On this episode of the Your Financial Pharmacist podcast, we finish our month long focus on how couples work together on their finances.

In Episode 36, we speak with Andria and Tim Church who share their story about how they first met and how their approach to their finances evolved over the course of their relationship. Andria and Tim share their wins and their struggles and impart valuable advice to other pharmacists and couples that are working together on their finances.

Featured on the Show

How Tim Church used Andria’s interest in primary care to court her

The Church’s struggle with budgeting, combining finances

Their “gazelle intensity” towards their student loans enroute to payoff and acquiring the Church family cat

How being budgeting, being frugal, side jobs and student loan refinance helped along the way

On Episode 035 of the Your Financial Pharmacist Podcast, Tim Baker, CFP interviews Sarah Stanley Fallaw, Ph.D, the founder and President of Data Points and they discuss money tips and behavioral finance. Sarah is continuing the study of wealth in America started by Thomas J. Stanley, Ph.D. using analytics to identify and develop wealth potential.

If you’re like most pharmacists, student loans will be your biggest expense aside from a mortgage, and a major barrier to achieving financial freedom.

Other than some of the forgiveness and tuition repayment/reimbursement programs available, dying, or becoming permanently disabled, you’re pretty much stuck paying them off.

If your goal is to pay off your loans as fast as possible, you essentially can do one of two things to accelerate the payoff: increase your income and/or decrease your expenses to make bigger payments.

While these strategies are powerful and arguably most important, there’s another tactic that can help: refinancing

When you refinance your student loans, you change the terms of the loan which could be the interest rate, type of interest rate, time to repay, or a combination of those.

While refinancing can be a good move, it’s not for everyone. If you’re pursuing or plan to pursue the Public Service Loan Forgiveness (PSLF) program you will automatically lose your eligibility if you refinance.

Also, if you need an income based repayment plan, can’t get a lower interest rate, or can’t make big monthly payments based on the new terms, then refinancing probably isn’t the best move right now.

However, if that doesn’t apply and you’re thinking about refinancing, here are the top reasons why you should.

Big Potential Savings

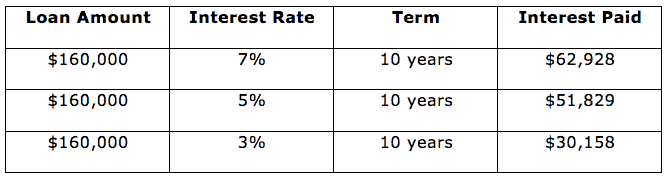

Pharmacy graduates are now facing an average student loan debt of $160,000.

If that’s paid back over a 10 year period with a typical federal interest rate of 7%, the amount paid in interest would be $62,928. Ouch!

Let’s look at what the savings would be if the loan was refinanced to a 3% or 5% interest rate and the loan is paid back over 10 years.

Refinancing to a 5% rate results in a $11,000 savings but a 3% rate results in over $30,000 in savings!

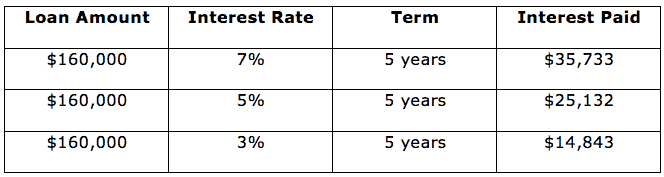

What if you want to be aggressive and knock out the loan in 5 years.

You can see the savings between interest rates isn’t as big the faster you pay off the loans but it’s still pretty substantial and the overall interest paid is significantly less than the total over 10 years.

If you want to calculate your potential savings with a new interest rate and time to payoff, you can check out our free student loan refinancing calculator.

Catalyze Your Payoff

When I refinanced my student loans a couple years ago my minimum payment went from about $1,000/month to $2,700/month. While some people refinance their loans to lower their monthly payment, I almost tripled mine.

In order to get the best interest rate, I had to refinance to a 5 year term resulting in that big monthly payment. However, that wasn’t the only reason for this move.

I wanted to get rid of my loans as fast as possible and wanted to eliminate one of the biggest barriers to my progress: myself.

When my monthly payments were $1,000, I had some disposable income in my budget and could have paid extra on the loans. But do you think I did that each and every month? Of course not. I spent it!

Being forced to make $2,700 monthly payments on auto-draft minimized the opportunity to spend money on things that were not consistent with my big financial goals. Refinancing jump started my payoff and forced me to be intentional.

If you’ve been making monthly payments through one of the income-based or extended plans you may have no trouble making your minimum monthly student loan payment but you also may not be making much progress. Refinancing can help you get focused and serious about paying off your loans.

Cash Bonus

Beyond the savings in interest you can get from refinancing, many companies also offer a cash bonus just for being a new customer. Obviously, they make money off you from the interest you pay over time but it’s a great perk and better than paying a fee for the service.

We have partnered with some reputable refinancing companies that offer great cash bonuses. Full disclosure here. We get a small amount when you refinance using one of our links but we have negotiated to make sure most of the bonus goes to you.

You can see the offers below or on our refinance page. Checking your rate does not affect your credit and takes just a few minutes. I would recommend checking them all to see the best rate you can get.

Even if you refinanced in the past, you can do it again, and could be a good move if you can get a better rate.

[vc_custom_heading text=”Check out these companies to find the best interest rate. ” font_container=”tag:p|font_size:28|text_align:center|color:%23343341″ google_fonts=”font_family:Montserrat%3Aregular%2C700|font_style:700%20bold%20regular%3A700%3Anormal”][mk_custom_list margin_bottom=”10″ align=”center”][/mk_custom_list][vc_custom_heading text=”If you refinance student loans using one of the links below we’ll both get a bonus. We take just a small amount to make sure you get the highest bonus possible. Checking your rate will not impact your credit score. ” font_container=”tag:p|font_size:21|text_align:center|color:%23343341″ google_fonts=”font_family:Montserrat%3Aregular%2C700|font_style:700%20bold%20regular%3A700%3Anormal”][mk_padding_divider size=”25″][vc_separator color=”custom” border_width=”6″ el_width=”10″ accent_color=”#343341″][mk_padding_divider size=”25″]

Credible Disclosure: To check the rates and terms you qualify for, Credible or our partner lender(s) conduct a soft credit pull that will not affect your credit score. However, when you apply for credit, your full credit report from one or more consumer reporting agencies will be requested, which is considered a hard credit pull and will affect your credit.

On this episode of the Your Financial Pharmacist podcast, we continue our month-long focus on how couples can work together to manage their finances.

In Episode 34, we interview Ellen & Ethan Ko who chronicle their journey walking through the valley of debt as a young couple, how they have managed to work together through financial hard times and what they are doing differently to be on the path towards financial freedom. Ellen is a 3rd year pharmacy student at VCU School of Pharmacy and Ethan is a physician that is trained in internal medicine with a subspecialty in nephrology.

In Part 2 of a series on Finding Your Why, Tim Baker, CFP, interviews YFP Founder Tim Ulbrich and his wife, Jess Ulbrich, by asking them a series of questions designed to help them envision what financial success looks like for them in 2, 5, 10 and 30 years into the future.

In this two-part series, Tim & Jess Ulbrich invite the listeners into their Find Your Why client meeting with Tim Baker, CFP.

In Part 1 of this two-part series on Finding Your Why, Tim Baker, CFP, interviews YFP Founder Tim Ulbrich and his wife, Jess Ulbrich, by asking them three life planning questions that challenge them to uncover their beliefs about money, their long-term financial goals and ultimately, why they want to achieve financial freedom.

In this two-part series, Tim & Jess Ulbrich invite the listeners into their Find Your Why client meeting with Tim Baker, CFP.