By Tim Baker, CFP

YFP Team Member & Owner, Script Financial

For many, knowing where to begin in order to get their finances in order is half the battle. There is much to consider and putting together a financial plan can definitely be overwhelming. However, whenever I examine a client’s financial health, the first two things I review are their emergency fund and their consumer debt level. Let’s look at both of these in detail.

Emergency Fund

It might seem obvious to some why an emergency fund is important, but that might not be readily apparent to everyone. This fund is important for a variety of reasons. First, having cash in an account gives you peace of mind. You know in the event of an emergency, you can easily access it and use the money as needed. Second, an emergency fund allows you to avoid credit card debt, which can be extremely costly. We’ll get into greater detail in a bit. Finally, the emergency fund buffers your investments, so you can take intelligent risk in the market and keep that money working for you. So, now we know why an emergency fund is important, but how much do you need? Great question!

The answer is…well, it depends, which might very well be the worst answer ever. Hold your horses. The amount of your emergency fund depends on two things: your non-discretionary monthly expenses (heh?) and how many income earners there are in your household. Let’s break down each of these. First, what the heck are non-discretionary monthly expenses? Basically, these are expenses you pay in order to live or to keep the lights on, so to speak. These expenses go out the door whether you are employed or not. Examples include a rent or mortgage payment, utilities, food, debt service payments, etc. The second factor is the amount of income earners in your household. If you are a single income earner, you’ll want to save 6 months of your non-discretionary expense. If your household is dual income, you can lower that to 3 months of non-discretionary expenses. Why the difference? Well, if you have two incomes, it’s unlikely that both you and your partner would lose their job at the exact same time and the still-earning partner will help offset your loss of income.

If you are a single income earner, you could be up a creek for a while, so the 6-month reserve makes more sense. And you may be thinking, “Wow, Tim, I need $25,000 in my emergency fund. You want me to keep that in a savings account earning almost no interest?” My answer to that question is in the affirmative because we need to remember the purpose of our emergency fund. It’s for emergencies, not to make bank on investment returns or interest. Now we know the why and the how much, but what about the where? There are a few things to consider when deciding where you should house your emergency fund. It important that the fund be both liquid and be redeemable at a known price. Cash is the best example of this, but other examples include check and savings accounts, money markets, and CDs. If you’re using your brokerage account invested in common stock or mutual funds as your emergency, pump your breaks. You’re leaving yourself open to the possibility that you may need to redeem those shares at an inopportune time. Also, if you’re thinking your 401(k) or IRA is a good place to hold your emergency fund, think again. If you are under 59 ½ years old, you’ll pay a 10% on top of any taxes you may owe. Ouch.

Consumer Debt

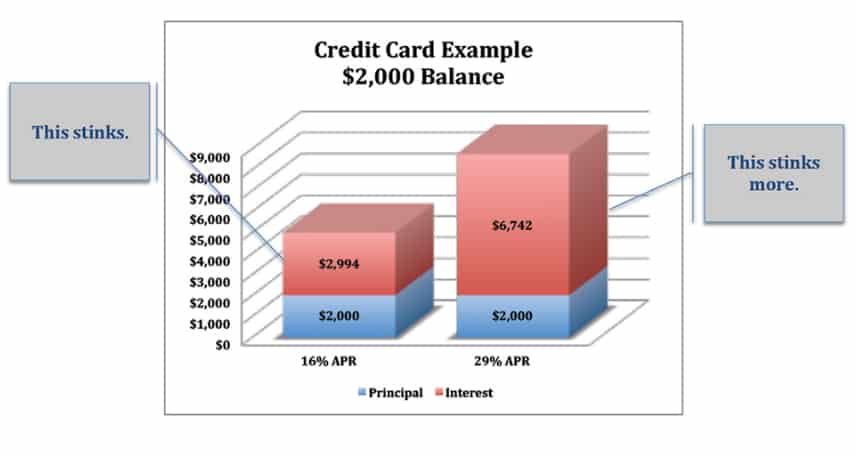

Many Americans today live by the plastic. An age of consumerism, coupled with the need for instant gratifications does not bode well for the American saver. Plus, interest rates offer next to zero (literally!) help with regard to the amount of interest you earn, so there’s no incentive in that regard. As a society we spend first and ask questions later. I remember back in the day when I wanted the latest, greatest Nintendo game, I had to scrimp and save and do extra chores to get those precious $60 together. The prospect of not having Super Mario Brothers 3 was just something I could not handle (do you remember the raccoon and the frog you could turn into? So dope.). Today, for some, it is merely a swipe of the card with the promise to pay it back later. That’s cool and all…if you actually pay it back without accruing significant (or any) interest. Unfortunately, many people use their credit card as their emergency fund [insert horrified emoji here]! To put it mildly, this is a less than ideal emergency fund strategy. The cost of credit, particularly credit card credit, is off the charts. The average American household carries $15,762 in credit card debt (I recently heard it’s closer to $17,000) and pays $6,658 in interest. “Hey, I could really go for the latest iPhone, but I don’t really have any money saved to purchase it. Oh hello, Mr. Visa Card…you look lonely…let’s take you out for a spin.” If that sounds like you, re-think it. That $300 you spent on your new phone will be much more bloated if you’re carrying balances on your card. As an example, take a look at this chart below. This situation assumes you’re carrying a $2,000 balance and making the minimum payment. At 16% APR, you’ll pay close to $3,000 in interest alone before you pay it back. Have bad credit or miss a payment (causing that APR to jump to 29%)? The interest you pay back more than doubles compared to the 16% APR.

So what can you do? There are a few techniques that you can practice that wade into the realm of budgeting, but specifically with credit cards there are a few things you can try. First, don’t use credit cards and pay with cash instead. Some people feel that returning to the ol’ paper money system instead of using plastic is better for your spending habits. I personally feel that if I have cash in my pocket, I’ll spend it, but I know it works for some. If you’re like me, and plastic is more your style, then retire your credit card and reach for the debit card. The prospect of overdrafting your checking account may stymie spending more than running up your credit limit. Next, examine your credit card bill. It’s amazing the self-reflection that goes on after looking at all those transactions. You may even have recurring billings for things you don’t even use or forgot about. Been there. The idea here is that you can’t fix it if you don’t know about it, so inform yo’self and get to work.

The emergency fund and a healthy consumer debt level are cornerstones of a sound financial plan. The emergency fund provides that much needed buffer for the unexpected events in life and having one in place shields you from acting financially desperate (i.e. using a credit card) in a desperate situation. Consumer debt, aside from the cost of credit, is a behavioral indication that portrays your ability or inability to live within your means. If you are ready to take the steps to begin building your financial plan, start with these two areas and square them away.

Join the YFP Community!

Recent Posts

[pt_view id=”f651872qnv”]

{kind=link}