As I was relaxing this weekend and watching one of my all-time favorite films — the 1985 Robert Zemeckis classic Back to the Future — I was thinking…how awesome would it be to be able to turn back time?

I’m not talking about going 30 years in the past and accidentally preventing my parents from falling in love, threatening my very existence. I just mean being able to go back and change some small mistakes, knowing what I know now.

Like an Undo button for life — a quick Ctrl + Z (or I guess I should say, Command + Z, as a recent Mac-convert).

That time you accidentally called your professor “Mom” in front of the whole class? *click* Do over!

That holiday dinner with extended family when you figured why not to bring up politics? *click* Now you can just talk about the weather!

And how about a few tax examples that could benefit from a Command + Z including…

That year you made it rain…so much so that you didn’t have enough cash to pay your taxes at the end of the year? *click* Do over!

That time you bought, fixed up, and sold an investment property only to be surprised by the taxes on the capital gains? *click* Now you can go back and strategize how to minimize or avoid those taxes!

Or, a big one right now…that time you didn’t synergize your tax-filing and public service loan forgiveness (PSLF) strategy and ended up paying more out of pocket than otherwise could have been forgiven tax-free? Ouch. *click* Redo!

The list can go on and on for common tax mistakes we see pharmacists making and, perhaps, less obvious, common strategies that could be employed, through proactive planning, to make sure you pay your fair share but no more.

Unfortunately, we’re still waiting for the Flux Capacitor to be invented.

Until that time comes, we need to be proactive in avoiding mistakes before they happen.

The good news is that some mistakes are easily avoidable…with the right strategy in place, that is.

Let’s take the first example from above – You’ve started doing some consulting work on the side of your full-time gig – after all, your mentor always did say, “If you’re good at something, never do it for free.” A few clients send you something called “1099s”. “Must be like some sort of proof of payment,” you tell yourself. “They already paid me in cash.”

You’re overrun with emotion. Excitement, surprise, self-validation (“maybe I’ll make a post on LinkedIn thanking all the haters who told me I couldn’t do it…”).

And on top of all that, you are ~flush~ with cash.

Finally, with some extra cash and breathing room, you can start hitting the fast-forward button to achieving your financial goals.

Building extra reserves – check.

Extra savings towards retirement – yes, please.

Purchasing an investment property – let’s do it!

Life’s looking pretty good with some extra cash, isn’t it?

Flash forward ten months (in real life, no time machines this time) — it’s April, and your tax return is due. “Congrats on the great year!” your accountant tells you, although this face suggests it may be best to put the champagne bottle back on ice. “I do, however, have a bit of bad news…”

$10,000.

You owe ten THOUSAND dollars to the IRS.

“Well, that’s the price of doing business I guess.” And you’re right; a large tax bill usuallyis an indicator that you had a great year. The problem is, that money is long gone. You set up an installment plan with the IRS, pay a boatload of interest, and learn from your mistakes.

But what if…

What if you had put some money aside for taxes in the summer?

Better yet, what if you had forecasted your end-of-year tax liability and made estimated payments against it each quarter?

Better better yet, what if you had strategically redeployed your excess cash to support your financial growth AND reduce your taxable income?

Even better still, what if you had an accountant do all that for you?

The proactive, forward-looking process I’m describing is called tax planning and is something that is too often overlooked when folks are crafting their financial plans. The focus tends to be on tax preparation, the once-a-year push to file returns before scary, looming deadlines.

While we all wait for the Undo button for life, we need to shift that focus.

I like to compare tax planningto the role of a director in filmmaking, while tax preparation is more like the role of an editor. While both are crucial to the end product, a director has the ability to change the acting in real-time, allowing her to align what’s happening on the set to exactly what she envisions in her script. The film editor can work his magic to take what has already been filmed and make it beautiful, but he’s limited by the passage of time: the scenes have already been cut.

Would a filmmaker prefer to edit a movie that was shot without direction or one that was filmed under the guidance of an expert director like Robert Zemeckis?

So why choose to build a financial plan without incorporating tax planning?

And don’t say because you can always hop in the DeLorean…unless, of course, you’re offering me a ride.

Still have questions? We can help.

The YFP Tax team offers a Comprehensive Tax Planning (CTP) service, created for the pharmacy professional, designed for folks who are ready to be proactive about their tax strategies.

To learn more about how YFP Tax’s CTP service can help add direction to your financial plan, visit yfptax.com or book a call with Sean Richards, CPA, EA, Director of Tax at YFP.

I’m going to get straight to the point with this post. I don’t want this important and potentially game changing message to get lost in any fluff. So, here it is.

You could be making a $1 Million (or maybe even more) mistake and aren’t even aware it is happening.

What?! There aren’t many things you read that can result in you making a small change for some BIG wins…this is one of those.

Whether you are saving for the future in a 401(k), Roth IRA or some other investment vehicle, I’m guessing that with the exception of some financial nerds reading this post, you don’t have a good idea of the ONE THING that is having a significant long term impact on your wealth building success….the fees associated with those investments.

In Tony Robbins’s books Money Master the Game and Unshakeable, he makes a very strong argument for how detrimental these fees can be to your overall financial success. If you haven’t read either of those books, I would suggest doing so as it will get you fired up to take action.

Even if you are not paying a financial advisor to manage your investments, when you account for expense ratios, transaction costs and other types of random fees that you and I aren’t really aware of, many funds (depending on the type of account) have fees that are north of 2%.

Is 2% a big deal? That’s the problem…2% can have a creeping effect that doesn’t make you realize the damage in the short term but will certainly have a significant negative long-term impact.

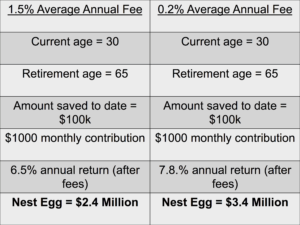

Check out the table below which highlights two different portfolios, one with a 1.5% average annual fee and the other with a 0.2% average annual fee. This calculation assumes the investor is receiving an 8% average annual rate of return less the annual fee.

Did you see the $1 Million mistake?

The investor with the lower-fee portfolio (0.2%) has a nest egg that is worth $1 Million more than the investor with the 1.5% fee portfolio.

Here is the amazing thing…the only difference in this example is the fee!

To compound this mind blowing reality, this difference may even be more for a lot of people reading this blog post over their saving years because their total fees may be even higher than the example used!

All other factors remain constant meaning that you, the investor, can make the same contribution with the same variables yet have a $1 Million greater result by ensuring you are in well-performing, low-fee funds. A Good example is an index fund. These are funds that track a specific market index (such as the S&P 500) rather than try to beat the market.

The following post was written by Nate Hedrick, PharmD., a 2013 graduate of Ohio Northern University. By day, he works as a clinical pharmacist for the sales team at Medical Mutual. By night, he works with pharmacist investors in Cleveland, Ohio – buying, flipping, selling, and renting homes as a licensed real estate agent with Berkshire Hathaway. This experience has led to the creation of YFP’s Real Estate Concierge Services, a one-stop shop for getting you on the right track toward buying or selling your next home.

My wife and I met on a blind date in pharmacy school. We were set up by a mutual friend and despite an impending snowstorm and an exam I really should have been studying for, we went out to our local Mexican restaurant and had a fantastic time. We were crazy for going out in that blizzard and my transcripts can attest to the fact that I should have spent more time studying. Despite the risks, we made it home in one piece, I passed that exam (with a C), and I ended up meeting my best friend that night.

We made that date work despite nature and other obligations working against us.

Now, over 7 years later, we are blessed with two darling baby girls, a goofy dog, a wonderful home… and a mountain of debt.

Pharmacy school is expensive. So are homes. (So are dogs and kids come to think of it.) Looking back, our blind date is actually a great analogy for our early financial life together. We bought our first home pretty much the same way we handled our first date. We were jumping in with both feet regardless of other obligations. I had just finished residency, our friends and family owned homes, and we were tired of the “temporary feeling” we had from renting. We were driving out into that blizzard despite what the weather report said.

I certainly don’t regret our first date and I love the home my daughters get to grow up in, I just now realize that there was probably more we could have done to set ourselves up for success in both cases.

Just like we could have waited an extra night for better weather and would have still gotten married years later, we could have waited a little longer for our finances to get in order and still would have ended up with a great place to live. Hopefully, some of what I learned can help you whether you are about to buy your first home or your forever home.

#1 – The bank does not set your budget.

A pre-approval letter from the bank is not the same thing as how much house you can afford.

As pharmacists, we are lucky to make great salaries right out of school. However, this is a double-edged sword that often fools us into thinking we can take on a lot more debt than we probably should. When a bank calculates how you get pre-approved for, they use the “28/36 rule” for conventional financing. This means that no more than 28% of your gross income may go to your total housing expenses. Furthermore, no more than 36% of your gross income may go to all your debts. Using these numbers with a pharmacist’s salary will often result in a pre-approval that could have you looking outside your range. Check out the calculator below to estimate your monthly payment based on your projected loan and other costs.

Mortgage Calculator

While there are many ways you calculate your own home-buying budget, I recommend considering the “50/30/20 rule”. The idea is that 50% of your TAKE HOME income should go to your needs, 30% to your wants, and 20% to savings.

Needs are things like food, clothing, transportation, medical needs, student loans, mortgage (or rent), insurance, and property taxes. Wants include entertainment, vacations, charitable donations, and any extra you want to throw at your student loans or other debt. Savings include traditional savings accounts, extra retirement contributions, and wherever you stash your emergency fund.

Remember, this is take-home pay, which really should be what you bring in after taxes and after maxing out your 401k match through your employer. I like the 50/30/20 calculation because it is specific enough to illustrate what you can really afford but flexible enough to allow you to adjust certain things based on your individual needs. Regardless of the method you use, calculate the number for yourself instead of allowing your lender to fool you into looking for a house you really can’t afford.

#2 – Shop around for mortgage lenders.

When I was looking for a bank to get a home loan for our first house I had no idea where to begin. I ended up just asking my parents which bank they used for their mortgage and went with that. It seemed like too daunting of a task to tackle otherwise.

Despite the numerous choices, I encourage you to meet with at least 3 different lenders or utilize a mortgage broker when finding your first mortgage. Find someone who is comfortable with the loan product you intend to use (FHA, conventional, VA, USDA, etc.) and compare what other incentives or advantages they provide if you decide to use them as your loan servicer. If you aren’t sure what the differences or advantages are between the different types of loans, check out my website www.RealEstateRPH.com for an article that walk through each type.

You can go to multiple banks or individual lenders online but this requires you to submit documents multiple times and could take significant time and effort. Plus, the moment you provide your information, it’s often sold to third parties and then you get bombarded with annoying phone calls, text messages, and emails by multiple companies. Fortunately, there is a faster and easier way to compare rates and that’s why we partnered with Credible.

Not only do they have an outstanding user-friendly platform that lets you compare mortgage lenders within minutes, but you deal with them directly until the final stages of the process.

It can be extremely tempting to skip saving up a significant down payment for your first house. With loan products available that allow 3.5% down, why would anyone want to save up a full 20%?

While there are a number of reasons, the primary financial concern comes down to private mortgage insurance or PMI. Essentially PMI is insurance that protects the lender against individuals who default on their loan. The problem is that this monthly payment effectively buys you as the homeowner nothing but ends up costing you $100 per month or more. Luckily, this requirement is removed once you have reached 80% loan-to-value.

What the lender often neglects to tell you is that unless you submit a request at that 20% they can actually continue your PMI requirement up until your reach 78% loan-to-value. Although it might not seem like much, this 2% difference could equate to hundreds of dollars! If you do decide to put only 5% or 10% down, make sure you are paying attention for when you reach the 20% mark and are aware of the process your lender requires for waving PMI on time.

#4 – Don’t forget the hidden costs of buying a home.

Aside from saving enough for a down payment, you need to have some cash reserves set aside for all the little things that come with buying a home. Once you put an offer in, your first major expenses will typically be inspections. General home, pest, radon, sewer line, and other inspections are all important in making sure the home you are buying doesn’t have any major issues. Depending on which inspections you choose to have, you can expect to pay a few hundred to about $1,000.

Closing costs typically run between 2% and 4% of the cost of the loan. That means for a $200,000 house you need to have an extra $6,000 or so available on top of your down payment. The lender is required to give you a detailed breakdown of exactly what your closing costs will be before everything is due. The good news is, many times the closing costs can be negotiated into the purchase offer and actually paid by the seller. Your real estate agent can help with this. Property taxes, home insurance, and PMI (if you have to pay it) are often taken out monthly by your lender and put into an escrow account. This ensures the lender that these important payments are received each month and are on time.

Lastly, if your heater goes out in the middle of winter, you don’t have a maintenance department you can call like you do with a rental. Setting aside some additional funds for these unexpected costs is why an emergency fund is so important. Don’t drain your savings account with your down payment and forget to keep something in reserve for the unexpected.

#5 – Prepare for a lot of “hurry up and wait”.

If you are going to be getting any kind of loan for your new house, prepare yourself for the uncomfortable month that is underwriting. I understand it from the bank’s point-of-view, there is some serious legwork to be done when giving someone tens or even hundred of thousands of dollars. However, I have yet to experience a closing that didn’t involve some mix of “We need this document from X and Y in 24 hours or the whole deal is going to fall through.” Promptly followed by days of utter silence. It can certainly be nerve racking. My advice is to simply be prepared for it and don’t try to squeeze your closing date into a smaller time period than is advised by your Real estate agent or lender. Also, be as diligent as possible when it comes to document collection. Create a new folder on your computer for all your loan documents to live in during the underwriting process and gather all your financial information in that one space.

#6 – Don’t skip out on the home warranty.

I distinctly remember the moment during our negotiations that my wife and I told our Real estate agent we didn’t need a home warranty. The house we bought had just been redone and we were certain the appliances were new. I lived in that certainty for about 4 months before I had no way to wash my dirty laundry. Several hundred dollars later we had a working washing machine and a heap of regret. The average home warranty costs between $300 and $600. The average cost of a new washer is $700. The average cost of a new furnace is $4,000. Each of these (along with several other household appliances) are covered under most home warranties. A small price to pay for a lot of peace of mind. This is especially true when you consider that you can often negotiate for the seller to cover the home warranty for you.

#7 – Work with a real estate agent – its free! (sort of).

Being a real estate agent myself, I admit I might be slightly biased. However, even before I became licensed, I realized the advantages of working with a good real estate agent. For starters they have access to a lot more information than Zillow® or Realtor.com®. These websites work well for the initial home screening process but when it comes time to look seriously for a home, you need a more powerful tool. Each agent has access to a database of housing information specific to your area called the multiple listing service (MLS). Think of it like Lexi-Comp® compared to webMD®.

The best part is that they can give you limited access to this database for yourself if you simply ask. Through the MLS portal, your real estate agent can set up automatic searches that deliver updated listings directly to your inbox as soon as new information becomes available. Once you find a property you are interested in, your agent should help you set up showings, put in offers, negotiate with the seller, and generally help you navigate the complex buying process.

When it comes to contracts and offers, I also recommend finding an agent comfortable with DotLoop®. This online tool allows all the important documents to be drafted, signed, and delivered online. The convenience of being able to submit a signed offer from your pharmacy’s break room is hard to beat.

Finally, the best part is that all this help provided by a real estate agent is effectively FREE if you are a first time homebuyer. The commission for real estate transactions is generally paid by the seller and then split between the listing agent and your agent. This means you usually only pay a small office fee of a few hundred dollars to get the whole deal done! Not a bad price to pay for personalized service.

Finding an agent like I described above can be a challenging prospect. That’s why we’ve created our FREE Real Estate Concierge Services! Here’s how it works: Head on over to our real estate page and click on buy or sell a home. There, you can sign up for a free 30-minute callwith Nate. During that call, we’ll start by learning about your budget, wishes, and goals. Then Nate will connect you with one of our preferred local agents from a network of personally interviewed and vetted top-tier agents. This gives you a local expert to help you on your way. Throughout the whole process Nate will stick by your side, even after closing, in case you have any questions or need an extra opinion along the way. It’s as simple as that! Head on over to our Real Estate page and get started today!

#8 – Home ownership provides tax advantages, even for people that make “too much”.

Not many people would expect there to be disadvantages to making a six-figure salary right out of school. If there is a downside however, it has to be income tax and a significant lack of tax breaks. Even the meager deduction that is student loan interest is lost if you make more than $85,000 per year ($170,000 if married and filing jointly).

Luckily, real estate remains a refuge for limiting your taxable income. Since interest payments can be the largest component of your mortgage payment in the early years of owning a home, the biggest deduction for many people is mortgage interest. There is even an extra point-based deduction you can take the first year you buy your home. For example, if you paid two points (2%) to close on a $200,000 mortgage ($4,000), you can deduct the points as long as you put at least $4,000 of your own cash into the deal. And believe it or not, you get to deduct the points even if you convinced the seller to pay them for you as part of the deal.

Finally, you can also deduct local property taxes you pay each year.

All these combined deductions can add up to quite a lot come tax day. This advantage can even be taken several steps further when you talk about real estate investing and home depreciation, a complicated topic that is worth reading up on.

#9 – Plan to stay for a few years.

The real financial advantage to buying a home comes from slowly building equity by staying there for several years. Although it’s not always easy to predict where you are going to be in a few years (geographically and in life) try to make a five-year plan when deciding how and where you want to live. If you don’t want to be tied to a particular location, perhaps renting is a better idea. If you and your spouse want to have a large family, pick a location (and the number of bedrooms) that supports your plan for a few years down the road. Again, all of this is easier said than done.

My wife and I bought a home with three bedrooms thinking we could grow into them once we started a family. That plan started to fall apart when both of us ended up working from home. Just two years after buying out home we found ourselves with a master bedroom, a nursery, an office…and one of us at the kitchen table. Flexibility is really the answer if your original plan has to be scrapped. Eventually we worked out an extra office space in the basement and now my wife only works at home a few days per week. My advice is to have a plan, then be able to roll with the punches if and when things change.

#10 – Consider “House Hacking”.

How would you like to buy a home, live privately in your favorite part, and have someone else pay your mortgage for you? If this sounds to good to be true, I encourage you to start reading up on the concept of house hacking. The basic concept is to buy a home with 2-4 units, live in one of them and rent out the others. Ideally, these are long-term tenants that consistently pay you enough rent to cover all or most of your housing expenses.

The real beauty of house hacking becomes apparent when you learn that the bank treats the loan for a 4-unit home in the same way they treat a single-family residence. This means a single mortgage buys you not only your first home but also your first investment property. There are also easier ways to house hack if being a landlord isn’t your cup of tea. Renting out your extra bedrooms, transforming your basement into a rentable guesthouse, or even Airbnb are all simple ways to lower your house payments by having others pay your mortgage for you. No matter how you do it, if you don’t mind living with a guest or two, house hacking can be an incredible way to make your first home more affordable. To learn more about house hacking, check out Episode 130 with Craig Curelop, the Finance Guy for BiggerPockets and author of The House Hacking Strategy.

Ready to buy your own home?

Click HERE to access our Real Estate Concierge Services!

I recognize I’m not going to become popular by writing this post. We Americans love our cars and I have fallen into this trap before. We love them so much that we will even defend having them at the expense of achieving other financial goals such as paying off high interest rate debt, building an emergency fund or saving for retirement.

I’m all about safety but let’s work through the rest of this article assuming that the vast majority of vehicles we all drive each and every day are safe. More so than ever before. I’m not suggesting that you start driving a car with broken windows and the bumper falling off to save a few bucks, but let’s be honest that we have overplayed the safety card to justify the ‘need’ for a newer car. It is clearly a ‘want’ and often is one that gets in the way of the rest of our financial plan.

Now, if you have no high interest rate debt, are saving appropriately for retirement, have an emergency fund in place and are working towards achieving your other financial goals, have at it. This article is not for you. However, the vast majority of us are still in debt with high interest rate loans OR are not funding our retirement appropriately OR do not have an emergency fund in place. Maybe even all of the above. This is the group that should evaluate whether or not their car is getting in the way of the rest of their financial plan.

In a recent blog post, “My Top 10 Financial Mistakes,” #7 was buying a car I had no business buying. Now that I have made that confession, I feel I can challenge others to look at this area as well. In 2014, while Jess and I were still trying to get rid of our student loans, I bought a really nice used Lincoln MKX when I had a perfectly functioning (and paid off) Nissan Sentra with less than 50,000 miles on it. I ended up re-selling the Lincoln 6 months later and learned my lesson.

According to Edmunds.com, the average monthly payment on a new vehicle in the US is $479. If you are struggling with debt and/or getting control of your monthly expenses, this is an area I would recommend you take a look at to see if cutting back may be worth it. You won’t miss your car as much as you think you will.

If the average monthly payment for a new car is $479/month and you could get rid of (or lower) that payment, what would that mean for reaching your financial goals? It certainly would mean doing them faster. And here is the thing Jess and I found out. When you make one cut, you start looking for other areas to make further cuts. If you have high interest rate debt, this savings from lowering this monthly payment for a car could make a dent in how long you have that debt hanging around and how much interest you end up paying over the life of that loan. No debt? How about taking the savings and building up your emergency fund? No debt and already have an emergency fund in place? How about getting closer to saving 15-20% of your income each month for retirement?

If instead of having a monthly payment that is the current average for a new car ($479), what if instead you paid cash for a car every 6 years. Let’s assume that car would cost $10,000. Remember, we are going for safe and functional. That would cost you, on average, $139/month ($10,000 / 72 months). If you took the difference ($479 average payment on a new car -$139 average per month if buying a $10,000 car every 6 years = $340 savings per month) and invested that money in a mutual fund within a Roth IRA earning 6% growth per year, that would be worth:

$55,721 in 10 years

$157,097 in 20 years

$341,541 in 30 years

$677,118 in 40 years

$1,287,665 in 50 years

There it is. The potential to save more than a million dollars by strategically buying used, yet quality and safe cars over a long period of time. Is your current car worth a million dollars to you? The great thing about this example is that it would all be tax-free growth since it is within a Roth IRA.

A million dollars you didn’t have before all because you bought used cars that were not fancy, but perfectly functional and yes, safe. No matter which way you look at it (paying off debt, saving for an emergency fund or saving for retirement), that is a better financial decision than buying an expensive vehicle that is going down in value.

The sweet spot is buying a used car and paying cash for that car. This will certainly go against the norm as 86% of all new cars and 55% of used cars have financing (Experian 2015 4th Quarter Report). One of my good friends role modeled this for me. Let me tell you how good it feels to pay cash for a car and walk off the lot without a monthly payment.

Now, people will argue that it is stupid to pay cash for a car when you can get a low interest rate loan. Two points to counter that argument. First, most used car loans are not as attractive as new car loans. On used cars, I have typically found interest rates in the 3-5% with good credit. The latest Experian Report shows an average new car loan rate of 4.63% and an average used car loan rate of 8.78%. Second, I can make a case that if you pay cash for a car, you will likely buy down significantly and ultimately save in the long term. It is easy to stomach buying a $25,000 car when the payments are divided over 60 or more months. It is a lot harder to throw down $25,000 at once. Therefore, you probably won’t and will save some money by buying a less expensive vehicle.

Why used? Here is an example to emphasize how much the value of a car goes down as soon as you drive it off the lot. Cars are a terrible asset only going down in value (with the exception of some collectible cars).

Let’s look at a new 2016 Nissan Altima 2.5 S. Very nice car. The MSRP is $22,900. We know no one ever pays MSRP so let’s say you walk out the door with the car for $22,000 after taxes. In contrast, on www.cars.com within 30 minutes of my house, I can find a 2015 Nissan Altima 2.5 S with less than 20,000 miles for $14,500. If you were paying cash, you could get it for even less than that. Almost $8,000 saved by being OK with not driving something new off the lot and letting someone else put a few miles on it before you do.

If you are worried about driving a high mileage car, there are lots of cars you can get that are quality, safe vehicles under 50,000 miles for less than $10,000. Take a look on www.cars.com. I think the sweet spot is finding a good car to pay cash for between $5,000-$10,000.

It took Jess and I a while to get ahead of our car payments enough to be able to pay cash for the next one but we were able to do this for our last two car purchases. Even better yet would be to pay cash for a car and then start saving on a monthly basis for a future car. We aren’t there yet but are hoping to continue working on our budget to make this a reality in the next year. For example, if we think we may need a new car in 4 years (based on our current mileage and durability of the car) and we want to spend around $10,000 for that car, we could start saving $208/month. After those 4 years, we would be in a position to purchase that car and there would be no surprises!

Your Financial Homework: Is your car payment getting in the way of achieving your other financial goals? Do you have an opportunity to sell your current car and buy down so you can free up some money per month to pay extra on your loans, build up an emergency fund or increase your retirement savings?

“Experience is making mistakes and learning from them.” –Bill Ackman

When it comes to our finances, we can all relate to the temporary bliss when everything is running smoothly and we feel like we have it under control. Unfortunately, ‘control’ of our finances can leave as quickly as it comes and just when we think we have it all figured out, we look up only to realize we are sucking for air, just trying to keep our head above water.

In talking with hundreds of pharmacists about their financial journey over the past year, I have come to realize that many feel as if they are on the brink of losing control. Despite having a single-person income that is more than double the median household income in the US, they are living paycheck to paycheck. I can often hear the angst in their voice and see the concern in their eyes.

How do I know what this sounds and looks like?

Jess and I were in the thick of this after graduating from pharmacy school when we found ourselves with approximately $200,000 in non-mortgage debt shortly after I completed residency training in 2009. Unfortunately, this number of $200,000 probably doesn’t shock many of you reading, as this is the norm for many new pharmacy graduates. When you consider the average student loan debt upon graduation from pharmacy school now exceeds $150,000 and you tack on a car or two, undergrad student loans, and some credit card debt; you can see that it is not too difficult to be at or above $200,000 in non-mortgage debt.

With this type of debt hanging over your head, all of the sudden the dream of enjoying a good income after working so hard to get through pharmacy school is a distant memory. Some choose to embrace this reality and others continue to live on as if this debt didn’t exist. Those that embrace it often make significant sacrifices in the early years after graduating from school and after a few short years of digging deep to live well below their means, they are off to the races with a solid foundation in place to build upon. On the other hand, those that ignore the reality typically have expenses that equal or exceed their income by overbuying on a home, and purchasing cars and other luxuries that leave next to nothing to give, save for a rainy day, build up a nest egg, or just have some breathing room.

The Struggle is Real

It should be no surprise that we all struggle from time to time with getting this right. We are trying to juggle paying off student loans, buying a home, saving for kids college, making sure there is a rainy day fund in place, saving for retirement, and the list goes on and on. With the reality of trying to balance multiple priorities at once, it shouldn’t surprise us that we as a nation (pharmacists included) aren’t doing this very well. In the US, adults carry more than $890 billion in credit card debt and over $1.3 trillion in student loan debt. Furthermore, a third of all households don’t save towards retirement and the majority of Americans don’t have enough savings to cover an unexpected expense of $500-$1,000.

The Mistakes are Inevitable

With so many competing priorities, the bad months from time to time and bad financial decisions are inevitable. I’ve certainly made my share of financial mistakes.

Have you made any mistakes with your finances recently? Are you beating yourself up because you feel like things should be more in order? Or how about losing motivation because the debt load seems so big or saving for retirement seems so far off?

It’s time to give yourself some grace, and keep moving forward.

Here is the reality. Those that will be successful getting out of debt and building wealth are those that can give themselves some grace in the times where their financial plan gets derailed.

Those that win in the long run don’t dwell on the bad. Rather, they learn from the mistakes, identify where things went wrong and make constant adjustments to ensure things are moving in the right direction. Over time, those constant adjustments result in getting closer and closer to achieving financial independence.

Achieving financial independence is a marathon, not a sprint and those that win will have the patience to learn from their mistakes and keep going.

The Easiest Place to Get Off Track: The Budget

If you haven’t already, make sure to read Jess’s article on budgeting. She nailed it. In my opinion, the budget is the key to winning yet the hardest thing to do and the easiest place to get derailed. If you struggle with the purpose of budgeting, I think you will find her insight helpful.

Jess and I have had our fair share of months that don’t go as we had planned with the budget. Some of these are out of our control such as an unexpected car repairs that cause us to dip into the emergency fund and put a pause on working towards other financial goals. Other bumps in the road that we encounter are certainly within our control and are often the result of becoming complacent with the progress are making. Jess and I have found that when it comes to the budget (which has been the single most important factor in our success so far), touching base with each other once a week or every other week to reconcile our expenses and see our progress throughout the month allows us to be successful in staying on track. When we don’t do this, we take a step backwards in our financial plan.

It is important to identify those areas of your financial plan that you know are critical to do but yet are areas that are vulnerable to falling by the wayside.

It doesn’t take much more than a month or two of getting off track with the budget to say ‘forget about it.’ Stay with it. I promise it will be worth it.

I don’t know about you but budgeting to achieving my financial goals reminds me of my commitment to exercise to maintain my financial health. There are good weeks and bad weeks. There are times where I’m hitting all cylinders and then bam! A few missed days and the plan falls apart for a while. Soon enough, I’m back on the track and then back off. But over the long haul, I have a commitment to make my physical health a priority. Your financial health is no different.

Your Financial Homework: Were you on track with your financial plan before but may have recently hit a bump in the road? If so, start small and pick one financial goal you will accomplish by the end of September. This might be setting your financial goals, starting (or re-starting) a budget, saving $100 towards an emergency fund, establishing an automatic withdrawal through your employer-sponsored retirement plan, or setting up a plan to pay off student loans ahead of schedule. The goal is not to solve your financial problems in one month but rather to pick O.

While Jess and I made some great decisions along our journey to pay off $200K in debt, there are some that I certainly wish we could have back. I recognize there is nothing we can change about these decisions now. My hope is this list will prevent at least one person from making one or more of the same mistakes that I did. It took me a while to hit send on this one since some of these are pretty embarrassing. Nonetheless, here they are…my top 10 financial mistakes.

#1 – Buying a house without 20% down

Jess and I moved to Munroe Falls, OH in the summer of 2009 when I started at Northeast Ohio Medical University. Not knowing the area, we rented for a year and then decided to buy a house in 2010. We got the itch to buy a home and the offering of the first-time homebuyer tax credit exacerbated that itch. As a result, we only put 3% down to get into our house. While the monthly payment for our mortgage was well within our means, we could have waited one more year and banked enough money to put at least 20% down.

I see three main reasons why it is good to put 20% down on a home, even with historically low interest rates. First, with 20% down, you will not find yourself in a situation where you have to pay private mortgage insurance. Second, you are more likely to buy within your means, especially if you desire to get into a home sooner rather than later. Think about it. If you hold yourself true to waiting until you have 20% down but at the same time are eager to get into a home, you will likely lower the price range of homes you are looking at so you can make that happen faster. Third, when you put a chunk down such as 20%, you instantly have some equity in your home so if the market goes down and/or you find yourself in a situation where you have to move sooner than you anticipated, you will be in a better position. Remember, mortgages are structured so the interest is frontloaded so it takes time to build up equity in the home by paying down the principal.

#2 – Delaying the purchase of life insurance

Delaying the purchase of term life insurance when you have a family that depends on your income is outright stupid. Go ahead; call me stupid, I deserve it. I’m not sure what I was thinking. Yes, I had some life insurance coverage through work (1x my annual salary) but nowhere near enough for what you would want to have in place (e.g., 8-12x your annual salary).

I currently have a 20-year term policy just shy of $1 million dollars in coverage that costs only $38 per month. Over 20 years, my payout in premiums will be just over $9,000. That is a pretty good investment for $1,000,000 of protection if my family were to need it in the event of my death within the next 20 years.

#3 – Trying to balance too many financial priorities at once

Jess and I were trying to balance a bunch of financial priorities at once. The problem is that we weren’t doing any of them very well. We were trying to pay extra on the house, save for retirement, start saving for kids college, build up an emergency fund and pay off student loans…all at the same time. While we were doing all of them OK, we weren’t doing any of them particularly well. There is something to be said about focusing on one thing and for us that one thing should have been getting out of our student loan debt as fast as possible so we could start focusing on the other priorities.

I’ve talked to too many new pharmacy graduates with loans that have interest rates above 6% and while trying to pay off those loans, they are also trying to balance buying a home, purchasing new cars, saving for retirement, and so on. Here is the thing. If you have high-interest rate debt (e.g., 6-8% student loans or credit card debt at an even much higher of an interest rate) there is little to debate. Pay it off as fast as you can. This should be your top priority unless you are banking on something like loan forgiveness. Where it gets sticky is when you have low-interest debt (e.g., car loan at 0.9%). Many will advise that it is not wise to pay off low-interest-rate debt at the expense of saving that money. That is an OK decision as long as you are actually saving that money which is often not the case. Why am I a fan of paying off debt no matter what the interest rate? By focusing on maximizing your debt payment within your monthly budget, you naturally limit your other expenses.

#4 – Waiting 7 years to create a ‘legacy folder’ including the will

For whatever reason, the idea of putting together a will seemed intimidating and time-consuming. While it wasn’t as critical when it was just Jess and me, it should have been much more critical when we had the boys. Amongst other things, the will covers what we would like to happen with our kids upon our death. We have all heard nightmare stories of custody issues that happen as a result of someone not having a will in place. As with many things we tend to drag our feet on doing, it wasn’t that bad after all. We used an online will-making site and had it done in under a couple of hours.

As Jess and I were going through Financial Peace University at our church, one of the lessons brought up the idea of creating a ‘legacy folder.’ Essentially, this is one place where you store all of your financial documents and important information so that in the event something happens to you; someone else can quickly get access to what they need to. If you are in a relationship where one person does most of the financial-related tasks in your household, this is even that much more important!

Putting together the ‘legacy folder’ took several hours but it was well worth it. In one place, we now have all of our financial documents. That is a great feeling.

#5 – Taking out student loans without knowing what was involved

I think most of us are guilty of this one. Taking out debt without knowing what we are getting into. For me, it was not understanding what my student loans were all about. I was 18 years old starting pharmacy school and the last thing I cared about was what a subsidized versus unsubsidized loan was or how the interest rate could compound over time at such a nauseating pace. Furthermore, I had little understanding of the repayment options and the advantages or disadvantages to refinancing and consolidating.

#6 – Cashing out retirement funds

I told you some of these were embarrassing and this one might top that list. After Jess decided to leave work to stay home with our boys, she had a couple of retirement accounts floating around from two different employers. For one employer, they kept changing accounts and I would constantly get letters mentioning the account was transitioning to a new plan sponsor. I was having a hard time getting access to these accounts so the money was sitting in a money market fund (this could be a whole separate point in this top 10 list). I got frustrated and since we were trying to pay off debt, we ended up cashing these out. Granted, it did go towards our debt that had interest accruing so that was a plus. However, we ended up paying income tax on the distribution as well as a 10% penalty for early withdrawal. As Dave Ramsey says, that is “stupid tax.”

#7 – Buying a car I had no business buying

In December 2014 as Jess and I were nearing the end of paying off our student loans, I bought a used Lincoln MKX. It was nice. Really nice. Leather heated seats, a moon roof, and an awesome sound system. Here is the problem. I had no business buying this car since I had a perfectly functioning Nissan Sentra with less than 50,000 miles on it. While the Lincoln was used and we paid cash for it, it still cost us $12,000 after we turned in the Sentra. That could have been $12,000 to get out of debt earlier or $12,000 to build up an emergency fund or $12,000 to save for retirement or $12,000 to save towards the kids’ college fund or $12,000 to go on vacation for a few years…you get the point.

According to Edmunds.com, the average monthly payment on a new vehicle in the US is $479. Ouch. If someone is struggling with debt and/or getting control of their monthly expenses, this is often the first area I recommend taking a look to cut back. You won’t miss your car as much as you think you will. I ended up selling the Lincoln MKX 6 months after I bought it (more ‘stupid tax’ to pay). In turn, I purchased a used Nissan Altima with 87,000 miles from my mother and father-in-law. After selling the Lincoln MKX and purchasing the Altima, the difference became our last student loan payment!

#8 – Opening a Lowe’s credit card

As with many store credit cards, we got sucked in by the 5% savings. The problem was that by having that card, we eventually decided to do a kitchen remodel that we probably would have waited on if we didn’t have the card. We could have saved up to pay for it in cash within 4-5 months but we got the itch. We ended up paying it off within a few months of the remodel being finished but still had to pay some interest we wouldn’t have had to otherwise pay.

#9 – Waiting to have a budget

This one is pretty simple yet we, like many others, didn’t have a budget in place for some time to plan and track our income and expenses each month. We were not outspending our income (which was good) but quickly realized it is a WHOLE new world to prioritize and strategize where our income should be going each month rather than reacting to where it went. What was the result for us when we decided to get serious about a monthly budget? Freeing up approximately $2,000 per month that was able to pay off our debts and then fund an emergency fund.

#10 – Misunderstanding about the priority of giving

While Jess and I were constantly giving throughout our journey to pay off $200K in debt, the giving was an afterthought. After all, we had other ‘priorities’ to take care of. In hindsight, this is laughable considering we created those ‘priorities.’ When we started making this a priority by giving the first % of our income, something magical happened. Our hearts changed towards doing this. We were humbled with what we had been given to us rather than trying to chase more. If giving is important to you, make it the first thing you do and budget off of the rest. For example, if you want to give away 10% of your income, set your budget off of 90% of your pay. Regardless of your religious beliefs, giving before spending really puts things into perspective.

Your Financial Homework is to take action on at least one thing based on this list. Whether it is making sure you have adequate term life insurance in place, putting together a will, or putting the pen to paper to create a monthly budget, we all have room to improve upon something. Take that one step today and share your progress.

This article was written by Matthew Muir, PE, LEED AP BD +C. Matthew is a 2006 graduate of Ohio Northern University and currently works as a Mechanical Engineer at Advanced Engineering Consultants. He has some good points for us all to consider as we think about taking on any loan. If you have any questions about his article, feel free to comment on the blog or e-mail him directly at[email protected]

Quantifying debt can be challenging. You just graduated from college, purchased a home or took out a car loan. If you haven’t been reading Your Financial Pharmacist’s blog and saving up for a long time, you probably don’t have the cash flow upfront to fund a large purchase. For the sake of discussion, let’s assume you go to the bank and take out a 5-year loan for $25,000 to buy a new car. The bank hands you a check and you walk out the door with $25,000 in debt, right? Not so fast.

I’m going to challenge you to think a little differently. From now on, quantify debt by taking into account the total amount of money you will pay over the term of the loan, not just what you borrowed. Ready to get started?

Loan Amount (Balance or Principal you Owe): $25,000

Interest Rate: 6.0%

Term (Months): 60 Months

Before we start drawing conclusions, let’s talk a little more about how loans work. When you make your monthly payment, the bank divides your payment up into two categories: principal and interest. The principal is applied toward the balance of the loan ($25,000 in this case) and the interest goes into the bank’s pocket. The first payment of any loan is the most depressing one; you pay the most interest you’ll ever pay and the least principal you’ll ever get credit for (per monthly payment). Look at the numbers:

Bottom line: $480.95 of the $483.32 goes toward paying off your loan, that’s 99.5%

Yikes! If you paid the minimum payment for the life of the loan (5 years) than you would have paid a total of $28,999.23 (principal: $25,000, interest: $3,999.23) for your new car, which means you paid 16% more for the car than the dealership was charging. $4,000 might not seem like a lot of money to some, but keep in mind the loan amount and the term we looked at. Imagine what those numbers might be on a $250,000 house loan over 30 years. Scary, isn’t it?

Loan Amount: $250,000

Interest Rate: 4.0%

Term (Months): 360 Months

Monthly Payment: $1,193.54

Total Interest Paid: $179,673.77

Loan Amount + Total Interest Paid: $250,000 + $179,673.77 = $429,673.77 (that’s not a typo)

Seeing that number makes me sick. (Hold on for a minute while I locate the nearest trash can!) By showing you these numbers, I’m not trying to discourage you from buying a house or borrowing money for a purchase, but instead trying to encourage you to pay off your loans quickly to minimize the extra money paid in interest so you can keep more of your hard-earned money. How do I do that? I’m glad you asked. The good news is that you are already on your way.

Know how much money your borrowing, for how long and how much it’s going to cost you if just pay the minimum amount over the full term of the loan (we covered this today). Shop around for the best interest rate. Credit unions can sometimes offer a better rate than a larger bank (less overhead).

Don’t pay just the minimum payment. Start by rounding your payment up every month. In my new car example, around $483.32 up to $500.00. You won’t miss the additional $17.00 per month, and at the end of the first year, you will have paid an additional $204 toward the principal on the loan. If you can, increase the amount you pay even more.

Stick to your budget regardless of what income comes in. Did you get a raise or bonus, a birthday gift, or find cash on the ground? Instead of looking at that money as “I wasn’t planning on receiving this money so I might as well spend it.” Use that extra money to pay off your loan quicker.

Take advantage of the months where you get an extra paycheck. If you get paid bi-weekly you will get 26 paychecks per year; 10 months you will get 2 paychecks per month and 2 months you will get 3 paychecks per month. Use the extra paycheck to pay off your loan quicker.

Consider setting up automatic bi-weekly payments (of half your monthly payment amounts). This is a similar principle to what was discussed in item #3. You will actually end up paying extra in principal per year just as a function of how the payment math works out.

Look for opportunities to refinance and consolidate your loan. (Your Financial Pharmacist Comment: This is a big one right now with many student loan borrowers having interest rates on loans in the 6-8%. More to come on this topic in the near future).

Ask for a lower interest rate. Never hurts to ask right? The worst they can say is no.

Cut expenses. Look for financial areas where you can make sacrifices. Cancel memberships and services that you are not using. My wife and I canceled cable and were able to save $50.00 per month. We use Netflix, an antenna, and YouTube and haven’t missed cable at all. Okay, I lied, maybe a little during football season. Go Ravens!

This is not intended to cover all the details about loans or to make you an expert. It’s important to do your research to ask the right questions while applying for a loan. What are the right questions to ask while applying for a loan? I’m glad you asked. Maybe Your Financial Pharmacist will invite me back to answer that question.

If you are reading this and have any other ideas about ways that to pay off a loan more quickly, please share your suggestions in the comments sections.

According to the 2015 Salary Survey conducted by the Ohio Pharmacists Association, the average yearly salary for a pharmacist in Ohio is $121,388.1 In comparison, the median household income in Ohio between 2009-2013 was $48,308.2

It is tempting for us to be lulled into the comfort of an income that is more than 2x the median household income. We worked hard to obtain that degree and should enjoy that income, right? Yes, of course we should enjoy the blessing we have been given but we also have a responsibility to manage that income wisely. It can be easy to become complacent with a six figure salary where your expenses slowly rise while time is ticking away with little to no progress made on other important financial goals such as eliminating debt, saving for retirement and having the ability to help others through giving.

Almost 1/5 (19%) of Americans spend more than they earn3 and 3/10 adults don’t save any portion of their household income for retirement.4 We, as a culture, often spend too much and don’t save enough. The result? Feeling like we are living paycheck to paycheck despite having a six-figure income.

The good news is that for pharmacists we have the hard part taken care of (the good income) and now we need to make sure we are doing the dirty work to manage the expenses side so we can win financially in the long run.

Here are three tips to help you on your journey to achieve financial freedom.

#1 – Get out of non-mortgage debt as soon as possible.

Getting completely out of debt is the ultimate goal, however, here I am specifically talking about non-mortgage debt. For pharmacists, the largest area in this bucket is likely to be student loans. According to the 2014 National Pharmacist Workforce Study, pharmacists within five years of graduation carry an average debt load of the $108,000. In 2004, that figure was just $42,000.5 A six-figure debt coming out of school is A LOT of debt.

There are two main reasons why I am a proponent of paying off debt as soon as possible coming out of school rather than making payments over 10+ years. First, you gain some momentum with early financial wins that will give you some breathing room and empower you that you can succeed long term with your personal finances. Second, it often forces you to get serious about making a budget to avoid adjusting your lifestyle up too much when you take that first job. What does minimum payments do for you on your student loans? For someone that isn’t disciplined, it may give him or her the impression they have more room in their monthly budget than they actually do if they were paying these loans off faster. The result? Often living up to a higher income by making a significant home purchase, buying nice cars, clothes, etc. because there is more cash flow ‘available’ on a month to month basis. There is nothing is wrong with enjoying some of your income but I’m convinced that the lifestyle you maintain in your first 5-7 years out of graduation will be close to the lifestyle you maintain in the long run. Therefore, if you make a commitment to pay off loans faster, you will be more likely to set a budget and keep your expenses down over the long run.

If you have low interest non-mortgage debt (e.g., student loan at 3%, car loan at 2%, etc.), there can be an argument made to pay minimum amounts on those loans to also focus on saving for retirement where you may have a higher return on your investments. However, if you, like I did, have many high interest rate loans (6-7%), I don’t think that argument carries much weight and would urge you to focus on getting out of debt before focusing heavily on achieving other financial goals (e.g., retirement savings, buying your dream house, etc.)

Why all the fuss about getting rid of debt? If not managed properly, it can hinder your ability to save for the future and give you the feeling of not making much momentum towards achieving your financial goals. For example, according to the 2015 Consumer Financial Literacy Survey, 58% of those paying off their own student loans or children’s loans noted being unable to establish emergency or retirement savings or purchase a car due to the financial commitment those loans required.4

#2 – Work towards putting away 15% of your gross income per year.

Some of you may say, “check, already done.” For others this will be a gut check. If you do the math on 15% of the average salary quoted earlier in this article that would be $18,208 per year or $1,517 per month. It is hard to put away that kind of money when you are strapped with debt and as I suggested earlier, I would wait on making serious progress towards this goal until you are out of debt; especially if you have high interest rate student loans.

If you can get in this habit early, it will pay off BIG TIME in the long run. The two keys to building a large nest egg that will last you throughout retirement include time (1) starting as early as possible so compounding interest can do the hard work for you, and (2) being consistent (doing this every month over many years). I shared in an article recently on Pharmacy Times that a pharmacist doing this out of graduation should easily become a multimillionaire in his/her lifetime. If 15% seems to big of a jump to start, just like we counsel patients on diet and exercise, start small, get some wins and build off of those wins. Maybe it starts at $100 or $200 per month.

#3 – Budget off of a reduced portion of your take home pay.

I get it. It’s not that sexy topic to talk about, but if you are struggling with managing your day-to-day finances and feeling like you should have more money available earning the type of income you do, it is time to get serious about setting a budget. This was the hardest but yet most impactful part for my wife and I in our journey to pay off $200,000 in debt. The budget we used to do this was pretty intense but allowed us to make significant progress in a short period of time to keep us motivated along the way.

I am convinced that the key to being successful with debt elimination and saving for retirement is this step. You have to make debt elimination and retirement savings a priority, rather than an afterthought, and the way to do that is by making them a line item in your budget.

In order to free up the money to do steps #1 and #2, get in the habit as soon as possible to set your budget off of some reduced portion of your take home pay. For example, if your take home pay is $7,000, set a budget at 75% or $5,250 per month. Now we have $1,750 per month to throw at debt, save for retirement, purchase a home, boost our giving, etc. I get it. It is hard and sounds way easier than it is. I’ve been there. But when your financial priorities become a priority through which you set the rest of your budget, the magic begins to happen.