main benefits of refinancing. So why would somebody pursue this? So they’ve decided, OK, I’m not going to pursue loan forgiveness, so now I’m going to evaluate either staying in the federal loan repayment system, choosing one of those options, or going to a refinance. What would be the benefits of doing a refi?

Tim Church: So I come back to your situation, Tim, because you’re somebody that was not pursuing any of the forgiveness programs.

Tim Ulbrich: Please don’t remind me, Tim.

Tim Church: And stayed in the federal system. And you —

Tim Ulbrich: At 6.8%, yes.

Tim Church: Right, so you had a lot of financial stability. And if you’re somebody in that position, most of the time, you’re going to be able to get a lower interest rate. And obviously, that is the main benefit and the main reason why you should even consider refinancing. So the average interest rates in the federal system are typically from 6-8% for a graduate loans or unsubsidized loans, and so by getting that overall interest rate reduced, you’re going to save a lot of money over the course of the loan. Now, it depends on your balance you start with, the change in the percentage and then obviously how fast you pay it off. But if you consider a pharmacist who has a balance of $160,000, and you plan to pay that off over 10 years, well if you take a rate from a 7% overall to a 4%, you’re going to save about $28,000 over those 10 years. So really, it can have a huge impact on the total amount that you’re going to pay over the life of the loan.

Tim Ulbrich: So what do you say — and I know obviously the news has been over the last year, we’ve seen the fed increase interest rates, which obviously these private loans are going to be tracking with what the fed is doing with their interest rates. So are you seeing these are still a competitive option with those federal loans being 6-8%? Were they more competitive 12 months ago, and they’re less competitive but still competitive? What are you seeing in terms of rates and what people are getting to? Obviously, knowing it’s variable based on debt-to-income ratio, credit score, etc.

Tim Church: Yeah, I mean, I haven’t noticed a huge difference.

Tim Ulbrich: OK.

Tim Church: In 2018, when we did multiple refis, we were able to get the first couple times down to in the 4’s. I know Nate, the Real Estate RPH, he I think was able to get down to like a 3.5% fixed rate with one of the companies. And this was in 2018. So I still think there’s definitely a lot of competition and a lot of room. And obviously, we’ll talk about one of the special partners that we have because they offer kind of a unique situation. So Tim, so we talked about obviously the lowering your rate I think is the biggest reason. That’s the No. 1 reason why you’re going to refinance. You’re going to pay less money in interest over time. So one of the things that’s kind of a cool way to look at it is technically, you will get out of debt faster if you make the same monthly payment that you’re making with a higher rate and switch to a lower rate because more of that payment is going toward the principal. So that’s another kind of a cool way to look at it. So regardless of what term you end up choosing, if you just make the same payment, you know, more of that is going to the principle, and you’re going to get done with it a lot faster.

Tim Ulbrich: So what are you seeing in terms of terms? You know, that’s usually one of the questions that I get of, you know, what is the range here? Is it 5-20 with everything in between? Are these all the same between companies? And then I would assume, in theory, the more aggressive you’re willing to be with payments, making larger payments, the better the interest rate you’re going to get. What are these companies offering?

Tim Church: Yeah, I would say in general, that’s true. So you’re totally right. Most companies, it’s anywhere from 5-20 years. A lot of companies offer a 7-year, a 10-year and a 15. And then a couple companies offer kind of rates a little bit in between there. But yeah, in general, the shorter the term, the more competitive the interest rate that’s being offered. And then also, the other variable that goes into it is whether it’s a fixed rate or whether it’s a variable rate. And that’s the other thing. A lot of times, they’ll put out teaser rates or rates from. Even on our website — which is typically their variable rate that they’re advertising. And sometimes, that’s just a teaser rate just to get you interested. But you always have to look at what the maximum or what the cap is because that can obviously change with the federal reserve and with LIBOR rates, so there’s a lot of different situations where you can end up in a worse situation than what your rate was before you refinanced.

Tim Ulbrich: Well, let’s talk there for a minute about the co-signer issue. That’s often a question I get as well is that, hey, I currently have a loan, I’m in the federal system, I’ve got a co-signer. How does that work when I’m looking to refi my loans and bring them over to the private sector?

Tim Church: So a lot of times, that’s another reason to do the refinance is you can actually get rid of a co-signer. So depending on your credit score, your current income that you have, your debt-to-income ratio, you can actually just put yourself on the loan and remove whoever else was on there. Because I know that that is a concern for some people, especially when the originally took out loans that they have somebody else that potentially is responsible.

Tim Ulbrich: Awesome. So we have talked through several benefits. We obviously talked about the interest rate and the savings, being able to get out of debt faster, the money going to a principle, potentially removing a co-signer, being able to lock in a fixed rate, more aggressive payments, usually the better rate that you’re going to get. What about the cash bonuses? You know, you mentioned the variable rates being kind of a teaser to get people in. The other teaser I see out there is often the cash bonuses, which certainly we have negotiated the best rates for our listeners over at YourFinancialPharmacist.com/refinance. But are those cash bonuses what they seem? Are there any hooks? And then why not refinance multiple times if you’ve got opportunities?

Tim Church: Well, that’s what my wife and I did. We literally did that. And this is no joke, but honestly, we actually made $2,700 last year in 2018, just by refinancing multiple times.

Tim Ulbrich: Time to quit your YFP job, right? Just keep refinancing.

Tim Church: Honestly, I don’t think that’s always going to be the scenario and the situation, especially depending on what competitive rates that you’re able to get. But it was fortunate for us is that every time we checked every couple months is that another company was able to make an offer that was lower at which we currently had. So it obviously made sense. It wasn’t just for the cash bonus that the companies were offering. It was also to get that lower interest rate. But I think it’s kind of important to understand, you know, why they do this and why pharmacists or healthcare professionals are sort of targeted. But obviously, it’s no secret that refinance companies, they’re going to make money from you by the interest that you pay them each month. And pharmacists, they typically carry high debt loads in the six figures, we all know that. They’re actually going to make more money off of pharmacists and other healthcare professionals than other people with just typical undergraduate student loan debt. And so as an incentive for you to use a particular company, they typically will offer a cash bonus or sometimes called a welcome bonus. And as we talked about, you’re not limited to doing this one time. And because the interest rates can always change and sometimes you can get a better rate, then you can obviously do it multiple times. I’ve heard this term before is “serial refinancing” where you can do this. But I mean, it makes sense that they’re able to do that. But I think one of the cool things — and obviously, we’re fully transparent. We do make a commission if you refinance through our links, but a lot of the big players out there, they’ve got student loan review sites and things like that. But they’re either offering nothing if you use their sites or use their links or a very minimum amount of money. But that’s not really our style. And one of the things that we wanted to do even from the get-go is really offer a lot of value and push that number as high as basically we could to offer our audience some really high cash bonuses, which there’s not very many companies and businesses that are basically putting that out there and putting that much money for people to get.

Tim Ulbrich: I think we need to get you a “Refi King” T-shirt. Right? That would be awesome. It really is incredible. And I think that’s an important piece that people just need to understand, what you just said there about the cash bonuses, the transparency is important. Obviously, that’s taxable income, right? So you need to account accordingly when it comes to tax season and accounting for that money that you’re making on a refi. What about the credit impact? That’s a common question I get that, “Hey, if I go through with these refinance offers, is looking at rates going to impact my credit?” And if not, obviously then when you go through the process, I’m assuming it would, just like you’re buying a car or something else. Talk us through the impact on credit.

Tim Church: Yeah, so when you do a rate check, they often do a soft credit check. So you’re just trying to see what kind of rate you’re eligible for. You’re not going to have any ding or any hit on your credit score. But you may experience a very minimal change when you do refinance, when you use — basically, when you fill out the entire application process, they’re doing a hard credit pull. So it is possible you might see a small reduction in your credit score. Personally, my wife and I didn’t really see that big of a difference, to be honest.

Tim Ulbrich: Which is just all the more reason, you know, to be aware of it, check your credit, annualcreditreport.com. You can do that once a year from three different companies. It’s something you should just be doing anyways, but obviously, be aware of the impact that this may have in that process and weigh that benefit as you’re going along and the risk, if any, associated with doing that. So Tim, second most common question I get outside of, “Hey, should I refinance or not?” is “I’ve got all these options, I’ve got all these choices. You guys have some on your site, I’m getting these fliers in the mail, I’m getting emails, I’m getting things from my national association. What company should I choose? And then what are some things that I should look for in choosing a company?”

Tim Church: Yeah, I mean, you definitely have to make sure they’re reputable. Unfortunately, there are so many scams out there with companies claiming to have these special forgiveness programs or special refinancing programs, and oftentimes, there’s — one of the ways you can tell they’re not reputable or they’re kind of scammy is that they want to pay them a fee. So that’s really a big red flag is that if they’re asking for some kind of origination fee in order to do the refinance, I mean, that’s a huge red flag. I mean, we just talked about that they want to pay you money in order to refinance with them. So definitely want to watch out for that. But there’s two places that I really like if you’re really concerned or you want to check it out. The first one is the Better Business Bureau. So you can go there and check out and see what kind of ratings they have and also some of the customer complaints, if they have any. And then NerdWallet actually has another cool resource called the Watch List. And we have that link on our website. We’ll put it in the notes. But what they did was is they’re basically identifying and targeting any businesses with unethical practices or fraudulent practices or have like severe debt or liens against them. So I think that’s another cool place to look for to make sure that whoever you’re using is a very, you know, safe company to use.

Tim Ulbrich: So obviously, they need to be reputable. You know, no origination fee, I agree that ultimately, you’re giving them business, and they’re going to make money off of that. We talked about the cash bonuses, you can obviously compare those. What about the forgiveness on death and disability? We know that if somebody only has federal loans, their loans would be forgiven in the event of death or disability. But that’s a question mark in the private sector. I know we’ve seen this move where it seems like most of all, these companies are offering that but not everyone. So what is your advice as you’re talking with fellow pharmacists and peers about how to evaluate that benefit of loan forgiveness on death and disability?

Tim Church: I mean, it’s definitely something you have to consider. I don’t think it’s an absolute must, but if you are going to decide to go with a company that doesn’t offer that benefit because they’re rates are much better, that you want to make sure you have those policies in place. I mean, for everybody pretty much, disability insurance or some kind of coverage is going to be warranted. Life insurance, that could be debatable on terms of whether you absolutely need it. But yeah, I mean, I think it’s something to keep in mind because that is one of the protections that you may lose when you switch your loans out of the federal system to a private lender. Three of the companies that we have on our site, so Common Bond, Earnest and SoFi, they will actually forgive the balance on death or disability. So that is one of the perks of those companies that we partnered with.

Tim Ulbrich: Awesome. So let me just point our listeners to — I think that’s a great point that it’s not an absolute, but if you’re going to work with a company that does not offer that because they’ve got a better rate and you’re weighing the risk and benefit, make sure to figure out that you have the life and disability insurance coverage that you need. We talked about that in Episode 044, How to Determine Your Life Insurance Needs, and Episode 045, How to Determine Your Disability Insurance Needs. So Tim, we talked through the benefits in terms of what somebody should look for in a company: they’re reputable, no origination fees, the cash bonuses, the loan forgiveness on death and disability. Now, obviously add making sure there’s no prepayment penalty. So just like in the federal system, if you want to make extra payments, maybe you’re on a 15-year fixed repayment plan, and you want to expedite that if for whatever reason you don’t refinance down to a shorter term, you can of course make extra payments along the way.

Tim Church: Yeah, and I’ve seen many people where, you know, they’ll say something like, “You know what? I could refinance to a five-year. I could make that monthly payment.” Or “I could make that seven-year payment. But you know what? I want to give myself a little bit more flexibility, and I’m going to set it up as a seven.” Or “I’m going to set it up as a 10. But I’m going to throw extra money at it.” So most of the companies, most of the main companies out there, I haven’t seen this be an issue of making additional payments and paying it off faster than what the term that you signed up for.

Tim Ulbrich: Yeah, I think especially as these companies have become so competitive at getting your business, they’re obviously wanting to offer everything they can to be able to secure that business. So Tim, one of our newest partners that we wanted to talk about on this show and make sure people are aware for those that are able to access this company and the benefits is First Republic. And I have to be honest, when you came to me with what First Republic was and told me about the rates, and I heard you talking about rates below 2% and I’m thinking of most people at 6-8%, I was like, “I don’t think I’m buying it.” But certainly, it’s legit. You’ve gone down this path. We’ve had several others that have. So talk to us about this opportunity, who qualifies, and what are they offering that’s unique compared to the other companies that we’ve been working with?

Tim Church: Yeah, they’re definitely a very unique bank. And it’s funny because of how this bank is described out there. Like a lot of blogs and websites, they talk about it as a secret or a mythical bank. Like, you know, like it’s hidden in the valley, like only certain people have the map to find it.

Tim Ulbrich: To find it, yeah.

Tim Church: But one of the main reasons why it’s kind of had that reputation is that unlike some of the megabanks out there, they’re only in select states and cities. So the state that they have the most locations in is California. And we have a link to the post that I wrote. It has all the specific locations there. But they’re in Portland, Oregon; they’re in Greenwich, Connecticut; and then they’re in Palm Beach County. They happened to be in Palm Beach County, Florida, which is where I live. And that’s why I was able to refinance with them. And then they’re also in Boston and New York City and also Jackson Hole, Wyoming. But why that’s important is that —

Tim Ulbrich: Jackson’s so random. Jackson Hole, Wyoming, right?

Tim Church: I don’t know, I don’t know. It would be interesting to see how their team, how did they decide how to select like what cities they’re going to have. But why that’s so important is that one of the requirements to actually refinance with them is that you have to live within a 20-mile radius of a physical location. I don’t know exactly why they mandate that, but that is one of their requirements. And obviously, that’s going to disqualify a number of people out there that don’t live in one of those locations.

Tim Ulbrich: Yeah, and depending on somebody’s student loan balance, it may be worth picking up and moving. I’m half kidding. But you know, it could when we look at these rates. But I think too, what I’m assuming they’re trying to do, which other companies are interested in doing as well is, you know, the refi here may be the gateway to get in the door as a long-term customer, to purchase a home, to eventually get a HELOC, to do real estate, other things that you do at their banking. But nonetheless, I mean, their rate is like no other what we’ve seen. So talk us through what they’re offering.

Tim Church: Right. You can’t beat it.

Tim Ulbrich: Yeah.

Tim Church: Yeah. I mean, there’s no one else that I’ve ever seen that has these kind of rates. But they still have, even as of the time of this recording, they have a five-year term. And this is the other thing is these are all fixed rates. None of these are variable rate offers. They’re all fixed rates. But they’re offering 1.95% for a five-year term.

Tim Ulbrich: Crazy.

Tim Church: And then it’s up to a 3.95% up through a 15-year term. And one of the things is that, you know, unlike some lenders where they’ll take all of your financial information and then they use their magic algorithm and spit you out a specific rate, it’s kind of — it’s an all-or-nothing. Basically, you either qualify or you don’t.

Tim Ulbrich: OK, so you mentioned them offering rates that are fixed, less than 2%, 1.95% up to 15-year terms at 3.95%. I was actually just coming back and looking using our refinance calculator, which we have available over at YourFinancialPharmacist.com/refinance, where you can run your numbers to say, “Hey, if I were to keep my loans in the federal system versus if I were to refinance, what exactly would be the savings?” So you know, looking at my total indebtedness, roughly around 6.8%, which is hard to think about when you’re talking about rates at 1.95%. So for me, it would have been about $30,000 of savings through a refinance like this. And I think that’s what we’ve seen on average for somebody who’s looking at the average indebtedness and saving a couple percentage points on a refi. Obviously, a rate like this is going to bring that down even a little bit further. Now, I know, Tim, you had to jump through a couple hoops that were not necessarily insurmountable but that were different from other refi companies out there to be able to work with them. So talk us through those just so people that are listening who are going to be evaluating this option among others, what are the things that they can expect in terms of meeting the requirements to be able to refi with First Republic?

Tim Church: Yeah, that is one of the big differences is that it’s pretty challenging to actually qualify and meet all of their requirements, much more stringent than the other major players out there. But we already talked about the 20-mile radius of a physical location. But one of the things that you have to have and what they’re looking for is about 10-15% of the loan balance in liquid savings. And depending on how high your loan balance is, I mean, that can be a pretty substantial amount. And if I recall, that’s not in retirement accounts or anything but actually liquid cash in savings, checking, something that’s able to be accessed pretty easily. So I think that’s one of the requirements that’s pretty tough. And then the other one that I think is pretty tough as well is they’re looking for a debt-to-income ratio of 40% or less. You know, we talked about earlier that it’s sometimes the opposite for people where they have a 2-to-1 debt-to-income ratio. So you know, much higher than that ratio. So I think those are probably the toughest requirements to meet. And sometimes, it may be something where you don’t meet it initially, but eventually kind of once you build your savings up, pay down your debt a little bit, that eventually you’re going to kind of meet those cutoffs. And what they’ve told me, what some of the reps is that these are not all, you know, you have to meet these exactly to the exact T. They kind of look at the whole picture, but this is kind of their basic guidance for when they’re looking at who to approve. And then some of the other ones that you have to have — so you have to have a loan balance of $25,000-300,000. Probably no big deal for most pharmacists who are graduating today. And then a credit score of 750 or higher. And those are really the main things. But then to kind of take it a step further, and this was something that for my wife at first was a little bit — caused a little bit of anxiety.

Tim Ulbrich: You convinced her, though.

Tim Church: I did. I used my amazing persuasive skills to show her all these benefits. But you actually have to bank with them. So basically, wherever you’re banking currently, you have to switch everything over. And that is to keep your rates at the level of where they are, you have to make direct deposits into one of their checking accounts. And then technically, you also have to keep I believe it’s 10-15% of the loan balance in there to keep that rate or it goes up — it goes up by a very small percentage, it’s not anything substantial. But the biggest ones to keep the rates down are making direct deposits, keeping a checking account open, not basically closing all your accounts before the loan’s paid off. So there’s definitely a number of hoops to get it to happen, but I will say that I am impressed overall with their customer service. You know, one of the things they do is they assign you a relationship manager, which you know, I kind of joke with people, I’m like, yeah, it’s VIP access, like your 1-800 number, like you’re calling like somebody’s cell phone, you know, in case you have any issues. But one of the other cool things they do is because they recognize that they’re only in select cities, if you have to use any ATM, it doesn’t matter what other bank or what other company, they’ll actually reimburse for any ATM fees that you incur, which is a pretty cool feature that they have.

Tim Ulbrich: I like that. I mean, I feel like the idea of ATM charges seems ancient in 2019. So glad to see that they’re on board with that.

Tim Church: Right.

Tim Ulbrich: You know, it’s interesting, even though you described those hoops, Tim, to me, as I hear you say all of those, they all make sense to me, right? So for them to be able to offer a very competitive rate, you know, they want to probably have somebody that they’re going to retain long-term business and get Return on Investment elsewhere, which makes sense in terms of banking with them, direct deposit so you have a higher likelihood of future business, and then they want to make sure that you’re a qualified applicant who’s going to be likely to pay on your debt and not be somebody who ends up going into default on these. So having liquid cash, having a favorable debt-to-income ratio, having a positive credit score, I think that all makes sense. And I think the thing I would consider for our listeners to evaluate if First Republic is an option for them to consider is maybe there’s a refinance play that you can do right now and take advantage of some of the savings, a cash bonus, and this is something you’re working towards as the next refinance, maybe in a 3-6 month period as you’re getting these things saved up. And I think you certainly can have your emergency fund in with them, which would help the 10-15% loan balance. So just some strategy, but when it’s all said and done, you’ve been there. It’s actually happened, right? And you’ve gotten good customer service, as you mentioned. So you can learn more about that on our website, YourFinancialPharmacist.com/refinance. We’ve got them listed alongside other partners. And then you wrote an awesome blog post on this topic and specifically, more about that offering that we’ll make sure to link to in the show notes.

Tim Church: Yeah, one of the other things that’s really cool — and this is the feature where I said, I don’t understand this offering that you have. But if you — once you refinance with them, if you pay off the loan balance within four years, they’ll actually give you up to 2% of the interest paid, 2% of the total loan balance. They actually give that and credit it back to you. And that’s one of the things where I said, “Well, like I don’t understand because you guys aren’t making much money, you know, off of this.” But again, it’s kind of what you said is this is one of their moves to get some of the younger generations into their banks to provide them and offer them other services.

Tim Ulbrich: Yeah. I mean, when the Churches end up being in the multi-millionaire status, they’re going to have your business, right? So that’s a good play on them in the future. So those that are listening to this that, you know, heard, OK, who should consider this, who should not? I know that I’m not going to pursue forgiveness, so now I’m going to evaluate a refinance. We talked about the benefits, we talked about the features of what somebody should look for in a company. So the question is, what’s the next step? Where do I go if I’m listening and I want to learn more about this? I want to check rates, I want to see my potential savings. What would you recommend?

Tim Church: Yeah, so I think going to our website, to YourFinancialPharmacist.com/refinance. And I think the first step is is just get some rates and see what you’re even eligible for. And then kind of once you look at the rates you can get and go ahead and use our calculator and see what that savings would be like. You know, some of the sites, they have it kind of baked in, so they’ll let you know and tell you what your potential savings are, but I think that’s kind of important moving forward. And then, you know, obviously if all the rates are the same and all of the perks and things that you like about the companies, then definitely go where the money is. Go for the cash bonus.

Tim Ulbrich: Awesome. And as always, if you have any questions as you’re going through this process, shoot us an email at [email protected]. And a couple last reminders as we wrap up this week’s episode of the Your Financial Pharmacist podcast, we mentioned at the beginning that 2019 is the year of giveaways over at YFP. And so this month, we’re giving away five Costco gold memberships — I really wish I was in this drawing, to be honest, but I don’t think that would be fair — valued at $60 each. So enter the giveaway today at YourFinancialPharmacist.com/giveaway. Again, that’s YourFinancialPharmacist.com/giveaway. And as always, if you liked what you heard on this week’s episode of the Your Financial Pharmacist podcast, please do us a favor and leave a review in iTunes, Spotify, Stitcher, or wherever you listen to your podcasts each and every week. So Tim, thank you so much for joining and to our listeners, have a great rest of your week.

Recent Posts

[pt_view id=”f651872qnv”]