Continuing the conversation from YFP Episode 002 regarding why every pharmacist should be a millionaire, Tim Baker, CFP, interviews Tim Ulbrich, PharmD to help him determine his nest egg and the monthly savings plan needed to achieve that goal.

Have you ever articulated your “Why” for saving for the future? In this episode, co-hosts Tim Baker, CFP and Tim Ulbrich, PharmD discuss the importance for finding your “Why” for building your wealth and the power of compound interest.

In the very first episode of the YFP Podcast, Tim Baker, CFP discusses his path to the launch of Script Financial and helping pharmacists achieve their financial goals and Tim Ulbrich, PharmD talks about his experience of being broke and working to become debt free.

This post was written by Justin Cole, PharmD, BCPS. He is a 2006 graduate of Ohio Northern University. Dr. Cole recently accepted an appointment as Vice Chair and Assistant Professor of Pharmacy Practice at the Cedarville University School of Pharmacy. Over the previous 10 years, he served in various roles at Nationwide Children’s Hospital in Columbus, Ohio, where he continues to practice. Professionally, he is passionate about pediatrics, pharmacy leadership development, and medical care of underserved populations. You can follow him onTwitterfor content related to these passions. He and his wife, Michelle, have three children and enjoy music, hiking, biking, and just about anything done outdoors. If you have any questions about this article, feel free to contact Justin directly at[email protected].

For most of us, a home is the largest purchase we will make in a lifetime. As a result, our homes are a symbol of status and wealth. We are slaves to comparison, defining ourselves by the number of square feet we occupy or the status of our neighborhood.

Pharmacists may also feel pressure to buy a “bigger and better” home similar to or better than the ones owned by our parents. These factors can lead to taking on mortgages that hinder us from achieving other financial goals. We give ourselves little wiggle room for changes in our financial situation and fail to account for all the costs of home ownership. Mortgage delinquency rates, even though improved today, remind us of this. Five percent of homeowners in the US are at least 30 days behind on their mortgage payment, and more than two percent are at least 90 days late (Ref: Forbes, 2017).

I felt many of these home-buying pressures shortly after graduating from pharmacy school. After having our apartment broken into, my wife and I decided to leave renting behind to buy our first home in a nice, safe neighborhood. We desired to have children in the future, so we looked for homes that we felt would be ideal for a family. During our first showing, we walked into the home and quickly felt it was our “forever home.” We ended up purchasing the beautiful four-bedroom home in a developing area. We knew it was a stretch for us to afford at the time, but we could not imagine passing up the opportunity.

To make it work, we ended up putting 10% down at closing and chose to take a second smaller mortgage at a higher interest rate for the additional 10% of the down payment (which I would never recommend doing). We paid off this second mortgage within a year by trimming costs in other parts of our budget. Over the next few years, we were able to refinance our home and were on track to pay off our mortgage years early. We felt incredibly blessed with our house and our three children that made it a home. We had hosted family gatherings, hosted a small group for our church, developed great relationships with neighbors, and made many fond memories in our home. It seemed that despite some of our financial decisions, things were working out well.

After 10 years in hospital practice as a clinical pharmacist and coordinator, I accepted an academic appointment at a school of pharmacy. With this career change, we decided to relocate and were suddenly in the housing market again. During our search for a new home, we initially went into the process thinking of making a lateral move into a similar-sized home. After all, we were comfortable in our previous home and enjoyed the space it provided. We put offers on two similar-sized homes, but neither worked out. Because homes were selling quickly at the time, we had to rethink our strategy. My wife and I decided to consider homes that were smaller than the one we previously lived in.

In the end, we moved to a wonderful home that was less than half the size and cost of our previous home.

I did not fully realize the impact that home ownership had on our overall financial picture until our move. Through the process, we have learned a lot about ourselves and experienced many unexpected freedoms through downsizing.

Freedom to pay down debt. We were already on a path toward financial freedom, but much of my income was going toward our mortgage payment each month. Moving to a smaller home allowed us to pay off all of our non-mortgage debt including my student loans and an auto loan for a used minivan. Without the move, it would have taken us many more years to achieve debt freedom despite our best planning!

Freedom to save, spend, and give. We desire to be good stewards of all that we are given. Moving to a smaller home allowed us to bolster our emergency fund and gave us the flexibility to save more for retirement. Shortly after moving and paying off our non-mortgage debt, we also decided to take a family vacation that previously seemed like a distant dream. Most importantly, we were in a position to be more generous. While we had always budgeted to give to our church, mission work, and a handful of non-profit organizations we supported, we found ourselves with the ability to meet other needs around us.

Freedom from anxiety. It still pains me to admit this, but I did not realize how much time and energy I spent worrying about our financial situation until after the move. While we weren’t living paycheck to paycheck and had an emergency fund, I still spent a lot of time dissecting our finances, much of which went toward our mortgage payment. After the move, it was as if a burden had been lifted off our shoulders. I found myself thinking a lot less about our financial situation, and my sleep even improved as a result. I had never thought of myself as an anxious person but realized that concerning finances I was. Sometimes it takes a change in circumstances to reveal faults in our own mindset.

Freedom from the desire for more. No one likes empty rooms. The bigger the house, the more you have to buy to fill it. In moving to a smaller home, we began to reevaluate what we really need. We have sold some items, donated others to second-hand stores, given items away, and even trashed things that we had been holding onto for too long. For purchases, we now consider space carefully and evaluate the real need for something shiny and new. In essence, we have learned to live with contentment. We are now more debt-averse than ever before. Our spending habits have changed; we now spend less on possessions and more on experiences that our family can turn into memories.

While living below your means makes complete sense, it took an unexpected change to help us truly realize its blessings. We can confidently assert that freedom comes from making financial independence a higher priority than status symbols. While this may not be the last home we buy, we are content with all of the unexpected blessings that we have through it, and are prepared to make solid financial decisions because of the lessons we have learned.

So what is the way forward for someone who desires to achieve financial freedom and purchase a home? How do you determine what home you need rather than the home you want? Can you have both? Look for more posts this summer related to how home buying fits into your overall financial plan!

The following post was written by Deeb Eid, PharmD. Deeb is a 2016 graduate of The University of Toledo College of Pharmacy and Pharmaceutical Sciences. He recently completed an Executive Residency at the Pharmacy Technician Certification Board (PTCB) in Washington, D.C. and is transitioning to Ferris State College of Pharmacy as Assistant Professor/Experiential Coordinator in July 2017. Dr. Eid’s vision of social and interactive education for all audiences about the profession of pharmacy has led to an ongoing startup development of Facebook, Twitter, and YouTube pages branded as Pharmacy Universe (Feel free to Follow/Like, but still under construction). For any questions, please contact him at [email protected].

Tim Ulbrich (Your Financial Pharmacist) and Deeb Eid have no financial tie to either one of the applications mentioned in this article.

From Your Financial Pharmacist (YFP): There are lots of apps out there that can help you automate your savings goals and invest your money (such as the ones noted below in this article). While automation is a great idea to help you achieve your goals, don’t forget about (1) appropriately balancing investing with your other goals (e.g., debt repayment, saving for an emergency, etc.) and (2) maximizing the use of tax-advantage retirement accounts (e.g., 401k, 403b, Roth IRA).

When smartphones were first introduced, I recall being fascinated with many mobile applications and the usefulness in daily activities. While some were very practical and useful (eBay®, Gmail™), others were simply entertaining and handy for those long car rides (Paper Toss, Temple Run). I found myself excited to learn about applications that made everyday life tasks more efficient. It was even more refreshing to refer friends to certain apps, if it felt like the “right fit” for their scenario. Somewhere along the way came bank accounts, personal finances, budgeting, and many other financial responsibilities that we all deal with each day.

During pharmacy school, I observed that many of my classmates, colleagues, and personal friends loved using their smartphones, but were often unfamiliar with many of the great personal finance mobile applications available. After reflecting, two common areas I’ve identified that we as pharmacy professionals commonly ask about or struggle with include saving and investing. The following mobile applications are both easy to use and provide alternative tools to utilize. They will help to address some of these commonly asked about areas and hopefully make your financial success that much easier!

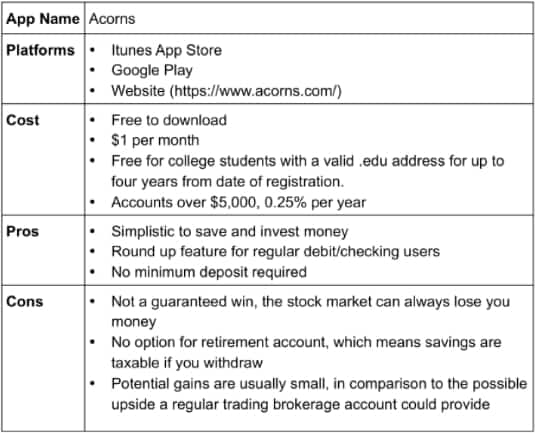

Acorns

Acorns is a seemingly effortless tool to help with saving as well as investing your money. On initial setup, you’ll be asked to connect to a checking account and a series of questions (since you are setting up an investment account, this is the usual). Don’t worry, Acorns encrypts and protects all of your data with bank level security. One of the main concepts within this app is to round up each purchase you make with the linked debit card/checking account. For example, say you go to get a cup of coffee and the total is $3.50. Swipe or pay with debit or the linked checking account and you will get charged $4 to your account, but $0.50 of that that will go into your Acorns account and be saved/invested. Some will find it necessary to turn this feature to “manual” which allows you to only round up those purchases if you choose to within the app.

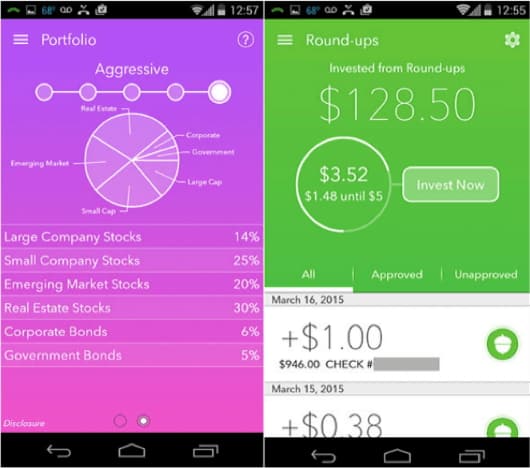

My personal favorite feature is recurring investments. This allows the ability to schedule a daily, weekly, or monthly investment from your checking account into your Acorns account. You would be surprised how quickly saving and investing $10 every Friday could add up! Acorns also simplifies investing. It allows you to pick an approach (1 of 6 available) to your portfolio with how you’d like to invest (from Conservative to Aggressive) (Figure 1). In addition, you can view the projection charts for each portfolio approach to gauge the predictions of how much money you can potentially save/earn based on the amount you put in over a period of time. If you are interested in exactly where your money is invested, Acorns also breaks down the percentages, funds, and sectors in simple and colorful fashion. Overall, Acorns provides a simplistic and easy way to start investing and saving, without all of the complicated financial terminology!

Figure 1

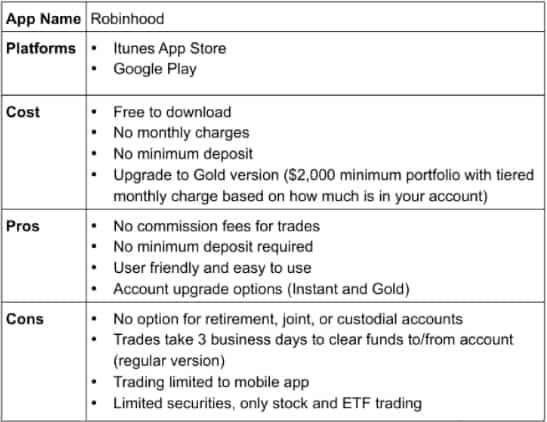

Robinhood

Finally, a stock brokerage that does not charge those pesky commission fees on every trade! For those of you looking to invest your money or who already do and are looking for an alternative broker, this app is worth checking out. Contrary to most other brokers (Schwab, Scottrade, E*Trade..etc.) Robinhood does not require a minimum deposit to get started, but does need your bank account to be linked for transferring money. The interface of the app itself is clean, colorful, and easy to navigate.

Additionally, Robinhood has two upgrade options (Instant and Gold) that have some friendly features for more experienced investors, including the recent addition of margin accounts. The app itself does not feature many of the extras you will find with other brokers (such as in-depth data or news) but serves more as a platform to trade instead.

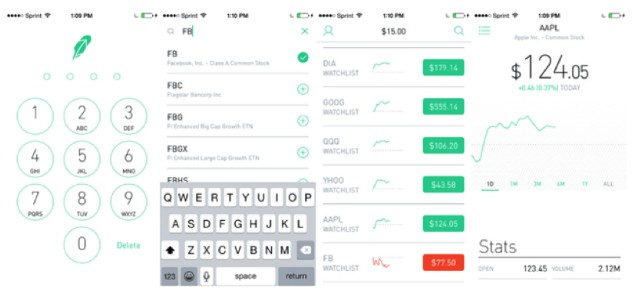

When you click on a specific stock or EFT, you will find some basic statistical information, a trend chart, and a short informational piece on the company (Figure 2). You are not able to transfer funds from another brokerage account into Robinhood, but can transfer them out for a $75 transfer charge. In addition, with the regular account, funds from transfers and trades take around three days to process, which can be limiting. Robinhood Instant has included a feature to eliminate this waiting period, but you might have to be placed on a waiting list to be upgraded.

Figure 2

Overall, Robinhood is a simple way to get started with investing or an option for more experienced investors, looking to for an alternative platform with no commission or account minimum. I’d recommend giving it a shot!

Over the past week, three new graduates reached out to me with $230,000, $240,000 and $300,000 of student loan debt, respectively.

Assuming an average interest rate of 6% and a 10-year repayment plan, the payment due on this type of debt would be $2500 – $3300 per month.

As a point of reference, that monthly payment is more than a mortgage payment on a $500,000 house with 4% interest and a 30-year repayment plan.

All three of these new graduates used words like overwhelmed, drowning, guilty, and confused to describe their situation. I could sense a feeling of anxiety and hopelessness in their communication despite making a six-figure income or being on their way to do so after residency training.

When I heard from these pharmacists, it resonated with my own personal situation where I found myself with $200,000 of non-mortgage debt, making payments of more than $2000 per month and seeing my balance inch downwards in a way that felt like it would never be gone.

So, if you find yourself in mounds of student loan debt, where should you start?

Would it be best to begin with the emergency fund? How about refinancing the loans? What about retirement? Is buying a home going to be possible? If so, when? What about planning a wedding or preparing for the expenses of children?

You get the point. It quickly becomes overwhelming.

For those that are resonating with this feeling of being overwhelmed and in part feeling hopeless, let this post reassure you that (1) you are not alone and (2) being aware of this feeling is the first step in turning the ship around.

The easy thing to do is to get overwhelmed with feeling like you need to do everything at once. I can assure you that the result will more likely than not be spinning your wheels and getting frustrated.

It’s time to do something different.

Your Financial Homework

I want you to make a commitment to get ONE SMALL WIN before the month is over that will help get some momentum moving in the right direction.

Here are some SMALL WIN IDEAS to get you started:

Read one personal finance book;

Put together a budget;

Give yourself direction by setting financial goals;

Save $100 towards an emergency fund;

Send me an e-mail at [email protected] with a question that has been on your mind and is causing you stress;

Buy a term-life insurance policy to make sure your family is protected in the event of your death;

Get rid of a credit card that is plaguing you.

Once you identify and achieve your ONE SMALL WIN, drop a note in the comments section below summarizing what you achieved.

Remember, you are not alone and sharing your ONE SMALL WIN may encourage another pharmacist to do the same.