Special Update: Student Loan Announcements from the Biden Administration

This is a special update with more information about the student loan announcement that was announced on August 24, 2022, from the Biden Administration. We know this update is top-of-mind for many pharmacists in the Your Financial Pharmacist (YFP) community and will update this post as we know more.

Check out this special update YFP podcast episode to learn more.

Let’s jump in with the updates:

1. Another Extension of Administrative Forbearance

It’s been almost three years since student loan payments were put on hold, and borrowers now have another extension that pauses both payments and interest.

The extension of the administrative forbearance will continue through December 31, 2022, with payments expected to begin starting January 1, 2023.

Although the forbearance has been extended in the past, we do think this is the last extension.

As before, all $0 payments will continue to count towards PSLF (Public Service Loan Forgiveness).

Announcements from student loan servicers should come out sometime between now and the end of October 2022. This communication should include payment amounts, employment certification requests if needed, and other information.

For pharmacists that graduated in the last 3 years, this will be the first time student loan payments will be made. Those pharmacists that were already making payments and had a pause in doing so will have to start making them again.

Student loans are a big part of the financial plan for the YFP community so payments restarting will impact other aspects of it.

2. Providing Targeted Debt Relief to Low- and Middle-Income Families with Debt Cancellation

Debt cancellation has been a hot topic since the presidential election. President Biden discussed canceling $10,000 of student loan debt, however, borrowers weren’t sure if this would happen.

On August 24, the Biden Administration announced that $10,000 of student loan debt would be canceled for those that have less than $125,000 (single) in Adjusted Gross Income (AGI) or $250,000 AGI (couples/households).

Borrowers that have Pell Grants can receive an additional $10,000 of student loan debt canceled.

For good reason, many questions have been raised with this part of the announcement:

How do I receive the debt cancellation?

How do I know if I’m eligible for it?

What’s the process to get student loan debt canceled?

What year will AGI be taken from?

From the latest information the YFP Planning team has seen, there will be an application that needs to be submitted for debt cancellation. The form should be available by October and submissions are encouraged by mid-November. AGI will come from your 2020 or 2021 tax return.

It’s likely that there will be a 4- to 6-week processing time for applications and applications should be available for one year.

The application is valid for undergraduate or graduate loans and Parent Plus loans, Direct loans, and some FFEL loans will qualify (note that not every FFEL is under a federal loan servicer and private servicer loans are not an automatic qualification). Clarification is needed here.

3. New and Improved Income-Driven Repayment Plan

A new and improved income-driven repayment plan hasn’t formally been announced, however, we do know that the biggest benefit is that it’s going to decrease the overall amount of required minimum payments for those that choose this plan.

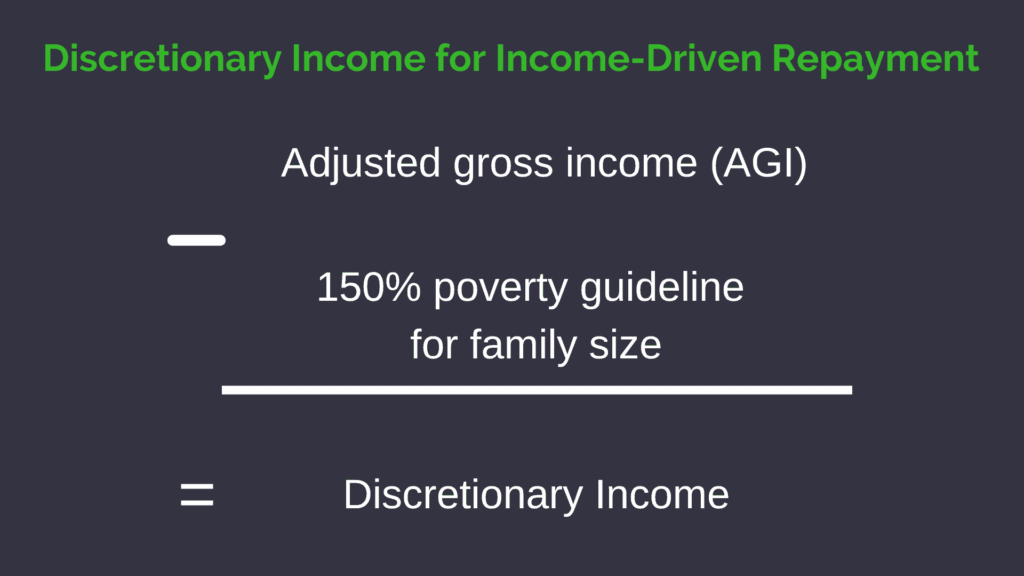

Here’s how the income-driven repayment plan currently works:

Payments are based on a percentage of your discretionary income. From the federal government’s perspective, your discretionary income comes down to two things: your adjusted gross income and the U.S. poverty guidelines for your family size. For the current Income-Drive Repayment plan, discretionary income is your adjusted gross income minus 150% of the poverty guidelines. From there, your payment under this repayment plan is 10% of your discretionary income.

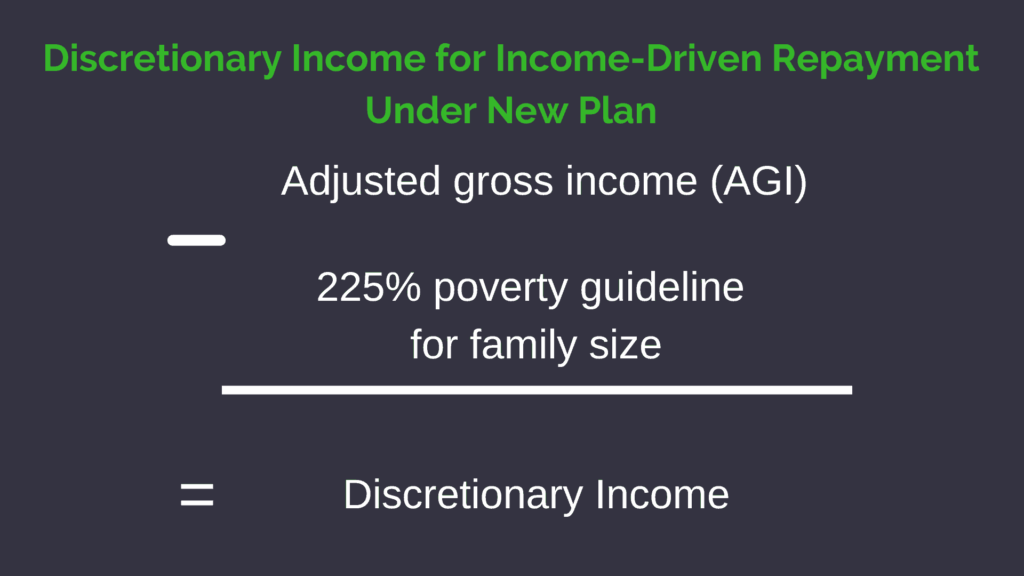

With the updated plan, your discretionary income will be calculated this way: adjusted gross income minus 225% of the poverty guidelines. With this updated plan, your payment is decreased to 5% of your discretionary income.

If you have graduate loans or a combination of undergraduate and graduate loans, a weighted average will be taken.

Calculators will be made available before payments start in January so that you can estimate your payments.

We should expect to hear something about this new plan and when to apply for it in the coming announcements.

It’s important to remember that while this may benefit many, it doesn’t mean that choosing this plan is the best for your personal financial situation as you would need to recertify your income based on your 2021 taxes if you haven’t recertified in a long time.

So what should you do while we wait for more information to be announced?

- Get prepared to start making payments in January and estimate what that payment amount will be

- Find out if you have a Pell Grant by visiting studentaid.gov

- Make sure you can log into your loan servicer, especially if you are pursuing PSLF

- Once you submit an application for cancellation when the time comes, be sure to check your balances to ensure that it happens

- The temporary waiver for PSLF is scheduled to be in effect until October. Make sure to recertify your employment if you haven’t already so that it picks up all possible payments that you could be eligible for.

Still have questions? We can help.

We know that navigating student loan repayment with or without changes to the income-driven repayment plan and the announcement for debt cancellation is overwhelming.

Now is the perfect time to get a handle on your student loans and determine the best strategy to tackle your loans.

Your Financial Pharmacist offers a Student Loan Analysis with one of YFP Planning’s Lead Planners, Kelly Reddy-Heffner, CFP®, CSLP®, CDFA® or Robert Lopez, CFP®. During this analysis, they’ll evaluate all of your options and decide on the best repayment plan and strategy for your personal situation.

Get all the details and purchase your student loan analysis with Kelly or Robert here.

Have additional questions? Email [email protected] and join the YFP Facebook group.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]