Intro to the Side Hustle Series

Summary of Episode

On Episode 063 of the Your Financial Pharmacist Podcast, Tim Church, YFP Team Member, introduces a new segment called the Side Hustle Series to talk about ways pharmacists can create additional streams of income to reach financial goals faster and to highlight pharmacists who are doing this to help you get inspired. In previous episodes, topics about how to budget, limit and cut expenses, and being frugal have been talked about, but what hasn’t been discussed as much is increasing or maximizing income. As you may know, there is incredible buzz and interest around the topic of a side hustle for pharmacists and many have a side hustle to earn extra income and pursue other interests and passions.

Mentioned on the Show

- Script Financial

- YFP Episode 053: One Pharmacist’s Journey from Financial Ignorance to Financial Independence with Tony Guerra, PharmD

- YFP Episode 009: Interview with Carrie Carlton

- The Happy PharmD

- YFP Episode 007: Maximizing Your Income with Alex Barker, PharmD

- When Eating Right Isn’t Enough: The Top 5 Medications to Control Your Type 2 Diabetes by Tim Church, PharmD

- Seven Figure Pharmacist by Tim Church, PharmD and Tim Ulbrich, PharmD

- Your Financial Pharmacist

- The Smart Passive Income Podcast

- The Go Giver: A Little Story About a Powerful Business Idea by Bob Burg

- 53 Side Hustles Any Pharmacist Can Easily Start by Alex Barker

- Email YFP About Your Side Hustle

Episode Transcript

Tim Church: What’s up, everybody? Welcome to Episode 063, which is all about side hustles. Now, those of you listening may be thinking, who is this imposter and what happened to the other Tims? Well, don’t worry. They will return. I’m just giving them a break. They really do an incredible job, which is evident by all of your positive comments and feedback, and we truly appreciate that. Well, I’m the other Tim and have made a few appearances on the show over the past year, but I decided to take the lead on this topic of side hustles. That’s something that really interests me. We talked a lot in many episodes about how to budget, limit and cut expenses, and just being frugal in general, but not so much about increasing or maximizing income.

As you may know, there’s an incredible buzz going around and interest around this topic of having a side hustle or side hustling. And there’s many pharmacists out there who are doing this to earn extra income and pursue other interests and passions. Some of our most popular episodes have been highlighting those who are working in some unique roles and pursuing non-pharmacy careers on the side — and I’ll definitely put those in the show notes. So because of this, we wanted to make this a regular series to continue to highlight these stories because we believe they’re truly inspiring and can help spark some creativity. So what the heck is a side hustle? Well, a very basic definition is a way to make extra cash beyond your main source of income. So really, that could be many different things that would fall under that. It could be something as simple as working a second pharmacy job besides your full-time gig, so working at a hospital while you’re working your full-time job as a community pharmacist or vice versa. Sometimes, people also refer to a side hustle as a passion project, something that they’re really called to pursue. And again, that could be something that’s not even pharmacy-related. For example, I know a pharmacist who has driven for uber on the side, and he absolutely loved the experience. Back in Episode 053, the other Tims interviewed Tony Guerra, and some of his side hustles include real estate, writing books, and podcasting. In Episode 009, we had Carrie Carlton on the show, and she discussed how she acquired 18 rental properties. So real estate has just been huge as a side hustle for her. My friend Alex Barker of TheHappyPharmD.com, who has been on the podcast a few times has been side hustling for a long time, doing many different things with providing career coaching to other pharmacists and creating online courses, just to name a few. He actually has turned his side hustle into a full-time job as he just recently had his last day at the VA hospital. So I want to shout out to Alex and just say congratulations. But the bottom line here is that there’s a lot of options out there.

So oftentimes, the questions comes up, why even pursue a side hustle? Pharmacists make a great salary, right? But I think a lot of people are interested in making more money, and that’s what it comes down to, what people really think about when that topic of side hustling comes up is I want to make extra money. There’s certainly nothing wrong with it, and that point is one of the major reasons why I pursued, started side hustles. But I think many times, it really goes deeper than that, and you have to ask yourself the question, Why do I want to make more money? I think there’s some current realities going on in our profession on why it really does make sense to consider a side hustle. Since 2011, the average debt-to-income ratio is rising as pharmacists’ salaries are not keeping pace with the rising student loan debt. And this means that more pharmacists are starting out in a worse financial position than pharmacists who have graduated in previous years. Traditional pharmacist positions also typically have a salary where it starts out high, but then small raises occur over time, typically based on some merit or time being spent there at the job or a combination of both. And furthermore, some companies are cutting pharmacists’ full-time hours. So instead of full-time being 40 hours or somewhere around there, it’s now down to 32 or something less. And that’s actually leading to some substantial pay cuts for pharmacists. So I don’t think you can ignore the reality of what’s happening with pharmacy jobs out there.

But besides that, I think a lot of people, the reason for wanting to pursue a side hustle is they want to accelerate their financial goals and get them done quicker. For example, student loans, obviously a big problem. And that was one of my main motivations is really getting these student loans out of my life a lot faster. A lot of people want to retire at an early age, and in order to do that, they have to save more money for retirement and invest more, and they have to get a side job in order to do that. Some people want to donate more money or help other family members and friends out financially. Perhaps you want to upgrade your lifestyle. A lot of people want to go out to better restaurants, go on better vacations, buy better clothes. There’s certainly nothing wrong with that. But as we’ve talked about many times, there’s a tendency to live up to and even beyond your means, and so sometimes making more money can actually make your financial situation worse.

The other reason for wanting to pursue a side hustle or why you may consider it is that relying on one source of income can be risky. Although many pharmacists’ jobs are thought to be secure, with the changing job market, things are not what they used to be. And so the demand is not as high as it was. There’s still definitely a demand out there, but everybody is susceptible to losing a position. And so having a second stream of income or multiple streams of income can give you that additional layer of security.

Beyond some of the monetary reasons behind pursuing a side hustle, I really think the big one is passion. So something you truly feel passionate to work on that’s meaningful, that gives you the results or feeling of happiness and self-satisfaction. And oftentimes, that’s a great combination, that you’re working on a project or doing something that the end result may be that it provides you with some additional income but is something that really fires you up, something that gets you up in the morning.

So I want to spend a few minutes talking about my personal experience with side hustles. By no means am I the expert on this; there’s definitely a lot of pharmacists who I mentioned earlier that are bringing a lot more money and are a lot more successful, but I want to just give you a few tips on kind of how I started with this.

So why did I start exploring side hustles? This was a couple years after I started my full-time job and after I finished residency. And initially, my main motivation was getting extra cash so I could get in a better financial position. I came to this realization that I was broke and that student loan debt at the time was totaling about $200,000, which is a combination of undergrad and graduate school. And I had to make some changes to get myself in a better position. Now, of course I scaled back on spending. I got on a tight budget. But I was looking for some opportunities to maximize my income. So I really wanted to reach my financial goals faster, that was my main motivator, that’s why I wanted to do it.

Now, my full-time job is working as an ambulatory care specialist at the VA hospital, where I have clinics to manage, chronic diseases, diabetes, high blood pressure and a number of others. My schedule is 7:30-4 Monday through Friday. Most of the time that I have available for side hustling is in the evening and on the weekends. Sometimes I’ve heard in books people who do a lot of their side projects on the weekends, they’re called “Weekend Warriors.” So that’s kind of how I viewed myself during some points of time when I’ve been doing this. The easiest thing that I came across on what I could do to earn some extra income was just do some staffing, some in-patient staffing at the VA after I would finish my day as an am-care pharmacist. And so that was a really easy thing to do because literally, all I had to do was press a button and go down an elevator a couple floors and really start my side hustle there. So that was a really easy, very convenient way to get some extra cash. It wasn’t always that consistent but definitely was a great opportunity early on.

The other thing that has come up is some special projects where I was able to get overtime. And still occasionally, this happens. But the opportunities don’t come about as much as they used to. So while those things were definitely great, they weren’t consistent. So I wanted to get something where I could have a more reliable extra income coming in. And for the first year and a half, I didn’t have a Florida license because I had graduated from a school of pharmacy in Ohio, and so that kind of limited my other options of what I could do working as a licensed pharmacist in other areas. So eventually, I became licensed in Florida, and I started looking at other opportunities that I could do working at another hospital or community pharmacy nights or weekends. And it took me a couple months, but eventually, I was able to find an opportunity at a local hospital. And this was really great because they were very flexible with my schedule, as soon as I was done at the VA, I could come in and work for a couple hours in the evening. And really, weekends were available too. And so this was a great way to really put a big chunk of extra money every month towards my student loans. So I was easily bringing home an extra $1,000, sometimes $1,500 a month. And I thought this was just a great opportunity.

But what started happening was is after about a year and a half, I really was getting burned out by all these extra hours. So sometimes, I was working close to 60 hours a week. And the other thing was I wasn’t getting really excited about the work that I was doing. The other element that came into play was I got married during this transition when I was doing the extra staffing. And so it’s another element that came into it and made it a little bit more challenging because I was spending so much time working. So at that point, I kind of said, what else can I do? Or what are some other opportunities where I don’t have to physically be present and work all these additional hours but still try to figure out how to get some additional income?

Well, after I finished my residency program and through this time that I was working the hours at another hospital, I really became a voracious reader, focusing on the areas of personal growth, business, psychology and personal finance. And really, because of that, I developed an interest in trying to pursue other things than just a traditional pharmacist’s role. And that led me to my first side hustle sort of outside of just a traditional pharmacy role, which was book writing.

And so after I read a couple books on how to write books because the technical aspects were a little intimidating for me, I felt like I could give it a try. So given diabetes management is one of my specialties, I thought writing a book for patients was a great idea since I can only reach a limited amount of patients in my full-time job. I was so excited about this and thought I was going to sell this thing like crazy through Amazon, I wouldn’t have to do anything but look for the money to be deposited in my checking account. Well, long story short, that’s not what happened. And to this day, I still have not recouped the money that was invested into the book, which was really only about $1,000 since I went the self-publishing route. But what’s interesting though is that every couple months, one or two people will buy the paperback book or Kindle version, and that actually brings in a royalty of a couple dollars. So I get a good laugh out of that because of how far off my expectations were. But at the same time, I did the work once, and it still has the opportunity to bring in more income. And so this is obviously a much more passive stream of income than physically being present and working in a traditional pharmacy role like I was doing when the extra staffing.

Well, this failure with my diabetes book or what I’m going to call it, a learning project, was really important, though, because it kind of helped set the stage for my next project, which was writing “Seven Figure Pharmacist” with Tim Ulbrich. Now, that has actually brought in some consistent revenue every month. My first book gave me the confidence in the process of not only writing and getting all the pieces in order, but really to get from that vision to reality and figure out how to actually get a good reach and sell the book.

And so besides the book, my other side hustle — as probably you could have guessed — has been working with YFP, Your Financial Pharmacist team, creating content, managing the website, among a bunch of other things. And this is something that I’m truly passionate about, and I’ve believed in Tim Ulbrich’s mission since he started the company in 2015. As I shared on previous episodes, I struggled with my finances for awhile, so the idea and the opportunity to help others and help prevent them from making the same mistakes that I did is just a great experience and something that really does motivate me and want to continue to work on this project and work on this side hustle.

So that’s really a quick snapshot of my experiences that I’ve had with side hustles. And I mentioned that when I started off, really it was really mainly money. I was looking for additional income; it was the bottom line. I mean, it was a very cut-and-dry reason. I wanted to get my student loans paid off faster, so what can I do to get more income? But eventually, it really — passion has been a huge driver for me for a lot of the things that I’m doing.

So if you’ve thought about a side hustle or are thinking about what else can you do to bring in additional income or what can you do that is something that you’re very passionate about, what are some things that you can do to get started? So I think the easiest thing to consider is that if you’re really just looking for an additional stream of income, you don’t care how you do it, then obviously looking at other pharmacy jobs out there where you can do some shifts, maybe even at your own institution or organization where you work, looking at different special projects that they have, something that’s a different time than your main hours, I think that’s obviously, that’s an easy one. And that’s what I did. But if you’re thinking about something other than that, then here’s some questions I think you can consider.

The first one is what knowledge or experience do you have that others would find useful or valuable? So obviously, you have very high competency with pharmacy-related topics and things when you graduate, but everybody has a very unique background and experience. And I had a lot of pharmacists in my class that had other careers, even prior to pharmacy. And I think that has helped shape a lot of what they’re doing now. And I think that’s something that you really have to consider is to bring into the picture because it doesn’t always have to be something pharmacy-related or it could be a combination of something pharmacy-related and something that’s not. Is there a hobby or passion that you have that you could actually monetize it? So I think that’s another one to think about. And the other one is, are there problems out there that people are willing to pay to have solved? And I think this is a big one and just a great way to think about entrepreneurship in general. When I started getting interested in this idea of side hustles, I was listening a lot to the Smart Passive Income podcast by Pat Flynn. And he always makes a point of this, that when you’re looking at different businesses and opportunities that you’re really looking to solve people’s problems. Can you solve them better than what the options are available now? Or do you have new and innovative ways on how you can solve people’s problems? So I think that’s a great way to think about that.

And as I mentioned, there’s a number of different motivators for wanting to do a side hustle. Maybe purely financial, maybe some other reasons, but I also think you have to have the right mindset. One of the most inspiring books I’ve read over the past couple years is a book called “The Go-Giver” by Bob Berg. And in this book, there’s really a story that goes on, and he talks about a lot of different laws that apply. And one of them that really stood out to me is called the Law of Compensation. And that basically states that your income is determined by how many people you serve and how well you serve them. So a lot of times, instead of asking the question, how do I make more money? I think a better question is, how can I provide more value to others? And by doing that and providing more value to others that the income eventually will come.

Now, if you’re looking to get some ideas for side hustles, I recommend you check out my friend Alex Barker. He has a post called, “53 Side Hustles Any Pharmacist Can Start Today.” And you can find that on his blog called TheHappyPharmD.com, and we’ll put that in the show notes. And in future episodes of the series, we’re going to talk about some more specific ideas and some things that you may not have even considered.

So moving forward with this series, I’m going to be interviewing other pharmacists who have a side hustle and really get into some of the details of what they’re doing, how they actually make money, how much money they’re making — when they’re comfortable with sharing that, of course — and how the heck they balance being a full-time pharmacist, having a personal life, and then also their side hustle. Because I think a lot of people manage this differently and depending on your personal situation and where you are, even the thought or the idea of doing something extra I think can be very daunting, especially if it’s something that you’re not truly passionate about. So I think it’ll be great to hear some of those experiences moving forward.

Now, if you have a side hustle and you want to be featured on the show, please reach out to us at [email protected]. Even if you’re in the beginning phases and just starting out, we would love to hear from you. So we’re really looking forward to hearing and learning about your stories in episodes to come. And so I’m just really excited about this series, so please if you have any comments or feedback, please reach out.

Join the YFP Community!

Recent Posts

[pt_view id=”f651872qnv”]

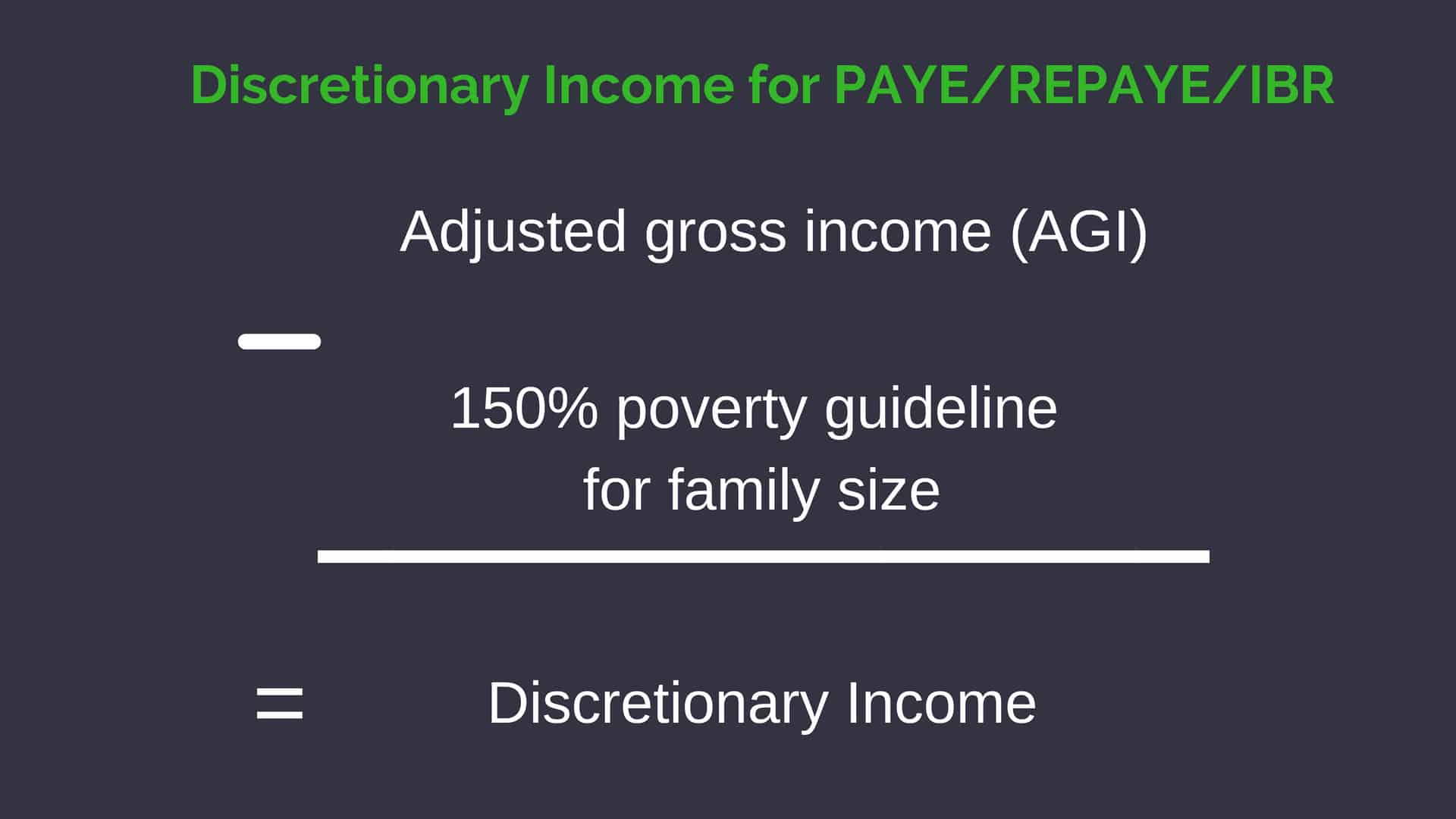

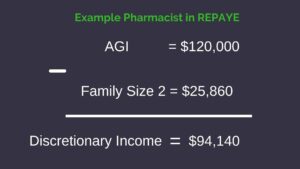

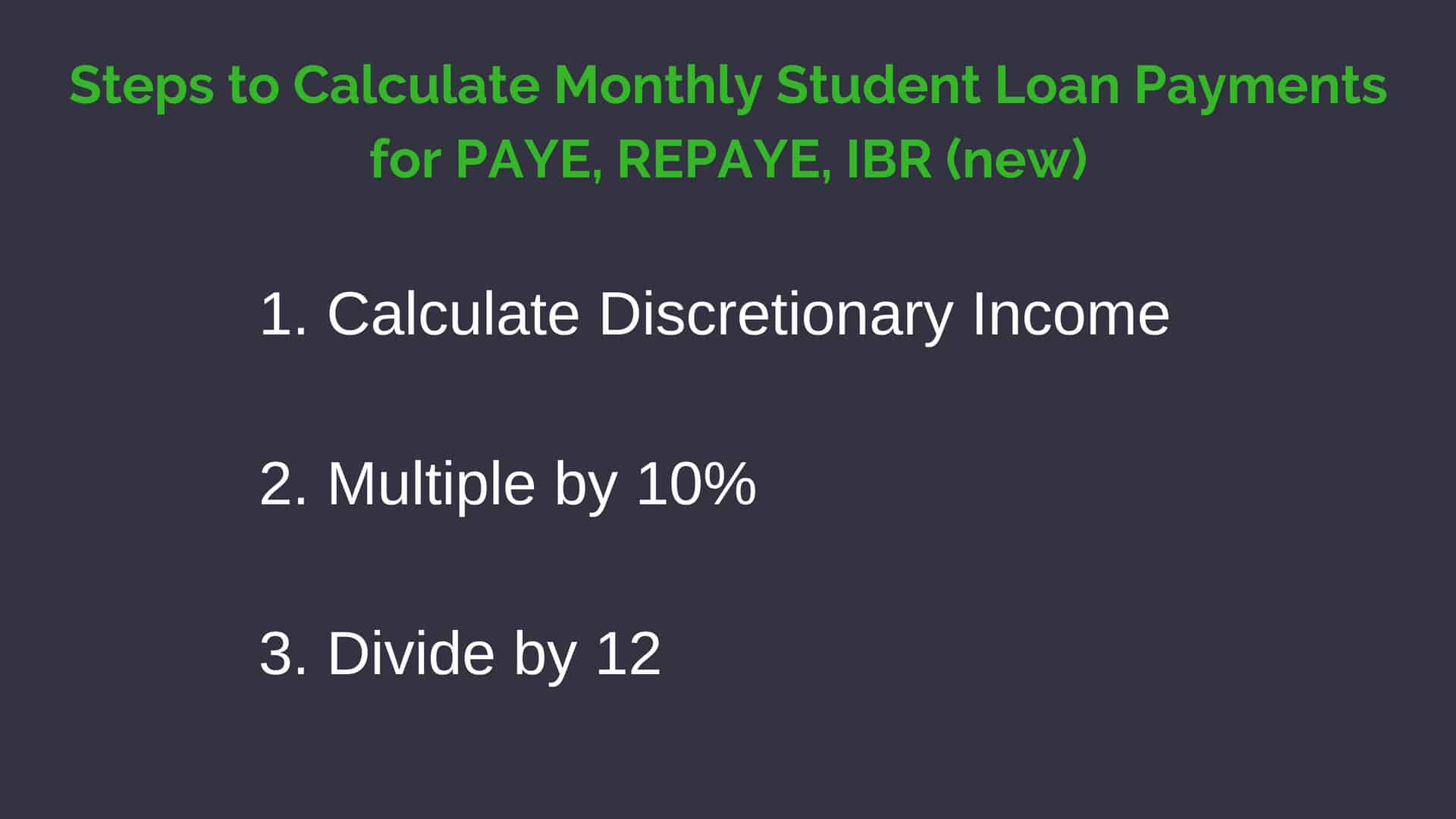

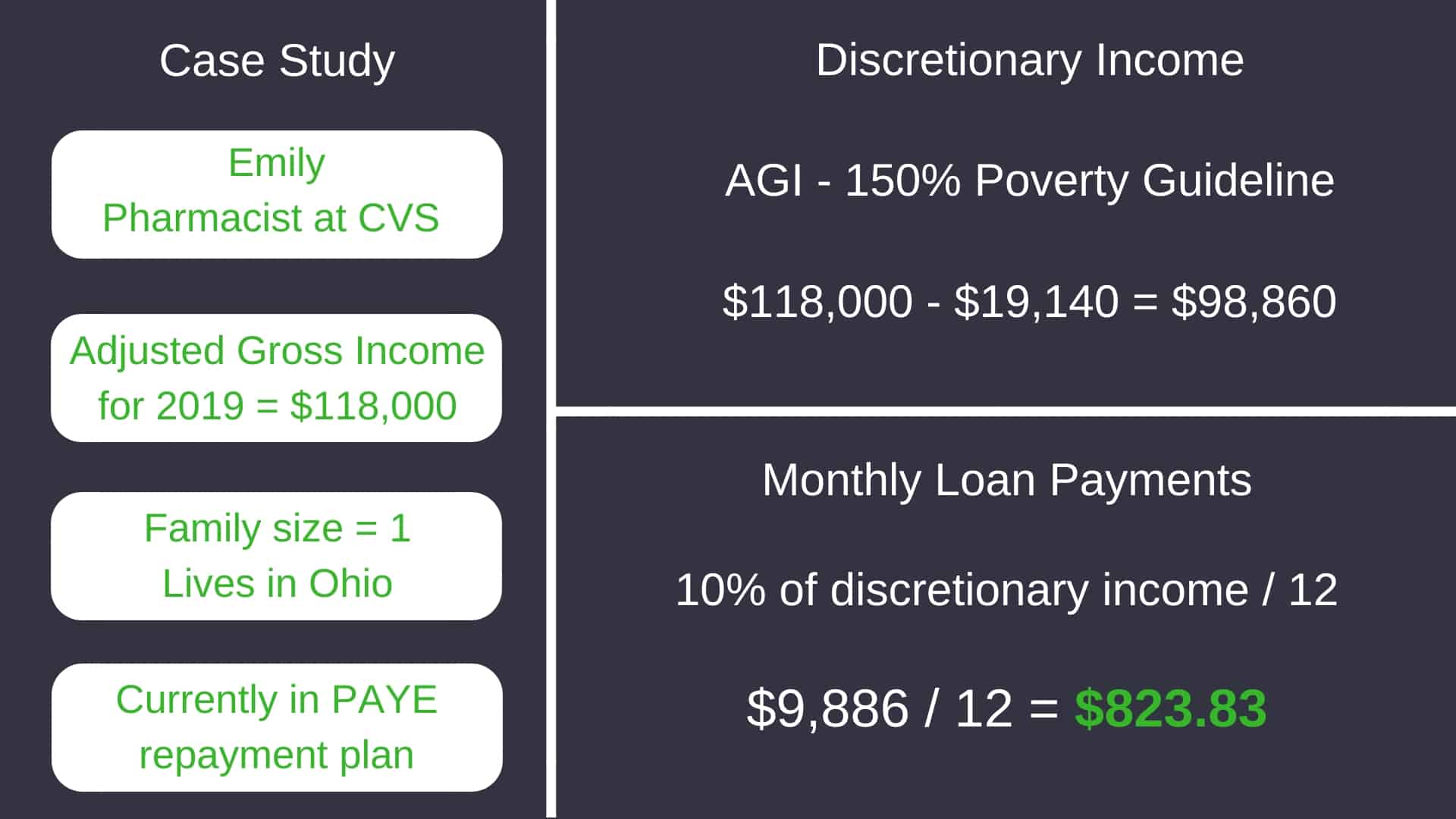

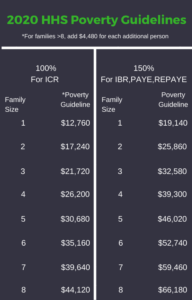

The specific income driven repayment plan will determine what percentage of the poverty guidelines is used in the calculation. For most plans including Pay-as-you earn (PAYE), Revised pay-as-you-earn (REPAYE), and Income-based repayment (IBR), it is 150%. For Income contingent repayment (ICR), it’s 100%.

The specific income driven repayment plan will determine what percentage of the poverty guidelines is used in the calculation. For most plans including Pay-as-you earn (PAYE), Revised pay-as-you-earn (REPAYE), and Income-based repayment (IBR), it is 150%. For Income contingent repayment (ICR), it’s 100%.