Buying a House with Student Loans

Each month, many pharmacists throw thousands at a seemingly endless mountain of student loans often making it difficult to contribute to other financial goals such as savings and retirement. In addition, the dream of owning a home can seem completely out of reach. In fact, according to the National Association of Realtors, 83% of people aged 22 to 35 with student debt who haven’t bought a house yet blame their educational loans. This leads to the obvious question: How do I buy a house with student loans?

If you’re a pharmacist with typical student loan debt, you probably started or are starting your career with a significant negative net worth. Terrifying, I know, as this was exactly the position I was in. I pulled up my old budget while writing this post and although I cringe to admit it, my wife and I actually bought a house with a net worth of negative $262,000. Looking back, we probably could have prepared a little better, but at the time our top priority was buying a house even with our student loans. I’m happy to report that 4 years down the road we are in a much better position and buying our house at that time ended up being a great decision. Although you may be feeling like home ownership is far out of reach and years down the road because of student loans, you can still make it happen.

This post will explore the different strategies on buying a house with student loans and the advantages and risks of each. Because there are many factors that go into this decision, the goal is to help give you some tips so you can identify the strategy that best aligns with your goals.

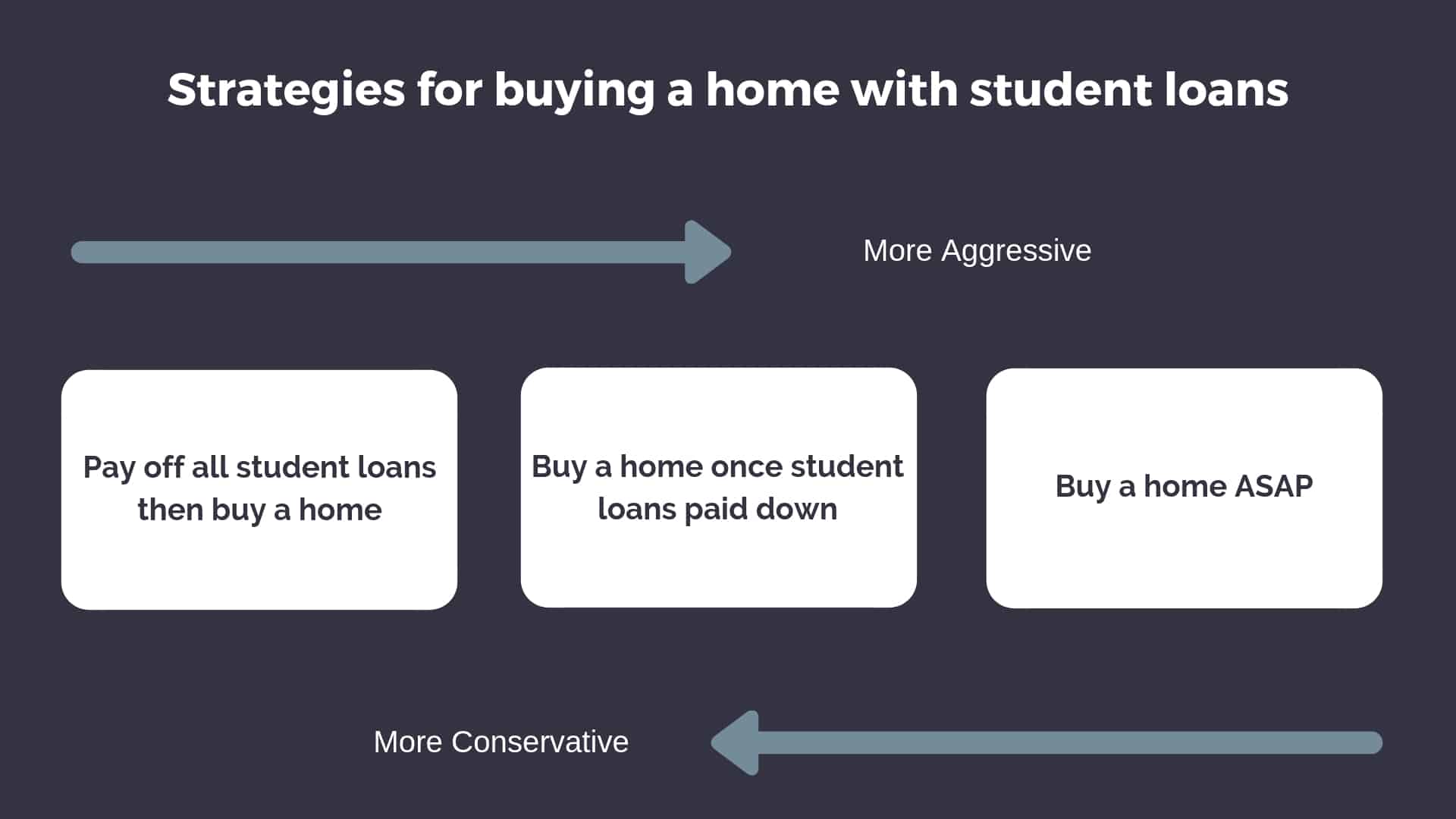

Three Strategies for Buying a House with School Debt

There are three main strategies for buying a house with school debt. The first is to simply accept that you are going to be in debt up to your eyeballs for several years anyway and buy regardless as soon as you can. While certainly not the most conservative approach, the appeal of owning instead of renting can be a powerful motivator. The second tactic is the opposite of the first. Pay down ALL of your debt including student loans before jumping in and buying a property aka the “Dave Ramsey” method. The third and final strategy is a hybrid of the first two. The idea is to really assess your finances and pay down your student loans to some amount and then purchase. We’ll explore each option but let’s discuss some fundamentals first.

Renting vs Buying

Beyond answering the question of “how do I buy a house with student loans?”, there’s another common related question. That is: “Is it better to buy or rent?”

Many people make the argument that buying is always better than renting because you aren’t “throwing away money” and you get the opportunity to build equity. In addition, the statement of “if the mortgage payment is the same as the rent payment then buying makes sense” is commonly made.

Because of the way mortgages are structured with the amortization schedule, you actually don’t build much equity at all in the first few years as the majority of the payment will be going toward interest. Also, owning a home is hardly just making the mortgage payment. There are taxes, insurance, some communities have HOA fees, and stuff tends to break.

This question of buying or renting rarely has a simple answer and there are a lot of factors that can go into a comparison. These include the details of a potential mortgage, years you plan to be in the home, speculation of the home price growth and rent growth rate, inflation, your income taxes, as well as maintenance costs and fees.

While this topic could easily be it’s very own post, this is something to keep in mind even before getting into the different strategies. If you really want to crunch the numbers with considerations in your location, consider using the NY Times Rent vs. Buy Calculator.

Are You Ready?

Regardless of the strategy you choose, buying a house with student loans is a big decision and you need to be ready to take on that responsibility. Certainly, you have to have your finances in order to make it happen, but you also want to be emotionally prepared. That means being on the same page with your spouse or significant other and being able to devote time and energy to the entire process. That also means having your priorities and goals in place. Before getting into the numbers here are some key questions to answer:

- Are my student loans and other debt causing significant stress?

- When do I want to be free of student loan debt?

- Am I adequately contributing to my retirement fund on a regular basis?

- Have I built an emergency fund?

- How will buying a home impact achieving my other financial goals?

Know Your Budget

Knowing your budget is key in this process and something you should establish before even getting preapproved or meeting with a mortgage lender. If you don’t do this, the lender will try to set it for you. Remember, the more debt you take on, the more you will pay in interest and if your mortgage takes up a huge chunk of your budget (a situation known as being house poor), it could put a strain on achieving your other financial goals.

Some people brag about how their mortgage is less than they would be paying in rent. However, they often forget to take into account things like home repairs, property taxes, maintenance, and insurance. Don’t ignore the full costs of a mortgage when setting up your budget. Check out our free guide on home buying for pharmacists if want to review all costs associated with buying a home.

Even if you think you’re ready to go all in and buy a home even with a large student debt load, you will have to meet some minimum financial requirements in order to get approved for a mortgage.

Debt-to-Income Ratio (DTI)

When a bank calculates how much they can lend you, they use the “28/36 rule” for conventional financing. This means that no more than 28% of your gross income may go to your total housing expenses. Furthermore, no more than 36% of your gross income may go to all your debts. Keep in mind these are maximum limits the banks set and stretching your budget to these rules could make it difficult to afford.

Let’s see what that looks like using an average income and debt load for a new pharmacy graduate. Let’s assume you make $115k in gross income. You have $160,000 in student loans with a 6% interest rate and a repayment term of 10 years ($1,775 per month). You also have a car loan and pay $350 per month towards that debt. The bank starts by calculating your 28/36 maximums.

28% rule = Max monthly housing expenses

$115,000 x 0.28 = $32,200 per year or $2,683 per month

Using the 28% rule, your total housing costs (Principle, Interest, Taxes, Insurance) cannot exceed $2,683 per month. (This equates to around a $450,000 house loan for a 30-year term) Assuming you pass the first test, they move to the 36% rule.

36% rule: = Max monthly gross income going to debt

$115,000 x 0.36 = $41,400 per year or $3,450 per month

Remember, the bank will not extend a loan that requires payments in excess of the 36% rule maximum of $3,450 each month. Your total debt payments each month with student loans and car payment currently sit at $2,125.

$3,450 – $2,125 = $1,325

(Maximum Debt)-(Current Debt) = Housing Allowance

This changes things quite a bit. Your $450,000 house loan was just reduced to $185,000. And remember this is the maximum the bank thinks you can afford but not necessarily what your personal budget may be able to handle. Your own financial situation will dictate whether these limits will become an issue for you or not. If you do find yourself over or very near the limit, there are a few things you can do:

1. Raise your income. Remember, it’s a ratio based on your debt AND your income. Starting a side hustle or a second job can give your top line the boost it needs to get you out of the red.

2. Lower your debt. If you pay off a credit card, sell your car for a cheaper one, or refinance student loans, you can adjust the debt side of the equation in your favor. If you don’t plan to use a loan forgiveness program, definitely consider refinancing your high-interest student loan debt through one of our partners. You can lower your DTI, pay less in interest over the life of the loan, and get a nice cash bonus!

If you are pursuing the public service loan forgiveness (PSLF){ program, then your goal should be to pay the least you can over 10 years. You can lower your monthly payments by decreasing your adjusted gross income (AGI) with pre-tax retirement contributions (i.e., 401(k), 403(b)). Lowering your payments in this way will also affect the numbers in your 36% rule.

[wptb id="15454" not found ]3. Consider a different loan product. While conventional loans use a 28/36 rule, there are many government-backed loan options that have looser requirements for DTI. FHA underwriting, for example, allows for limits up to 31% of your gross income and 43% of your total debt load. If you want more information on multiple loan options, check out our free guide on home buying for pharmacists. It’s also worth mentioning that these limits are in place to protect you from buying outside your means and it’s usually not in your best interest to try to work around them.

4. Reassess the size of your mortgage. This might seem obvious, but if you get to this point and still can’t make the numbers work, you might simply trying to buy too much house. In fact, the harder you have to work to get around your DTI ratio, the more likely it is you need to reassess your overall budget. This can be a hard pill to swallow if you’ve already located a house you really want. If you need a reminder for why these limits are important, just look back at 2008 when the housing market collapsed. A good portion of that failure came from people who owned too much house and too much debt for their income to sustain.

Credit Score

Next up, get your credit score up. There are countless reputable sites for obtaining your free credit score without it affecting your report. Most banks and credit cards even provide monthly credit reports so you can track things over time. Most lenders want your credit score to be above 750 for the best rates possible. Pulling your own credit score allows you to review the report for errors before heading to the bank. According to the FTC, more than 20% of consumers found errors on their credit reports that could be affecting their score.

Speaking of credit, regardless of the strategy you choose, you should knock out any existing credit card debt. The average APR for a credit card is 17%. This means that any gains you make with a good investment elsewhere are going to be eaten up by the interest costs of your credit card.

Down Payment

Often, saving up enough cash for a sizable down payment is one of the toughest parts of buying a house with student loan debt. With retirement contributions, other debt payments, rent, emergency funds, and everything else, it can be quite a challenge to save the thousands required. Although it’s easier said than done, try to use the process of accruing your down payment as a test for your new budget as a homeowner. Unexpected costs are going to come up and learning to live off a leaner budget now can help to ensure your success down the road. If you’re still struggling but have a generous family member, monetary gifts can also be used as your down payment without penalty. Don’t forget, while most conventional loan products require 20% to avoid private mortgage insurance (PMI), there are a number of options available with down payments as low as 3.5%.

All of these factors will be used by your lender to determine the loan products you are eligible for and the size of payments you can expect to make. Once you’ve crunched all the numbers and done all the homework from above, you’ll want to go ahead and get pre-approved.

Consider a Professional Home Loan

You’re well aware that student loans can make it challenging to save a 20% down payment (or else you wouldn’t be reading this post), especially if you live in a market where home prices are high and you have other competing financial priorities.

Additionally, getting approved for conventional loans can be tough because most lenders will count your student loans when determining your debt to income ratio as I mentioned earlier.

YFP has been on the hunt for another possible solution for you when a large down payment or conventional loans are out of reach.

We partnered with IberiaBank who offers a Professional Home Loan (aka Doctor’s Loan) that is available for pharmacists.

The Professional Home Loan product offers a 3% minimum down payment without PMI and is available in all states except Alaska and Hawaii.

Learn more about this loan product and the 5 easy steps you can take to get a home loan even if you don’t have 20% down.

Mortgage Calculator

Another Tip Before Moving Forward

Something that’s often overlooked as part of the home buying process is having good disability and life insurance policies in place. Your ability to pay for your home and student loans is dependent on you earning an income each and every month. If you became disabled because of an accident or illness and are unable to work, disability insurance will provide you with money to help replace your income. If you were to die unexpectedly, your mortgage will usually pass on to your spouse if he or she is on the loan. A strong life insurance policy could pay off the remainder of the mortgage or be enough so that your significant other could continue to make the monthly payments.

Ok. Now that you have your priorities in place and have done some due diligence, let’s explore some of the pros and cons of each of the strategies I mentioned above.

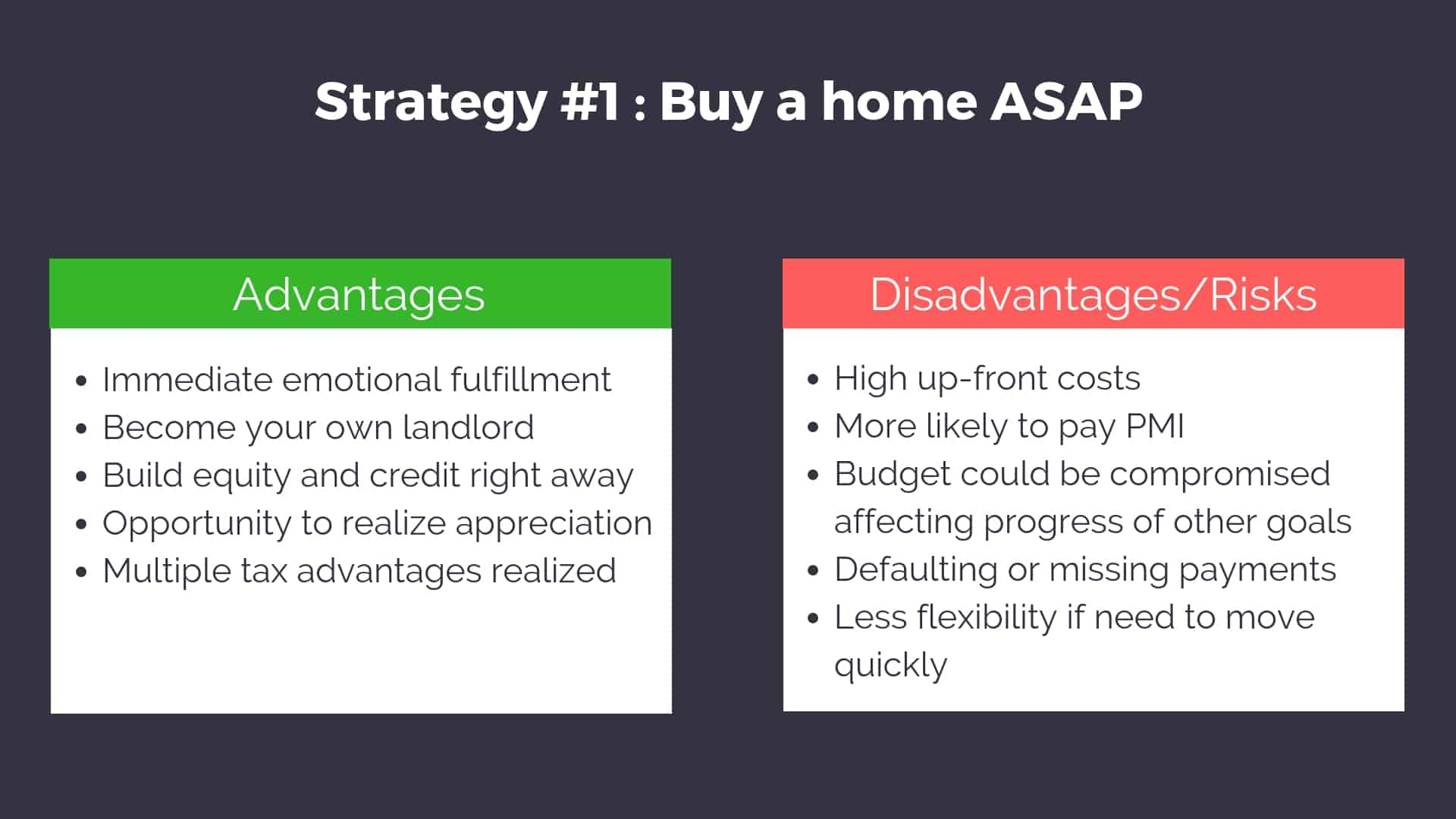

Strategy 1: Buy a Home ASAP

Let’s face it, a great deal of the decision to buy a home comes from your heart and not your head. Of course, you want to make a sound financial choice, and most homes are just that, but sometimes you also just WANT TO OWN A HOUSE.

My wife and I have owned our current home for a little over 4 years now. It’s very difficult to beat the feeling of security and peace of mind I have knowing that my daughters have a safe place to sleep every night. I never have the threat of a landlord deciding to sell the property, or raising the rent, or simply kicking me out with only 60 days notice. I can put effort into my home and enjoy the benefits of that effort. This is something that connects us to the property in a way a rental never could.

This strategy is for people who are looking for that feeling and are looking for it right now. You may also choose this strategy if you are someone who is confident in your housing market and feel that you can take advantage of the projected appreciation and resale opportunity.

There are some compromises of course if you choose this path. For starters, you may not have enough saved up for a full down payment. This means a larger mortgage payment in addition to paying private mortgage insurance (PMI), which will ultimately increase the total cost of the house. Depending on the size of the mortgage, you could put a strain on your budget making it harder to pay off other debts or to contribute to savings and retirement.

Also, if you pursue this strategy with very little equity, it could be very difficult to move if there was a dip in the housing market and your upside down and you owe more than the home is worth. Therefore, you have to be comfortable with this risk.

This strategy could definitely make sense if your student loan strategy involves one of the federal forgiveness programs, especially PSLF since you are anticipating having student loans for 10-25 years and will be making income-driven payments. Because there is a standard term to get the full benefits of forgiveness, it doesn’t make sense to make extra payments since you can’t accelerate the process.

If you choose this strategy, consider building a decent a down payment and a mortgage size that doesn’t cause too much stress on your monthly budget and make it impossible to make progress with your student loans and other financial goals.

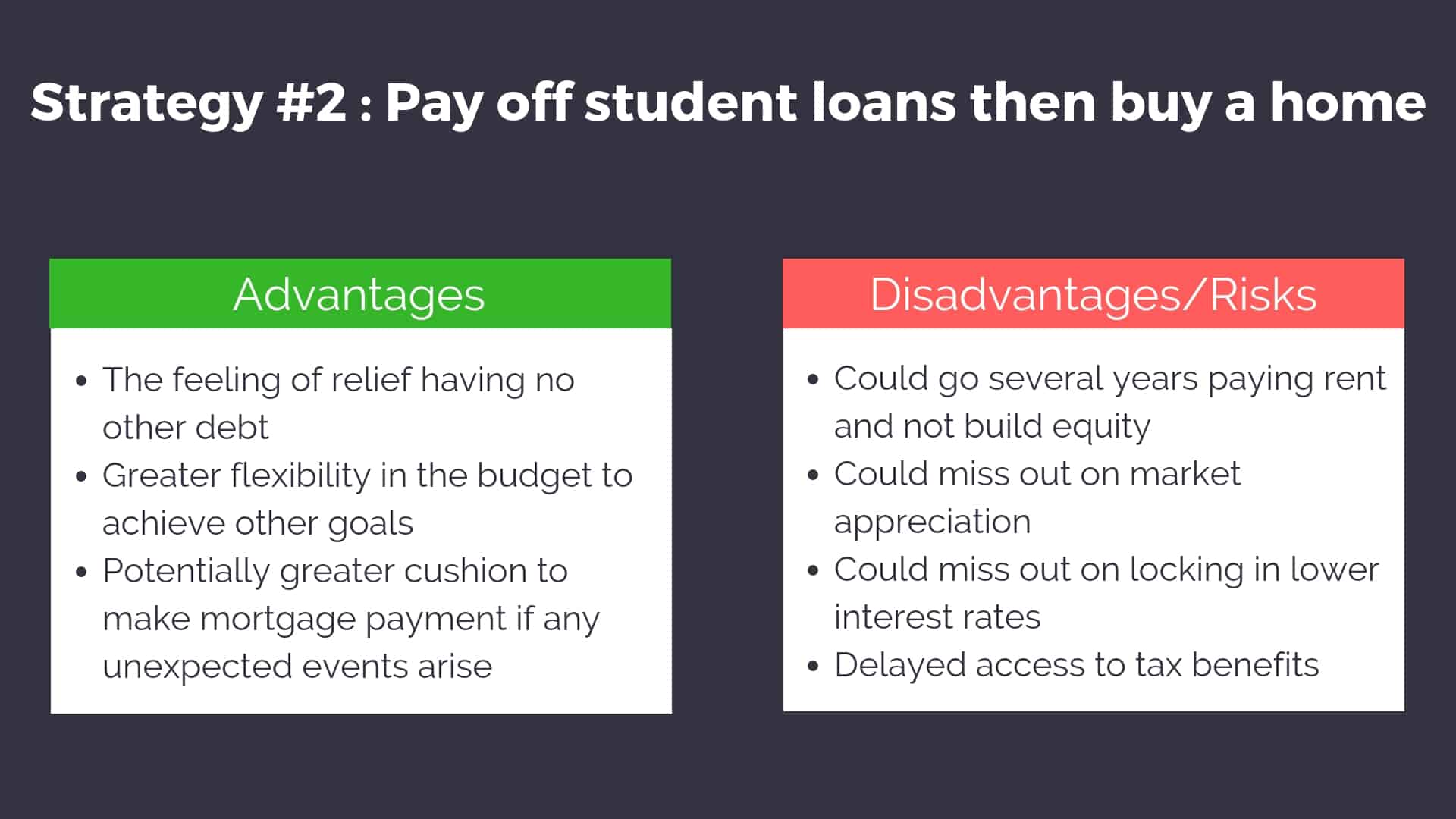

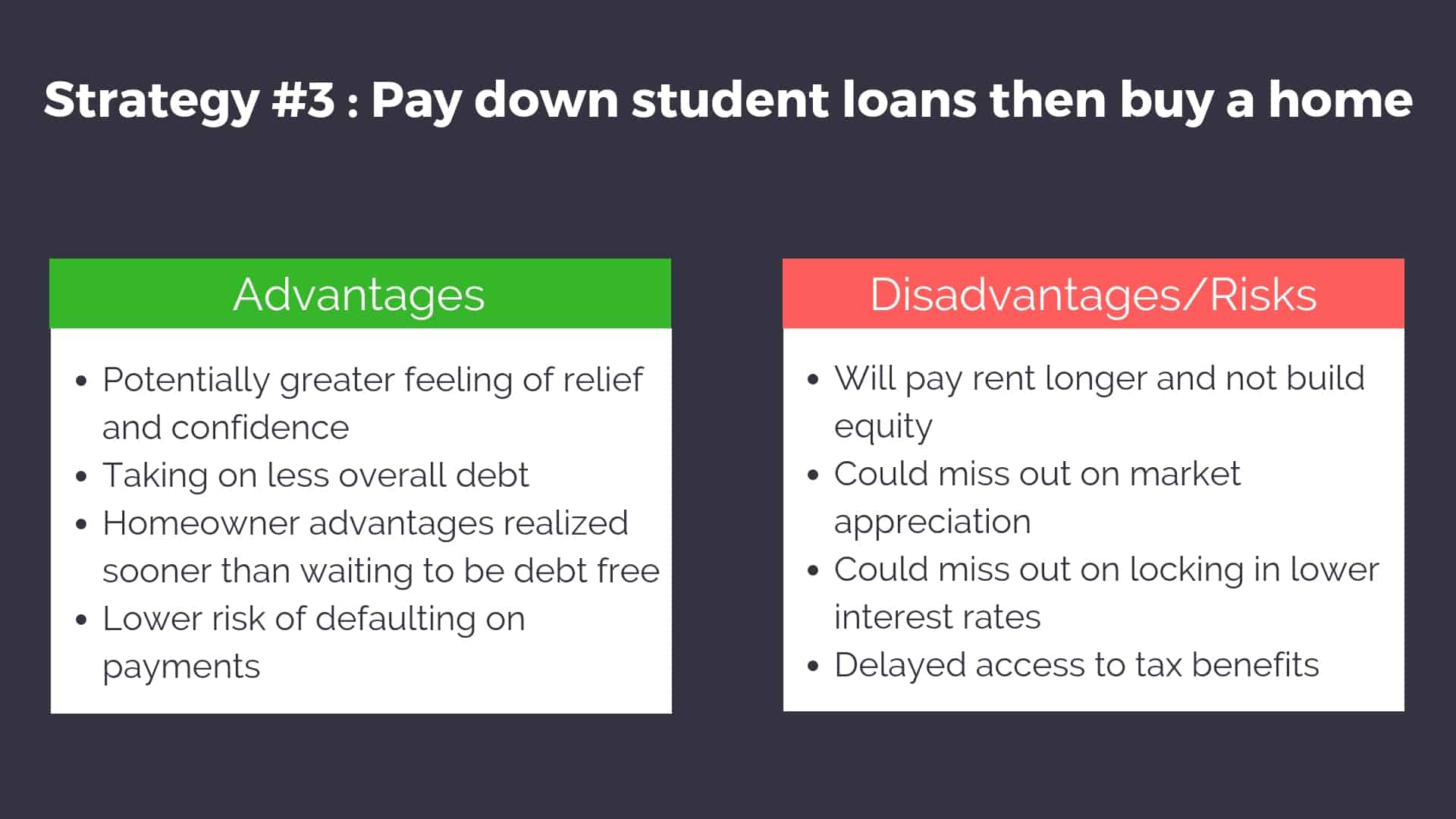

Strategy 2: Pay off all student loans then buy a home

If the thought of your student loans makes you sick to your stomach, adding more debt by buying a home may be the last thing on your mind. This strategy focuses on paying off your biggest debts before adding more to your plate. This is the true Dave Ramsey philosophy and is a strategy for people who can handle delaying their gratification.

The advantage here is all about flexibility. You have the ability to move relatively easily if you experience a job change or life event. Renting requires far less in upfront costs compared to buying so you retain more flexibility in your budget for paying down other debts faster. The costs of renting are also much more predictable given you won’t have repairs or capital expenditures to worry about.

The tradeoff is you will miss out on the benefits of being a homeowner until later. Namely, building equity and tax benefits. Interest rates are also increasing at the moment and if trends continue, they could be significantly higher in just a few years. Missing out on a lower interest rate now could mean spending quite a bit more down the road. Plus, depending on the size of your student loans and potential mortgage it could take several years to clean that up and then save enough for a down payment.

Many people who follow this approach simply hate the idea of being indebted any more than they have to be or fear the possibility of defaulting on payments with a sudden change in income.

Strategy 3: The Hybrid Approach

The third and final approach attempts to mix the best aspects of the initial two. The basic philosophy is this: Pay off a portion of your student loans and lower your debt to income ratio, save up a sizeable down payment, and buy a home when you are more financially stable.

If you use this approach, what percentage of your student loans should take out prior to pulling the trigger on a home? It really comes down to what your comfort level is and how long you want to delay the homebuying process.

Similar to the last strategy, you will miss out on some of the benefits of being a homeowner for a period of time potentially missing out on market appreciation and locking in a lower interest rate.

Like strategy #1, this hybrid approach would definitely make sense if your student loan strategy involves one of the federal forgiveness programs.

Conclusion

Buying a house with student loans can certainly feel overwhelming. There are emotional and financial points to consider that are often at odds with one another. There are three basic strategies to consider and what works best for you will be dependent on your situation including your priorities, emotions, financial position, and risk tolerance.

Have more questions about buying a home with student loans? Nate Hedrick, the Real Estate RPh, is a full-time pharmacist and licensed real estate agent. Head on over to yourfinancialpharmacist.com/real-estate to get in touch!

Current Student Loan Refinance Offers

[wptb id="15454" not found ]

2 thoughts on “Three Strategies for Buying a House with Student Loans”