The following is a guest post from Brandon Dyson, PharmD, Co-founder tl;dr pharmacy

Note: The following is a sample chapter from tl;dr pharmacy’s guide: Mastering the Match. If you are looking to get a residency, Mastering the Match is the best place to start. It walks you through every step of the process; from how to make yourself a competitive candidate to how to nail the interview. In this post, I’ll talk about how (shockingly) expensive it is to get a residency and some ways that you can help lower that cost. If you want to give yourself the best possible chance to win the residency of your dreams, check out Mastering the Match here.

Money Talks: The Price of the Pharmacy Residency Quest

So you’ve decided you want to apply for a PGY1 residency. You, like so many others before you, have felt the rising pressure of holding patients’ lives in your hands and are not quite ready to take the reins all by yourself.

Or you’ve realized during your fourth-year rotations how much pharmacy school ISN’T teaching you, and you’re having an “oh-crap-there’s-so-much-I-have-left-to-learn” moment. I’ve so been there. (Sometimes still there, tbh). Which brings us back to your decision to apply for residency.

While the rest of Mastering the Match will prepare you for the residency process, this chapter is about the math. We’re pharmacists, we like math.

And no, this section is not about numbers in increments of 5s (#shoutouttomyretailphriends!). Nor will it have first-order decay equations a la vancomycin dosing.

WAY more complex then we are about to get into

This is simple arithmetic, but it is so necessary to know ahead of time what you’re getting into financially with the residency application process. Money is all about planning.

So let’s get started.

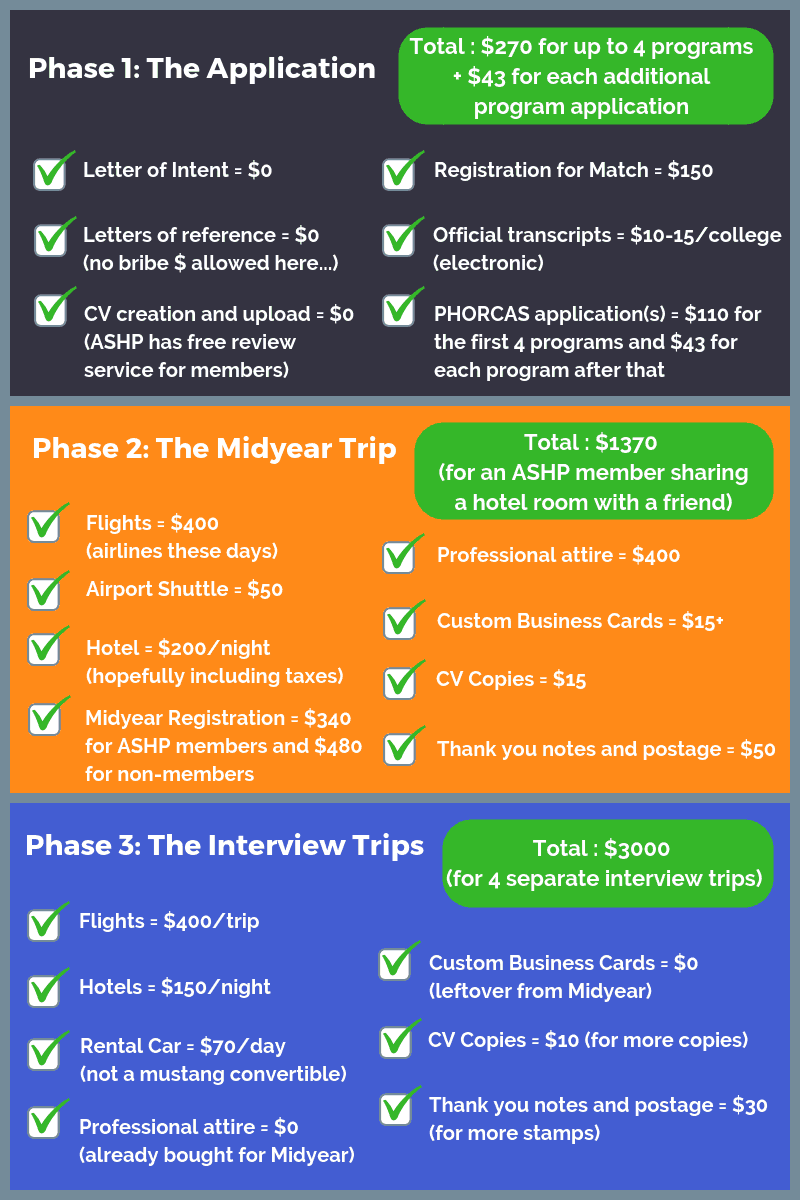

The residency search process can be broken down in 3 major phases:

Phase 1: The application

Phase 2: The Midyear trip

Phase 3: The interview trips

Now let’s take that exact same list and attach estimated costs to each piece to get a rough budget.

Grand Total for Residency Application Process

(with 4 applications and interviews): ~$4600

Phew! That’s a lot of money! Granted, it’s just an estimate, and there are certainly tweaks that can save money. Let’s break this down a little further and talk about where the plusses and minuses might be on this estimate. And we’ll also discuss a few tips to do this in a more thrifty manner.

The Application

There, unfortunately, isn’t much wiggle room to be had here. The only thing I’ll say is to be realistic and thoughtful in your decision to apply to a program. Don’t just apply to 25 programs willy-nilly because you heard so-and-so was going to apply to that many and you feel you have to in order to increase your match chances. That can quickly add up at $43 extra per program application!

This will be you if you apply to 25 pharmacy residency programs

scattered across the country

This is YOUR job search, and if a program isn’t really on the table for you (whether due to interest, distance from home, etc.), it’s ok to NOT apply! That being said, if you have the residency-or-bust attitude and the money to back it up, by all means, go for the gold.

Just remember, all it takes is one program to match. Refer to the many other sections of this guide for more advice on researching programs and the match process.

The Midyear Trip

Travel and Accommodations

There are many ways to save money here! There isn’t much leeway with flights unless you’ve saved up airline points on a travel credit card. You can also book WAY in advance when prices are generally lower.

Where you can really make an impact on your budget is with ground travel and hotel costs.

For ground travel, try to share airport shuttles with other classmates. There will likely be several of you getting into the same airport at similar times, so coordinate ahead of time to book shuttle transportation to and from the airport.

Even if you have to wait 30 min (or more) for other people’s flights to arrive; trust me, you have plenty to do to prepare for the Midyear. So grab a coffee and kill some time in baggage claim. It’s worth it to be able to divide the shuttle cost between up to 8 people for a van instead of just you in a taxi (because, math).

It’s a similar story for the hotel. This may surprise you, but you do not need to stay at the Ritz and drink Dom from fine crystal glasses. You don’t need to buy scotch that’s old enough to legally vote from the hotel bar. Be conservative here. A decent hotel one more block away from the convention center will serve you well.

That being said, I also wouldn’t book too far away from the convention center because you will be going back and forth A LOT. And those cute dress shoes are pretty much awful to walk in. Plus carrying your poster tube and your purse (or your European carry-all for the guys reading this). You don’t want to be a hot mess when you do finally arrive at the showcase.

Another thought on the hotel. Just like with ground transportation, sharing is caring. You don’t have to be besties with a person to share a room for a few days. More than likely, if it’s a classmate, they aren’t a serial killer. So you should be ok to bunk in together for the convention. At least figure 2 to a room so you can each have your own bed. But if you have good friends going and can be comfortable 4 to a room, go for it! (#sleepover!)

Another caveat here…

You do actually have to get some sleep during this convention so you don’t look like the walking dead when you’re telling the RPD why you want their program. So don’t just room with anybody for the sake of saving money. Especially if that somebody is only attending Midyear to hit up Bourbon Street or The Strip. Know what I’m sayin’?

Professional Attire

There are plenty of other places on the internet that can give you much better fashion advice than I can. This section is about how to find something without spending an arm and a leg. You don’t need to be all Armani for this event. Pharmacy residency programs are just looking for conservative, clean-cut, professional attire.

So if that suit happens to be off the rack at TJ Maxx, go for it! If you’re like me and have a hard time finding well-fitted business attire at discount stores, then it’s ok to invest in a nice suit (still doesn’t have to be Armani…a department store works just fine). THEN use the discount store for your dress shirt, business bag, belt, shoes, etc.

If you have a suit already, use this section of the budget to account for dry cleaning. Use a dry cleaner you trust but that isn’t too expensive. You want your suit to come back to you in good shape (viva la suit!). Then, if you’re a careful packer and you hang that suit up in your hotel bathroom right when you get checked in, it shouldn’t be too wrinkly. (And the shower steam can help diffuse minor wrinkles so you don’t have to mess with finicky hotel irons). Online reviews will often point you in the right direction for which dry cleaner does good work for the right price in your area.

Meeting Registration

There’s no getting around the meeting registration. The only tip here is that if you’re not already an ASHP member by the time of registering, it’s worth the $51 for a student membership to go ahead and join. You still come out ahead rather than paying a non-member meeting registration fee ($340 + $51 vs $480 for non-members).

Business Cards and CV Copies

Not every program at Midyear is going to accept these, it’s true. But you’d really hate to have an RPD ask for your CV or contact information, and you don’t have anything to give them. In this case, it’s better to have and not need than to need and not have. Have some copies of both on hand.

Luckily, business cards are cheap to design and print at most big box office stores. There are also online options like www.vistaprint.com. Maybe one of the student chapters of APhA or ASHP at your school is providing business cards through a fundraiser. Just go with the basic package (no glossy finish needed here, peeps), and monochromatic tones will be just dandy.

Don’t go overboard on your student pharmacist business cards…

Same with your CV copies. This is Midyear, your CV is likely going to end up in a box with hundreds of others for reference if needed. Don’t print it on vellum and douse it with the scent of sexy professionalism. It will not make you stand out (at least not in a good way). Just basic white paper copies will be fine. You don’t need to splurge on the thicker stock resume paper. The content of your CV is more important than the material it’s printed on.

Thank You Notes and Postage

There are mixed thoughts about this whole thank you note ordeal with Midyear. Some advise to always send a handwritten thank you note. Others say an email will suffice. In the end, it’s up to you to decide.

But for those of you who choose to walk the path of handwritten, mailed thank you notes for Midyear, you should know something…

The USPS doesn’t mess around. Forever stamps may be good forever, but that doesn’t mean their price stays the same forever. Hot damn, they’re expensive little buggers! So if you’re planning on sending a thank you note to every soul you meet at each program, just know a book of 20 stamps is currently sitting at $10.

Oh and don’t go out and buy Hallmark thank you cards. The dollar store sells some classy, simple multi-packs. It’s ok to send similar-looking cards to people within the same department. Pharmacists won’t be offended by getting the same card – it’s what’s on the inside that really matters! (#awww)

The Interview Trips

Scheduling

While many of the same concepts as the Midyear trip apply here, there are some additional tips to remember. If you have programs in a similar geographic area, see if you can arrange interview dates around the same time. Perhaps you interview with one program on a Friday and another the following Monday. (That’s what we southerners like to call a twofer – two programs for one flight!)

Plus, you’ll have the weekend to check out the area and see if it’s somewhere you’d really like to live for a year. If you’re a Planner Level: Expert, you can even use that time to check out some housing options you’ve researched beforehand.

Travel and Accommodations

Try to use what I’d call the family and friends discount. You know a person you can crash with for a few days? Call ‘em! An extra bonus is the built-in tour guide and transportation for the area.

Oh, but even with all this talk of being frugal, don’t be a total Scrooge – dinner, and drinks on you, of course. They’re saving you a lot of money, you can spend a little of that as thanks. It’s called common courtesy, people.

Professional Attire

Use what you have. There’s absolutely no need to worry about getting a different suit because, gasp, the programs already saw me in this suit with this shirt! This isn’t Fashion Week in NYC, and you’re not interviewing with Tim Gunn. Trust me, programs don’t remember or care (remember, they saw 10,000 other people in suits that day). Unless of course, your suit is purple. (Don’t do it. Just don’t. And I only say that because someone will. Every year. Long story short, please don’t buy or wear a purple suit.)

NOT you at Midyear…

Bonus Tip!

We have to talk about taxes. You know what you’re doing with all of these interview trips, right? Yes, you’re looking for a residency program… but you know what that really is? A JOB! Save ALL of your receipts because, in a rare stroke of governmental goodwill, you can write off job search expenses when you do your taxes! Woot woot #adultwin.

Final Thoughts (tl;dr)

So there you have it, a rough estimate of what costs you can expect from the pharmacy residency search process. Of course, it is just that – an ESTIMATE. There are certainly people who will spend more, but there are also people who will shell out less during the entire cycle.

Remember too, that during this time of interviews, you will also begin the process of applying for licensure in one or more states and registering for the NAPLEX and MPJE. There are (heavy) costs here as well, and you have to factor these in when you’re budgeting for residency interviews.

Generally, licensing costs can be about $1000 for your first state, which includes the NAPLEX ($575), the MPJE law exam ($250 per state, non-MPJE state law exams are similar), state licensure fees (variable, ~$150-300 per state), and background checks (~$50/state).

Additional states can run you ~$500 each (MPJE, state licensure, and background check fees). You can see how graduation is not exactly cheap (there’s also a cap and gown and matriculation fee associated with graduating most pharmacy schools…it’s usually about $100). You either need to be loaded or disciplined with your money to make this work without having the heat turned off in your apartment.

With all of this being said, please Please PLEASE (and I can’t say it enough!) do not let the numbers scare you away from pursuing residency if that is truly what you want to do! It really CAN work (as evidenced by thousands of people every single year)!

There are fantastic residency programs all over this country, and you may not have to go far from your current location to find one that fits what you’re looking for. So your travel budget may be very different than the sample person above who flew all over the country interviewing.

Remember, it just takes one program, and it doesn’t have to be the famous one on the other side of the country. It may be the solid program a 3-hour drive away. Use this as a guide and an awareness tool, and apply it as you see fit.

On episode 76 of the Your Financial Pharmacist podcast, Tim Ulbrich, founder of Your Financial Pharmacist, and Tim Baker, YFP Team Member and owner of Script Financial, wrap up a month-long series focused on investing by fielding questions posed by, YOU, the YFP Communityin this rapid fire investing Q&A edition.

Summary

Tim Ulbrich and Tim Baker tackle several questions during this investing Q&A episode.

Q: Is it better to hold company matched retirement contributions to pay off 20-25% interest credit cards that I had to live off of between residency and my job? A: This may be a situation where you should hold off contributing to retirement and pay off your credit card debt quickly. Tim Baker would suggest to a client to look at strategies for debt reduction while growing income. The additional income can be applied to the debt. This is also dependent on how fast you can get out of credit card debt.

Q: 401k Roth or before tax 401(k) which is the preferred option? The before tax 401k lowers taxable yearly income but we’ll pay taxes on the growth or the Roth 401k is tax free growth over time but higher taxable income at the end of the year. I can’t decide which is the best route. A: There is no one bad way as you’ll either pay tax now or in the future. If you think taxes today will be lower than taxes in the future, go with Roth. If you think taxes will be lower in the future, maybe wait to pay taxes. Tim Baker leans toward the Roth component.

Q: What are your thoughts for proper investing strategies for current pharmacy students? A: Don’t invest anything as a student. Put that money into an emergency fund, toward your credit card situation, or put that additional money toward the accruing interest on your student loans. If you fall in the 10% that graduate without student loans, look at things like an HSA or IRA. Tim Baker offers a student/resident package with a reduced fee to help you establish a foundation and not miss out on wasted opportunities.

Q: Can you go over how to rebalance a portfolio? A: When you set an allocation for your portfolio, over time it is going to drift. When it does, you need to rebalance it. To do so, you sell and reinvest. This usually happens once or twice a year. You can set alerts if an allocation drifts over 5%. Talk to your advisor, company or Tim Baker to do this.

Q: Can you review pros and cons of active and passive funds? A: Active funds believe that the market is not perfectly efficient and that you can achieve above market returns through security selection, market timing or both. Passive investing means that you believe the price of the stock market is efficient and that you are unlikely to outperform the market on a consistent basis. 9/10 actively managed funds underperform passive funds.

Q: Have you guys talked about HSA accounts and risks/benefits and how they fit into a long term financial strategy? A: Yes, in episodes 19 and 73. Follow-up question: Do HSA accounts need to be deposited throughout the year or are these ok to max out contribution limits anytime during the year? A: Like with an IRA or 401(k), it doesn’t matter when you max the contribution out.

Q: How do you feel about investing apps, like Robinhood and Acorns? A: Tim Baker needs to do a review of them as this question comes up a lot. A lot of these solutions believe in low cost investing. Tim Baker likes the concept of building wealth over time and these apps may provide a way to save money without the emotional ties.

Q: Can we do 401(k), IRA and Roth IRA all three? What are the limits in each? Which other options to turn to for tax saving purpose? A: Yes, it depends on the income limits. Tax saving purpose options are HSA or 529 accounts.

Q: What is your thought on robo investors (Betterment etc)? I am a Federal employee, and so my retirement investments go into my TSP. However, I am looking at options for taxable investments beyond what I currently have with an advisor (the fees are making me consider other options). I know that index fund investing with Vanguard or Fidelity offer attractive low fees, but leave me open to issues with taxes on dividends unless I manually do my own tax loss harvesting (which I am reading and learning about, but don’t feel comfortable taking on my own just yet). Betterment does this for me at a higher fee than index investing on my own, but significantly less than an advisor. So, is something like Betterment “good enough” for taxable investments for those that want lower fees but still a more hands off approach? Thank you! I have loved catching up on your podcasts and am, 7 years post graduation, finally getting a better grasp on finances than I ever have. A: Tax harvesting is looking at the gains you make in a year off of your investments. You can sell loser stocks in your portfolio to offset your taxable gains with the goal of breaking even. Betterment or robo advisors can do this automatically and financial advisors also have tools for this. If you do this on your own, you have to do it manually which could take a lot of time.

Q: If I’m a 1099, and have been contributing to a SEP IRA, and decided I want to take advantage of a backdoor Roth, what steps do I need to take to move my money to make it work? A: In a backdoor Roth IRA, you move money from a traditional to Roth IRA. This is a legal way to fund a Roth IRA.

YFP Episode 019: How Do Health Savings Accounts (HSA) Fit Into a Financial Plan?

Episode Transcript

Tim Ulbrich: Hey, what’s up, everybody? Welcome to Episode 076 of the Your Financial Pharmacist podcast. Excited to be here alongside our financial investing expert, Tim Baker, as we’re going to take questions from you, the YFP community in a rapid fire format. So Tim, we’ve got lots of questions on investing. And I think you’re on the hot seat today.

Tim Baker: Yeah, I think I’m ready. I’m ready to go. We have lots of questions, lots of engagement in the Facebook group, so hopefully we can get some of these questions answered.

Tim Ulbrich: Yeah, it’s been a fun month. I think this is a topic that we identified — as we were planning out the month of November, we identified we haven’t done enough on investing. We got that feedback from the community, we heard you, we listened, and hopefully we haven’t overwhelmed on the topic of investing. But knowing it’s such a critical part of the financial plan, we want to give it the attention it deserves. So if you haven’t been with us for the month, make sure to go back and check out the topics we’ve already covered in terms of priority investing, some of the behavioral biases, how to evaluate your investing accounts, DIY versus robo versus an advisor. And here, we’re wrapping everything up with a rapid fire Q&A format. And so for those that submitted questions via the YFP Facebook group, via LinkedIn, via email, thank you. And for those that have a question, make sure to join the YFP Facebook group if you’re not already part of that community. Or shoot us an email at [email protected]. Alright, here we go. Ready?

Tim Baker: Let’s do it.

Tim Ulbrich: Alright, Peter from the YFP Facebook group asks, “Is it better to hold company-matched retirement contributions to pay of 20-25% interest rate credit card that I had to live off between residency and my job?”

Tim Baker: Yeah, this is a great question. And I typically will say an addendum to the certainties in life are death and taxes. I typically will say the part three really should be if you have a match in your retirement plan, the third part is you probably should put that money in and get the max. Free money, you’ve heard us talk about that time and time again. So this might be one of the situations, however, that you might want to pump the brakes. And I think a lot, Tim, it deals with the timeline of things. So if this is something that we can put the retirement contributions on hold and do a gazelle-like sprint, as Dave Ramsey would say, and get through the credit cards, that might be where it would make sense. If we’re talking about a longer term horizon, we’re talking about a debt load of 20-25%, what I would actually do with a client here is possibly look at strategies for debt restructuring so you can get some breathing room. And then my thing is, OK, like how can we grow the top line? How can we grow the income? Not necessarily put the retirement contributions on hold but to apply all that extra income towards kind of the predatory debt levels. So it might be in your case, Peter, that it does make sense and it does make sense to put it on hold for a year or a short time frame and get through it as quickly as possible. But if I’m your advisor, I would say, hey, is there anything that we can do to make additional income so we can kind of keep the match going but also keep aggressive on the loans.

Tim Ulbrich: Yeah, and Peter, I’d point you back too to Episode 026. Tim Baker talked about baby stepping into a financial plan, specifically with a focus on consumer credit card debt and emergency funds. And I think that that would help even answer this question further. We obviously talked about in Episode 068 when we went through the pros and cons of the Ramsey Baby Steps. And via YFP team member Tim Church in the Facebook group saying, “Great question. Thanks for sharing. If you put your match on hold, how fast could you get out of credit card debt?” And so I think that’s the question of at what intensity, as you referenced, would you be able to get this paid off? And then obviously, how do you feel about having that 20-25% debt?

Tim Baker: It’s a great question by Tim Church.

Tim Ulbrich: Alright, Rachel from the YFP Facebook group asked, “401k Roth or before tax 401k?” So referring to a traditional 401k versus a Roth 401k. “The before-tax 401k lowers taxable yearly income but will pay taxes on the growth, where the Roth 401k is tax-free growth over time but higher taxable income at the end of the year. I can’t decide which is the best value.” Now, in Episode 073, Tim Church and I talked about the priority investing. We broke down the differences between traditional 401k, Roth 401k, we talked about IRAs. So I think what we didn’t get into as much in that episode was this whole idea of if I’m weighing between traditional contributions where I’m going to defer the payment of taxes to the future but lower my taxable income versus a Roth contribution where I’m paying taxes now, and I’m going to reap the benefits later. How do you weigh the balance of where to be prioritizing there?

Tim Baker: Yeah, and I think without being too simplistic, again, I think this is one of the things that I think sometimes we look at and we’re like, I don’t know what to do. And it’s almost like paralysis by analysis. And to me, I think it’s the same thing — and I kind of equate it to the avalanche versus snowball. There’s really no one bad way. I mean, you’re going to pay the tax either now or in the future. So you know, again, to back up just so everyone is crystal clear because we had a few questions around this. When you have a 401k, this is typically administered through your employer. Your employer will say, hey, Fidelity, Vanguard, whoever, we want this benefit for our employees as means to recruit and retain, we’re going to set up this 401k and we’re actually going to match. And we’ll say 3%. So it’s basically quarterbacked, in a sense, by the employer. So in this particular investment account, you basically put in a set amount, and everybody — these are 2018 numbers — can put in $18,500. So every year, that’s what you can put in. That’s what you can put in as a maxing out your 401k. Now, concurrently, your employer will incentivize you to put money in by matching a certain percentage. So they might say, hey, if you put in 3%, we’ll put in 3% and match that dollar-for-dollar. And there’s different things. They might say, we’ll match the first 3% and then 50% on the next 2%. So you have to put in 5% to get the full match and essentially, they’re putting in 4%. So I know there are a lot of numbers out there. In the 401k system, you basically have a traditional 401k, so that’s all pre-tax dollars. So it goes in pre-tax, it grows tax-free, and then when you distribute that in retirement, it comes out taxed. So in retirement, you’re going to be taxed on that amount you distribute. What’s becoming more and more popular these days is the Roth component of that. So anytime you see Roth, think after tax. So you’ll actually have what is basically almost like two subaccounts. You’ll have a traditional 401k, which you could put money into. And any match that you get from your employer goes in there. And then you’ll have what looks like a secondary account, which is your Roth 401k. So it’s going to look like two subaccounts, which is all after-tax money. And those monies cannot be co-mingled because you have a pre-tax bucket and an after-tax bucket. So the mechanics of that is it goes in after-tax, meaning you don’t get any tax deduction. So that money actually flows through onto your tax return. It grows tax-free, but in retirement, when you’re looking at a Roth 401k, and there’s $1 million in there, you actually have $1 million that you can distribute. Versus a traditional 401k, if you have $1 million in there, you don’t necessarily have $1 million because Uncle Sam still needs to take his bite of the apple. So those are really the same components. Now, in terms of your ability to contribute to that, it’s an aggregate. So between if you put $10,000 into your traditional 401k, you can only put $8,500 into your Roth 401k. So that’s the 401k. So to kind of go back to the question of which is better, if you think that taxes today will be lower than taxes in the future, probably best to go with the Roth option. If you think that taxes will be lower in the future, it might be worth to defer and wait to pay the taxes in the future. So and again, we’re really trying to look at the crystal ball here. I kind of lean more towards — and I think some of the studies that show, well, if you put money in pre-tax and it grows, that you’re going to pay a higher amount of tax on more money, essentially. And there’s studies that kind of support I think both sides. I think what I’m trying to say here is don’t get caught up in the minutia. I think if anything, I would go more towards the Roth component. But again, like when we talked about in the tax episode with Paul Eikenberg, which was Episode 070.

Tim Ulbrich: Yes.

Tim Baker: 070. There are different strategies out there. So it could be a tax strategy where you are looking to defer or you’re look to avoid. So it just depends, I think. If you have a handle on your tax situation, you’re going to know what makes the most sense for you and kind of your household. So lots of stuff there. I would be remiss to not mention IRAs here, which are similar in a sense that instead of the employer basically quarterbacking it, this is your own Individual Retirement Account that you are — there’s typically no match there. There is no match. But you’re basically putting money into an account and investing it on your own. And we can talk about that a little bit more.

Tim Ulbrich: Tim Baker, preaching and teaching. I love it.

Tim Baker: I’m trying. It’s a lot of stuff. I don’t want to confuse anybody.

Tim Ulbrich: No, it comes up so much. And I think your point’s a good one that we’ve talked with so many new practitioners that are getting that paralysis by analysis. So I think like anything else, take some action, get started, continue to learn, get some help along the way. But don’t do nothing because it seems so confusing.

Tim Baker: Right. And you can always — I mean, it’s the thing like year to year, you can always look at when you’re truly doing financial planning and kind of tax planning strategy, it can change year-to-year. So you might look at your pre-tax money and say, it doesn’t make sense to pay the tax on it today and actually get into some of the nitty gritty. I think for a lot of our listeners, just like how do I get started and what should be the bucket I focus on?

Tim Ulbrich: Yeah, and if you’re somebody who’s not resonating with the audio version of this, and you want to read this and be able to break it down, we spend a lot of time in Chapters 12 and 13 and 14 of “Seven Figure Pharmacist” breaking down investment terms and strategies and retirement accounts and taxable accounts. And so if you need some more time to digest it, look at it, you check that out, sevenfigurepharmacist.com. Alright, we’ve got a question — actually, we got several questions via LinkedIn this time, which was cool. Scott asked, “What are your thoughts for proper investing strategies for current pharmacy students.” So we’ve talked at length about student indebtedness, coming out, and I think when we talk about students, we tend to only focus on debt. So here Scott’s asking, well, what about investing? “I know that if I have time and I can invest and get compound growth, should I get started as a student? If so, what’s the strategy?”

Tim Baker: Yeah, so I typically give the least sexy answer to this question as I can because I get this like when we talk to pharmacy schools. And if it were me, I think the conservative approach to me would say I wouldn’t really invest anything as a student. If I’m a student, any additional income that I have, I’m either kind of going back to Episode 026 where we’re talking about baby stepping into a financial plan where we’re focused on do you have a solid emergency fund? Do you have — what’s your credit card situation looking like? And then from there, I think if I have a solid foundation, any additional money that I had that I want to — I’ve had students ask me about, hey, what do you think about the cannabis industry? What do you think about bitcoin? And I’m like, no, don’t do that. You guys have $160,000 in debt on average. So the least sexy answer is I would apply all of that money back to the interest on your loans that’s accruing. Because what happens is once you get through your P4 year, you pass your boards, you go through your grace period. And around this time of year, you’re going to hit repayment. Any of the interest that you’ve had that you’ve accumulated since the loans originated when you took the loans out — and that’s going to capitalized, which means that it basically moves from the interest side of the ledger to the principal side of the ledger. And now, that interest is accumulating interest on top of interest. So it doesn’t sound sexy, and I get it. Now, if you are one of the 10% of pharmacists out there that doesn’t have student loans, then I would definitely look at things like the HSA, the IRA, and obviously maxing out. And maybe it might be worth spending some time about how I typically advise clients to fill their investment buckets, which would be essentially get your match and your max in your 401k. And the example that I gave, if you have a 3% match, you typically want to put 3% in. And then typically, there you want to go into the IRA world, which is you setting up an IRA at Vanguard or wherever. And you’re putting $5,500 in per year, which is $458.33. So get into that monthly rhythm of putting that money in. And then you typically want to go back into the 401k and max it out, so that’s where you’re getting the $18,500. And then if you exhaust that, then that’s typically where you want to go into the taxable accounts that we’ll talk about here in a little bit. And what I didn’t say is probably along with the max of the IRA, in that second step, if you have a high deductible plan, maxing out the HSA, which is for a single person, $3,450. And for a family, it’s $6,900. So again, if you’re a student, I would focus on all the boring stuff. If you have the debt, if you don’t have debt, then that’s how to start filling your buckets. Now, if you don’t have an employer, obviously, you would want to go right to the IRA and start doing that. But it also depends — to kind of make this answer longer than it should be — is what is your goal? So if the goal of the investment is just to build wealth and put money towards retirement, that’s great. But if you’re investing for purposes like a wedding or something like that that you have a little bit more runway, then maybe you go straight to the taxable account. So lots of stuff, kind of lots of little pieces.

Tim Ulbrich: And I’m glad you brought up the 10% because we don’t talk about the 10%. I mean, if you look at the AACP data in any given year, when they publish the graduating student survey, 10-12% of students report they have no student loan debt.

Tim Baker: Which is a lot.

Tim Ulbrich: Yeah, it’s great. And I think we’re so often preaching to the 88% probably, but I think what just to highlight what you said there is keep your eye on the prize of graduating with as little student loan debt as possible. And I think it can be exciting to jump into investing or it can be exciting to do these other things that are opportunities there, but if you’re contributing some to investments while you’re in school, all while you’re taking on credit card debt or you’re taking on more cost of living, tuition and that’s compounding in interest, obviously, we’re kind of fighting against the effort that we’re doing. So I think this is a good time to talk about what you’re doing with the student resident financial planning services. We haven’t really talked much about that, but if we have students and residents who are listening, saying, I’ve got all these competing things, I’d love to work with Tim Baker talking about financial planning, what are you doing with the student resident package?

Tim Baker: Yeah, so I basically, what I do with students and residents — and I think it to me I think a lot of people are like, oh I don’t have the money or I’m too early in this process. But I think one of the things that I see is especially when it comes to like the foundational stuff, which includes cash flowing, budgeting, student loans, emergency funds, is it could potentially be — and not to speak in hyperbole — it can be hundreds of thousands of dollars swing in terms of your student loans and how we attack them. So what I’m really trying to do is present an offering that focuses on the student and focuses on the resident. So in those years, we can still work at a much reduced speed because I realize that there’s not a whole lot of income. But we’re setting the foundation to the financial plan. So the idea is to work with you guys, that population earlier, and then hopefully feed you into comprehensive financial planning like you and Jess are doing. But I think the swing — I know a lot of planners out there that say, hey, come talk to me after you’re through your residency. And I’m kind of thinking of a counterpart that I have that works with physicians. And my thought is that there’s a lot of wasted opportunity when you don’t have a sound financial plan in place almost immediately. And I think back, Tim, when we went back to USC and we were talking to basically the school, the pharmacy school out there, and we were talking to the P4s. And I was kind of like, I don’t know, probably begging is not the word, but like imploring their P4s, they’re in no better of a situation in that moment to be intentional about their finances.

Tim Ulbrich: Absolutely.

Tim Baker: And really be conscious of and having a plan for their student loans and especially if it’s like a PSLF option if they go into residency. There’s a lot of moving pieces there that I think if you can nail those first few years, that will set you up. So you know, I get fired up about it, and I like working with really all of my clients, but I think the students and residents, there’s so much opportunity there to get in front of.

Tim Ulbrich: Absolutely. So YourFinancialPharmacist.com/financial-planner will give you all the information for those that are interested in learning more. Michael and Audra via the YFP Facebook group are asking about rebalancing. So this idea of rebalancing a portfolio, can you go over how to rebalance, maybe what it means and a step-by-step process. And as you’re working with clients, how often do you do that?

Tim Baker: Yeah, so I think ultimately, when you set an allocation for your portfolio, over time, the investment portfolio’s going to drift. So the example that we can give in very broad terms is Tim, if you come into the office and kind of look at —

Tim Ulbrich: Your new office.

Tim Baker: New office, yeah, in Baltimore. Pretty excited about that. So if you come into the new office in Baltimore and you sit down and say, hey, I really want to save for retirement. I kind of put you through what’s called an investment policy statement. We’re going to build out like what that looks like. A big part of it is going to be the risk assessment. And the risk assessment, it’s going to basically return like an allocation. So it might say, when you answer these questions, you should be 80% in equities, which are stocks, and 20% in fixed income or bonds. So you know, there’s like a general rule of thumb out there — I typically don’t use this — but you could say as a general rule of thumb, just take 100 and then subtract your age, and that’s what you should be in equities. So if you were at 100, and you were 20 years old, you would be in 80%. And I don’t necessarily subscribe to that, but it’s kind of just rough math there. So say, Tim, you need to be 80% in equities and 20% in fixed income. Then you could essentially — and I think we’ve talked about this on the podcast, which a lot of financial planners would maybe argue with me. But I think that you can build a very diverse portfolio just essentially using two funds.

Tim Ulbrich: With low fees. Tim Baker: With low fees. Basically, a total market fund and an aggregate bond fund. So you would buy, if you had $100,000, you would buy $80,000 in a total market fund and $20,000 in an aggregate bond fund. Now, I slice it a little bit thinner. You know, I’ll do more large cap and small cap and international. But I think if we use the example of one fund that’s 80% and one fund that’s 20%, over time, that’s going to drift. So over time, it’s going to be 85%, maybe 90% in that one fund and 10% in the other. So in that moment, your portfolio is more risky than essentially you sign up for. So what you would do is you would say, OK, now the portfolio has grown from $100,000 to $120,000, but I’m exposed too much because I’m in a 90% allocation, so you would essentially say $120,000 by .8, and that’s the target that you would want your total market, that equity to be in. So you would essentially sell off some and basically reinvest it into the bond to rebalance. Now, you typically want to do this once or twice per year because really, it just saves on costs. So typically, I have alerts on my investment accounts that basically alert me to trade. In most of the retirement plans, you can actually set these up. So if it drifts over 5%, then it will rebalance for you.

Tim Ulbrich: Yeah.

Tim Baker: So if you don’t know how to do that, obviously I would say to talk to someone at that, whether it’s Fidelity or whatever, talk to this, they can help you or reach out to me or another advisor that can help you with that.

Tim Ulbrich: So this might go into the behavioral biases, but I’ve found that I like having somebody else rebalance. Not because I think it’s difficult to do, per say, but what I found myself doing is I would go into my accounts, and I’d start sticking my fingers in it. And then I’d start saying, ooh, international, 10%. I keep reading the news, what’s happening with international stocks, and you start inserting all these biases. And I start adjusting and shifting things. Where if you and I agreed on an investment policy and strategy and we’re not reacting to the world of today but we’re looking at the long-term play, I’m less likely to do that, right? Or I’m going to at least engage with you before I make those decisions or whomever. So I think it just speaks to — and this gets to the next question about active versus passive funds, which I’m going to pose to you. But it speaks to that strategy of not necessarily leave it and forget it, but once you develop a strategy and a mindset, we’re in this for the long-term play. We’re not in it for the news of what’s happened in the DOW this week, right?

Tim Baker: Right.

Tim Ulbrich: So let’s talk about active and passive. So another question via the Facebook group, “Can you review the pros and cons of active funds versus passive funds?” I think we have some biases here probably. We’ve talked about those before. But what are the main differences and what should people be looking for?

Tim Baker: So an active investor basically believes, they believe that the market is not perfectly efficient. So if I’m an active investor, I basically think that I can achieve above-market returns through essentially security selection, market timing or both. So I’m smarter than the average bear that if I’m looking at large cap stocks, I’m going to be able to pick that better than what the market can essentially do. And then in terms of market timing, I can essentially see the future in a lot of ways. So the condition is I must determine when and under what conditions to both buy and sell. So the two methods that really people use to do active investing is technical analysis, which is really an attempt to determine kind of the demand side of the supply-demand equation of a particular security. So this typically relies on timing; it’s a lot of charts. You study past pricing, sales volumes, future trends. And you’re not necessarily concerned about hey, what’s Ford’s next line of cars? Or what’s the leadership at this company? It’s really about patterns. So that’s one way to look at it. The other way is the fundamental analysis where you’re looking at both kind of that macro and micro data. So you’re looking at interest rate increases, monetary policy, but then also specific to that industry or that company, productivity and profitability and earning potential. So that’s the active investor. The passive investor says, thanks but no thanks. I believe that the price of the stock market is essentially efficient, and then when I read that story in the New York Times about the cannabis industry or whatever or bitcoin, it’s been priced into the market long, long ago. So I’m not getting a stock tip or anything like that, I’m basically — I know that that is perfectly efficient. So the passive investor basically says, you’re unlikely to outperform the market on a consistent basis. And generally, that well-diversified portfolio that I just explained that has low cost is the better way to go, that you’re not going to — in the long-term — outperform the market. And the stats show that about nine in 10 actively managed funds underperform the passive funds. So inverse is true is typically, actively managed funds are more expensive. And that’s one thing that a lot of investors aren’t really aware of is what is it, how much money is actually going to be evaporating from their accounts because of expense ratio? And typically, the more you pay for the investment, the worse it is for the investor. So you would think if I’m buying a luxury car and paying more, I get better quality. So I would expect that. It’s not true with investments. Typically, the cheaper ones are the better way to go.

Tim Ulbrich: So for those interested in learning more on this topic, a few that come to mind, resources and books. We talk about obviously in “Seven Figure” as well, but “Simple Wealth, Inevitable Wealth” by Nick Murray is a great read. “Laws of Wealth” by Daniel Crosby is fantastic. And then “Index Revolution.”

Tim Baker: “Index Revolution” is such a simple —

Tim Ulbrich: Charles Ellis, is that who wrote that?

Tim Baker: Charles Ellis.

Tim Ulbrich: Yeah.

Tim Baker: Yeah.

Tim Ulbrich: OK. So we’ll link to those in the show notes. But I think a great topic, and obviously when this topic comes up, probably the most famous quote on this is Warren Buffet, who is the active investor of all active investors, you know, really quoting that as he thinks about the future for his family, his spouse, in terms of advice, obviously what he had to say was probably most people are best off putting it in an index fund and letting it ride.

Tim Baker: Yeah, and he’s one of the people that on Planet Earth — and there’s probably, you know, a very small, like maybe half dozen that can kind of see what’s going on with the markets — part of it, and I think these guys admit it because they have access to investments. Like they just buy companies.

Tim Ulbrich: A little more purchasing power than we have.

Tim Baker: Right. So by and large — and I think that’s one, if you’re talking to people and really advisors who say, hey, I can beat the market, go the other way because nine times out of 10, even moreso than that, we have no idea where the market’s going to go. It’s better set an allocation, keep expenses low and kind of the singles and doubles approach.

Tim Ulbrich: Awesome. So Ryan asks via LinkedIn, “Have you guys thought about HSA accounts? Risks and benefits and how they fit into a long-term strategy?” We did in Episode 019, we broke down, you and I, HSA accounts and then also again in Episode 073, Tim Church and I talked at great length about the prioritization of the HSA, what are the contribution amounts, what’s a high deductible health plan. So for those that are itching, especially around — well, we’re post-enrollment now — but around that time, it’s a good time to be talking HSAs. But we had a follow-up question from Brynn on HSAs. “Do HSA accounts need to be deposited to throughout the year? Or are those OK to max out the contribution limits anytime during the year?”

Tim Baker: Yeah, I don’t think it really matters. I think it’s the same thing with like an IRA. Like some people will say, hey, I want to max out $5,500 immediately. Same thing with the 401k. I guess technically, you could front-load $18,500 in the first quarter of the year. With the HSA, if you $6,900 to put into it and you know that you’re going to have family medical expenses, I would have it really act as a pass-through if that’s the purpose of the account is to fund that and then use it if you are using it for medical expenses. Now I think what we’re trying to do in my household is more of using that as a self-IRA and really cash-flowing the health expenses and let the HSA go. So again, I think that’s a little bit of next-level in terms of having that bucket of money for that purpose. But yeah, HSA is a powerful — and I think one of the really good things about the HSA is that you could make $1 million and still get a deduction for that, which with the deductible IRA, most pharmacists, unless you’re a resident, you’re going to make too much to be able to enjoy the deduction.

Tim Ulbrich: Joseph via LinkedIn asked, “How do you feel about investing apps like Robinhood and Acorn?”

Tim Baker: Yeah, you know, we get this question so much that I really — I probably need to sit down and actually review all of these different solutions and come up with kind of an opinion on them. So I know a lot of advisors — and you kind of see this in the pharmacy world too, it’s like as technology creeps in, there’s almost like a defensive pushback like oh, I’ll never be replaced by a robot. I’m more of the mindset to embrace the technology and utilize it for good. So I think some of these ideas with rounding off purchases and slowly building wealth over time, I actually like that concept. Because from a behavioral perspective, we’re more likely to save that way than if Tim, if I was a financial planner and I said, “Alright, Tim, can we put $100 more per month into your IRA?” If you’re less of a feel, less of an emotional pull, I’m all in. So I think to Joseph, I think I owe you and a lot of the other people that asked me that question to kind of do a deep dive and look at these and see. I do know that a lot of these solutions believe in kind of low-cost investing. They’re not necessarily putting you in expensive funds. But I think an extensive look is probably something that we should have on the docket for 2019.

Tim Ulbrich: Alright. Via the Facebook group, Krishna asks, “Can we do 401k, IRA and Roth IRA all three? What are the limits in each? Which other options to turn to for tax savings purpose?” So again, in Episode 073, Tim Church talked a lot about the total contribution limits, you broke that down, preaching a little bit earlier, so we covered that. But the question of all three, the answer is yes with an asterisk, right? Depending on some of the taxable, the income limits and what not that we’ve talked about. What other options besides those do you turn to for tax-saving purposes? So if somebody’s listening that’s saying, “OK. I’ve got me covered in a 401k, got me covered in a Roth IRA. I’m looking to do more.” HSA…

Tim Baker: HSA would be the big one. Yeah, absolutely. And I think if the HSA is not on the table — and that typically is where you look at the taxable account, which you don’t necessarily get a tax benefit unless you’re doing some tax (inaudible), which we’ll maybe talk about here and that type of thing. But yeah, those are the major books that you want to focus on and really exhaust before you get into some of the other vehicles. And I think that’s one of maybe the drawbacks for like Robinhood and Acorns is I’m not sure if they’re necessarily IRAs or they’re taxable accounts. And typically, I feel more comfortable, unless it’s more of a near-term goal like a wedding or a trip or something like that, I would want clients to focus more on the retirement buckets before they would go into the taxable buckets.

Tim Ulbrich: Yeah, and obviously if kids are in the picture, taking advantage of 529s and the tax advantages over there as well. So Cory via email asks, “What’s your thought on robo-investors, specifically Betterment?” Now obviously in 075, we talked about DIY v. Robo and Hire a Planner, so if you haven’t yet heard that, go check it out so you get some more background on robos. He says, “I’m a federal employee, and so my retirement investments go into a TSP,” which we talked about in Episode 073. “However, I’m looking at options for taxable investments beyond what I currently have with an advisor. The fees are making me consider other options. I know that index fund investing with Vanguard or Fidelity offer attractive low fees but leave me open to issues with taxes on dividends unless I manually do my own tax loss harvesting, which I am reading and learning about but don’t feel comfortable taking on my own. Betterment does this for me at a higher fee that index investing on my own but significantly less than advisors. So is something like Betterment good enough for taxable investments for those that want lower fees but still a more hands-off approach? Thank you, I love catching up on your podcast. I’m seven years post-graduation, finally getting a better grasp on finances than I’ve ever had.”

Tim Baker: That makes me feel good.

Tim Ulbrich: Yeah. So Cory, thanks for the thoughtful question, appreciate the feedback. And I think these are the ones that get us fired up.

Tim Baker: Oh yeah.

Tim Ulbrich: So before going into the question maybe about pros and cons of a robo and building off what we talked about in 075, break this down on tax loss harvesting quick. I think this is kind of a next-level question from what we’ve talked about before.

Tim Baker: Yeah, essentially so when we depart from all of the retirement accounts, 401k’s, IRAs, in those accounts, your investments essentially grow tax-free. So the government basically leaves you alone from a tax perspective and any gains you might get inside of those accounts. On the taxable account, which is basically a brokerage or just an investment account that you have that is funded with after-tax dollars, it doesn’t grow tax free. And when you realize gains, you actually pay taxes on it. So what tax loss harvesting is is essentially you’re looking at any gains that you make throughout the year. So if I buy Tesla stock at x and then I sell it at x plus a 20% profit, I’m going to pay capital gains on that amount of money. What tax loss harvesting done is basically it looks at some of the less profitable, even loser stocks and positions in your portfolio, and you can actually sell those to offset your taxable gains. So you’re essentially trying to break even, in a sense, from a tax perspective. So this is a strategy that robo investors like Betterment can do automatically, and sometimes they do. And even a lot of financial advisors have tools that can do these things similarly. If you’re on your own, though, with a lot of these tools, you essentially have to do it manually. So at the end of the year, you might say, hey, I have a gain, so I don’t want to pay this amount of tax on it. So where can I sell an investment at a loss to offset those gains. And typically, you can basically offset whatever your gains are, and you can actually lower your income by about $3,000 per year, your ordinary income, if you have enough of a loss. So it’s kind of next-level. Betterment, I think boasts that you could potentially save .7-2.5%. Like that’s the range that you can ultimately do. I think those are a little bit exaggerated. To go back to the question, I think it’s really a matter of you get what you pay for, in a sense. Obviously if you’re doing low-cost investing on your own, obviously you have to do a lot of the legwork.

Tim Ulbrich: Yeah.

Tim Baker: Tim, you kind of talked about with your DIY approach when you were buying and selling houses, or selling house. It’s a time-suck. The Betterment approach is maybe that where they can do it automatically, but you’re going to pay 50 basis points on that. So you pay for that. And then an advisor could be where they’re charging you a fee and maybe an AUM fee. But you get a little bit more of the human element. So it kind of depends on, I mean, if I’m Cory, if this is something that you want to DIY, and your taxable account is not huge at this point — I’m not sure where you’re at — maybe you try to figure out the tax loss harvesting for yourself and take a crack at it. But you might get to a point where you have a million other things to do with life and you just would rather just slot it into a Betterment. But yeah, it’s definitely a strategy that I think if you can do consistently over time, you can essentially protect some of your gains because we talk about taxes and inflation are the big headwinds that are blowing in your face as you’re trying to build wealth over time.

Tim Ulbrich: Yeah, and I think this builds nicely off of what we talked about in 075 and really, have been talking about since Day 1 is emphasizing the point, which is important here when we’re doing a whole month on investing, that investing is one part of a very comprehensive financial plan, right? So if you’re doing the DIY robo route, making sure that you’ve got those other pieces accounted for and you’re not looking in one avenue, in a silo, only one bucket, and you’re really looking at the entire financial plan and picture as you’re moving forward. Alright, last question comes from Mo in L.A. via email. She asks, “If I’m a 1099 employee, and I’ve been contributing to a SEP IRA and decided I want to take advantage of a back-door Roth, what steps would I need to take to move my money to make it work?” I think that while Mo is asking this question of being a 1099 and a SEP IRA, which we talked about in 073, maybe to broaden this out to the community at large is the mechanics of a back-door Roth IRA. Now, we’ve defined what it is. But for those that say, OK, I don’t meet the income limits for a Roth IRA, so I know I need to do a back-door Roth, what is the next step they take?

Tim Baker: So typically, the breakdown is like anybody can contribute to a traditional IRA, but not everyone necessarily gets the deduction. For a Roth IRA, not everyone can actually contribute to a Roth IRA. So once you make a certain amount of money, those doors close to the Roth IRA. So typically, what the mechanics of is you can actually contribute to a traditional IRA and then essentially recategorize or do a back-door Roth IRA. So you basically move the money from the traditional to the Roth in an instant. And it’s a legal way to basically fund the Roth IRA. So that’s really the mechanics of it. Now, a SEP IRA, which we’ve outlined in previous episodes, is really the IRA for that Self-Employed Person. So for someone like me who I don’t have a TSP, I don’t have a 401k, I basically am — and really the traditional and the Roth IRA are not enough for me to be saving for retirement. So you can only put $5,500 per year in that. The SEP IRA is basically an investment account for the self-employed where you can put a lot more money in. It’s like $55,000 per year into that versus the $5,500 that you can put into the Roth and the traditional IRA.

Tim Ulbrich: So good question. We took a lot this week, and here we are, finally, end of November. We’ve hashed out investing. I think this is a series we’re going to really look back at and say, for those that want to dig in deeper into investing, go back to November 2018 where we covered a lot on this topic. So we’re pumped as a team to be wrapping up 2018. We’ve got lots of exciting content, new content, new ideas, things are coming to 2019. So we hope that you’ll continue on the journey with us. We hope that you’ll join us in the YFP Facebook group. And before we wrap up today’s episode, I want to again take a moment to thank our sponsor, PolicyGenius.

Sponsor: While paying off debt, buying a home and saving for retirement can be MUCH more exciting than ensuring the proper insurance coverage is in place, having the right coverage — not too much and not too little — is essential. And for pharmacists, our greatest tool to achieving our financial goals is our income. And that’s where disability insurance comes in. It protects your lost income if you’re sidelined by an illness or injury. And PolicyGenius is the easy way to get it done. They compare quotes from the top disability insurance companies to find you the best price. So if you rely on your income to get by, compare disability insurance quotes by visiting PolicyGenius.com. PolicyGenius will help you protect your paycheck at a price that makes sense. You can get started online right now. PolicyGenius. The easy way to compare and buy disability insurance.

Tim Ulbrich: And one last thing if you could do us a favor. If you like what you heard on this week’s episode, please make sure to subscribe in iTunes or wherever you listen to your podcasts. Also, make sure to head on over to YourFinancialPharmacist.com, where you’ll find a wide array of resources designed specifically for you, the pharmacy professional, to help you on the path towards achieving financial freedom. Have a great rest of your week.

On episode 75 of the Your Financial Pharmacist podcast, Tim Ulbrich, found of YFP, and Tim Baker, YFP team member and owner of Script Financial, continue YFP’s month-long series on investing by talking about the pros and cons of a DIY approach to investing compared to utilizing a robo advisor or hiring a financial planner.

Summary

On this episode, Tim Ulbrich and Tim Baker dive into a discussion of three strategies of investing: DIY, robo and hiring a financial planner. The DIY (do it yourself) route of investing means that you, instead of your employer or planner, will be in charge of all aspects of your retirement or investment. You’ll determine how much to defer into retirement accounts, what to invest in, make adjustments, and figure out to how to distribute funds at retirement, among other tasks. This route is becoming more popular most likely due to the fact that there are resources available and many advisors require their clients to have a lot of money to work with them. Pros of the DIY strategy are that there is a potential savings (if you are doing it well, etc.) and a feeling of empowerment. Cons are that there is a lack of accountability, that someone isn’t there checking or bringing awareness to potential financial behavioral biases you may have, and if you aren’t well-versed in the information, you could end up paying more.

Using an advisor is a strategy that lies between the DIY and financial planner routes. With this strategy, technology is used which allows you to simply click a link, answer a few questions, and fund taxable accounts. The pros of this strategy are that you don’t have to go through thousands of funds, the funds are automatically rebalanced over time, and the cost lands between .25-.5% on what’s invested. Cons are that there is no human interaction and that this only focuses on one part of your financial plan.

Hiring a planner means working with someone to act as the middle point between you and your investments. Pros to this strategy are the human aspect, the potential of having a comprehensive financial plan, the ability to create a diversified portfolio, and having someone act as a safeguard between you and your investments. Cons of hiring a financial planner are that the industry is structured so many planners are incentivized to grow your assets, may have a conflict of interest due to making more money off of your investments, and that a planner may not help you with credit card or student loan debt.

Tim Ulbrich: Hey, what’s up, everybody? Welcome to Episode 075, excited to be here alongside Tim Baker as we continue our month-long series on investing. We’re nearing the end. We’ve got next week coming up, we’re going to do an investing Q&A. But first and foremost, happy Thanksgiving, Tim Baker, to you and to the YFP community. So excited to be here.

Tim Baker: Yeah, happy Thanksgiving, Tim, to you and yours. And excited to get this episode going.

Tim Ulbrich: Yeah, we hope everyone’s having a great day, enjoying with family. We hope that you’re not nerding out on personal finance podcasts while you should be spending quality time with family. But if you are listening, please know that we appreciate it and that we’re certainly grateful for the community that has developed here over the past year. So we’ve been going along this month on investing. We’ve covered a lot of different topics and information, everything from behavioral aspects to investing, prioritization of investing, what to look for in your different investment accounts, the fees and so forth. And next week, we’re going to wrap it up with an investing Q&A. But here, we’re talking about the strategy of investing. Is this something you do yourself? Is this something you look at engaging with a robo advisor? We’ll talk about what that means. Or is this something you look at hiring a financial planner? Maybe for many people listening, there may be a different answer depending on the status of what you’re working on and what your preference is. So we’re going to reference some previous episodes throughout this episode, so let me throw them out here in advance. Episodes 015, 016 and 017, we talked at length, Tim Baker and I did, about what to look for in a financial planner, the benefits, different types of planners that are out there. In 054, we talked about why fee-only financial planning matters. And in 055, we talked about why you should care about how a financial planner charges. All of that feeds into the conversation here about DIY, robo or hiring a financial planner. So in terms of the structure and format of what we’re going to do, with each of these three buckets, we’re going to talk about what we’re referring to in a DIY approach, in a robo approach, in a financial planner approach. We’ll talk about the pros and potential pitfalls of each of those approaches. So Tim Baker, DIY. When we say DIY as it relates to investing, what exactly are we talking about? Whether listeners are thinking about maybe their 401k or maybe their 403b at their work environment, in the TSP, or they’re thinking about an IRA that’s outside of their work?

Tim Baker: Yeah, so the DIY, the Do It Yourself approach when it comes to investing, when we’re discussing things like the 401k, the 403b, the TSP, this is a little bit set up on a T-ball stand for you because the employer is essentially putting it in front of you and saying, hey, now that you work for us, we have contracted through an organization like a Vanguard or a Fidelity to basically have this investment account for you. So we’re going to cut you a deal, as long as you put money into it, we’ll match it. And we’re going to help you grow your retirement. So you can DIY that. And essentially, it’s a sandbox approach because you’re going to put in front of you a series of 10, 15, 20 — depending on the plan — investments that say, hey, for large cap, for U.S. large cap, you’re going to have four or five funds to pick from. From international, you might have two or three funds to pick from. From a bond, you might have some, it could be target funds. And if you’re hearing me talk about this and you’re saying, ‘What the heck is this guy talking about?’ then maybe having some help and not DIY-ing that — won’t be for you. Because the plan is defined, you’ll have basically a sandbox to work in. And essentially, what you’ll do is you’ll determine how much to defer into your retirement accounts. We’re talking your 401k, your Roth 401k, your 403b, what to actually invest it in — so a lot of people sometimes, they miss that step. So they think that once they put the money in there, it’s automatically invested. And some plans will be like that. But some plans won’t.

Tim Ulbrich: And they find out it’s just sitting there in a market fund.

Tim Baker: Right. I’ve seen that happen quite a bit. So you basically figure out how much you want to defer, what you’re going to invest it in, and over time, you have to kind of make those adjustments and do the rebalancing and things like that. And then when you go to retire, then you basically say, ‘Self, how do I distribute this in the most tax-efficient manner as possible?’ Whereas Tim, I don’t know about your dad, but my dad — well, my parents, really, they worked for the same company for 40 years, and the companies did that for them. And the pension manager would do that for them, basically would manage all those steps. So now, it’s kind of on us to figure that out. So that’s kind of the retirement side. If we’re talking outside the retirement, and we’re looking at IRAs, Individual Retirement Accounts, could be 529s, could be taxable accounts, that’s really where we’re going out into the market, essentially, and we’re looking at TD America, Vanguard, Fidelity, we’re going onto their website because we’ve heard of these companies, and we’re saying, ‘I want to open up an account on my own and basically do some investing on my own.’ So this is where you would open up a taxable account, open up a Roth IRA, and then the process is very similar except it’s just outside of the realm of what your employer is. So you’re opening up that account, you’re funding money from your paycheck. In then in that world, you’re essentially looking at a vast ocean, thousands and thousands of stocks and bonds and mutual funds and exchange traded funds, all the different things that could fit in these accounts. And you’re doing it in a way that hopefully is consistent with your beliefs about investing, if you have any, your risk tolerance, how you want to maximize or minimize, really, expenses and that type of thing. So I can tell from personal experience just the first time I ever opened up a Roth, I was at West Point. And I wanted to just dip my toe in the market. And I wanted to feel the feeling of basically buying a stock in a company.

Tim Ulbrich: Been there.

Tim Baker: And I think I bought like one share of Johnson & Johnson, and like after the transaction grew — and it’s kind of not very exciting — it was kind of exciting to see it, but I bought one share, which is the most inefficient way to do it because one share at that time was probably like $45. But then I paid like $10 —

Tim Ulbrich: The fee, yeah.

Tim Baker: Just to do the trade-in. But it was cool because at that time, I was like, well, technically, I’m part owner of this company, a .0 — add so many zeroes — 1% of Johnson & Johnson, so I would get documents that say, ‘Hey, these are when the board meetings are,’ but I really didn’t know what I was doing. And quite frankly — I know, Tim, we talked about this before — I probably had no business doing that, opening up an account like that because I didn’t really have a proper emergency fund. In the Army, a student is a little bit different, but there were so many other things that foundationally, I should have done before I even got to that point, but that’s kind of in a nutshell what the DIY approach is.

Tim Ulbrich: Yeah, and I think it’s — for many of our listeners, they’re probably thinking about, OK, most of my investing — maybe not all — but most of my investing’s happening with my employer-sponsored plan, so 401k, 403b. Of course that’s not everyone listening, many people have Roth IRAs or have taxable accounts that are out there, but what I’ve seen, Tim, is depending on the employer, how complex that is or is not can be all over the place. So for example, I work for the state. And they intentionally simplify options, you know, you’ve got two options in large cap, two options in international, they’re all index funds. Fees are pretty low. And I think they’re really trying to minimize some of the behavioral components that are there. But it’s still up to me, if I were doing a DIY approach and saying, OK, this is my asset allocation, this much stock, this much bonds, this much cash or cash equivalent or REETs or whatever. And then within there, what types of stocks I want to be investing in and then am I going to rebalance or not. Now, for other people — like a target fund I’m thinking of specifically — if somebody were to choose a target fund to say, OK, I’m going to retired in the year 2075, and that’s going to then set my asset allocation. The rebalancing is kind of happening along the way.

Tim Baker: It’s automatic.

Tim Ulbrich: Yeah.

Tim Baker: I would say from a target fund perspective, if you literally listen to what I just said about different types of funds like bond and international, emerging markets, small cap, large cap, and you’re like, ‘I have no idea,’ then go target fund. You probably will pay some type of premium for that service of it being rebalanced and becoming basically more aggressive to more conservative over time. But more often than not, I would rather you just pay the premium than have it sit in cash or be way too aggressive than you need be, depending on where you’re at in your life. But oftentimes, when I work with clients — and this is the opposite end of the spectrum, which is not DIY, it’s working with an advisor — I crack that nut, and I say, “Hey, client, you have 15-20 different options out there. And you’re in a target fund right now by default. I think we can do a little bit better given your situation and save on expense and things and break it out that way.” I think one of the things that you talk about (inaudible) and I’ve read a few books about the more choice that we are given, the more it causes that paralysis by analysis. And they say even like things like auto-enrolls. So we’ve talked about auto-enroll. There’s a lot of people that before auto-enroll really became a thing would work for a company for five, six, seven years, a decade, and never opt into their benefit of a 401k and the match there. Now, and this could be something the Obama administration put in, is that they’re incentivizing companies to basically auto-enroll employees. And then you essentially opt out of it if you want. And they’ve done a lot of studies in this with like Sweden and Finland, you have to opt out to not be an organ donor. And two countries that are very similar in a lot of ways, the opt-in, the percentage of people that were actually donating their organs was very low versus the opt-out. So a lot of this plays in. And we could do a whole topic, a whole episode, on behavioral finance and all the different biases that are out there. And I think that’s one of the things that maybe working with an advisor does. But it can be really confusing when you do it on DIY. It’s not impossible, obviously. But I think ultimately, my opinion — again, I’m biased because I do this for a living — is that I think it’s always good to have an objective look at your finances and say, hey, does this make sense? Is what I’m doing OK because I heard Uncle Tommy say this or my neighbor down the street said that, and I really want to know like sanity check this.

Tim Ulbrich: So obviously, as we think about the DIY approach, I think it’s fair to say that it’s becoming more popular — maybe not more popular but why is it popular in some regards. Accessing information is more readily available than it’s ever been before.

Tim Baker: Right.

Tim Ulbrich: Resources are out there. Just today, we had somebody ask in the YFP Facebook group, you know, I’ve heard of back door Roth IRAs, but what do I actually do mechanically. And we were able to quickly reference an article, get her a stepwise approach. So that information is there, readily available. I think that’s one of the reasons that it’s quite popular. What else do you think in terms of why people are going kind of that route of more of a DIY?

Tim Baker: I think it’s a little bit of an indictment of kind of my professional brethren. You know, there’s a lot of advisors out there that will say, “Hey, love to help you. But you have to have a half a million dollars before I can actually do work with you.” And the reason they do that is because they’ll charge based on assets, investable assets, which basically mean the assets they control directly, not what’s in your retirement account. So they say, “Hey, love to help you, but I can’t because I won’t essentially be paid enough.” So you have those minimum assets under management, AUM, requirements that basically for a lot of young population, just excludes them in general. I think one of the things that — and I was a little naive, no, I was a lot of naive to that is when I was looking at the profession of personal finance, kind of the whole 1% Occupy Wall Street was going on. So I think there is a distrust of large banking institutions and really financial advisors in general. And I think in a lot of ways, it’s well deserved. What a lot of people don’t know is that the majority, the overwhelming majority of financial advisors can legally put their own interests ahead of their clients, which when I kind of figured that out — and I was in that model when I discovered that the fee-based where you can earn commission fees, that blew me away. And it shouldn’t be that way. And I’m not saying that means 95% of the professionals out there are corrupted. But to me, is it should always be about the client, always be about what is in the best interests of the client, not necessarily mine. So I think that that perception is prevailing in a lot of ways. And that’s why I’m kind of fortunate when you talk about the work that we’re doing with you and Jess, it legitimizes, I think, what I’m trying to do. And I think what the fee-only world is trying to do is really say, there are services for young people that you’re not excluded. And by the way, I want to be on your team. And I want to get you to those goals that we talked about that whether it’s orca whales (?) or being able to retire at a certain time or whatever that is, that stuff jacks me up. And really, it’s the mechanisms of what the investments are and are properly insured that are just that supporting detail that I more or less have a playbook in my mind, and we just kind of plug and play depending on your situation.

Tim Ulbrich: Yeah, and I think I can say as somebody who went the DIY route for 10 years, you know, after graduation and obviously in working with you and Jess and I, I think too it’s fair to say for many listening, there’s just that overwhelming transition that happens where you’ve got new career, you’ve got tons of student loan debt, you feel like you’re trying to develop budgets and take care of all these other things. And part of it I think is just that feeling of being overwhelmed and my budget’s tight, I’m trying to figure out these things, and I may see additional fees or things and not necessarily be able to articulate the benefits associated with those.

Tim Baker: Right.