I’m going to get straight to the point with this post. I don’t want this important and potentially game changing message to get lost in any fluff. So, here it is.

You could be making a $1 Million (or maybe even more) mistake and aren’t even aware it is happening.

What?! There aren’t many things you read that can result in you making a small change for some BIG wins…this is one of those.

Whether you are saving for the future in a 401(k), Roth IRA or some other investment vehicle, I’m guessing that with the exception of some financial nerds reading this post, you don’t have a good idea of the ONE THING that is having a significant long term impact on your wealth building success….the fees associated with those investments.

In Tony Robbins’s books Money Master the Game and Unshakeable, he makes a very strong argument for how detrimental these fees can be to your overall financial success. If you haven’t read either of those books, I would suggest doing so as it will get you fired up to take action.

Even if you are not paying a financial advisor to manage your investments, when you account for expense ratios, transaction costs and other types of random fees that you and I aren’t really aware of, many funds (depending on the type of account) have fees that are north of 2%.

Is 2% a big deal? That’s the problem…2% can have a creeping effect that doesn’t make you realize the damage in the short term but will certainly have a significant negative long-term impact.

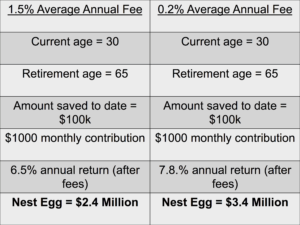

Check out the table below which highlights two different portfolios, one with a 1.5% average annual fee and the other with a 0.2% average annual fee. This calculation assumes the investor is receiving an 8% average annual rate of return less the annual fee.

Did you see the $1 Million mistake?

The investor with the lower-fee portfolio (0.2%) has a nest egg that is worth $1 Million more than the investor with the 1.5% fee portfolio.

Here is the amazing thing…the only difference in this example is the fee!

To compound this mind blowing reality, this difference may even be more for a lot of people reading this blog post over their saving years because their total fees may be even higher than the example used!

All other factors remain constant meaning that you, the investor, can make the same contribution with the same variables yet have a $1 Million greater result by ensuring you are in well-performing, low-fee funds. A Good example is an index fund. These are funds that track a specific market index (such as the S&P 500) rather than try to beat the market.

If you’re looking for some extra help with investing and choosing specific funds, you can book a free call with the YFP financial planning team.