7 Programs for a California Pharmacist to Conquer Student Loans

The following post contains affiliate links through which YFP LLC. or its team members receive compensation.

California has the most practicing pharmacists in the U.S. which is no surprise given it’s the most populous state.

It also has the most pharmacy schools at 13 and pharmacists earn the second highest mean salary next to Alaska at $136,730.

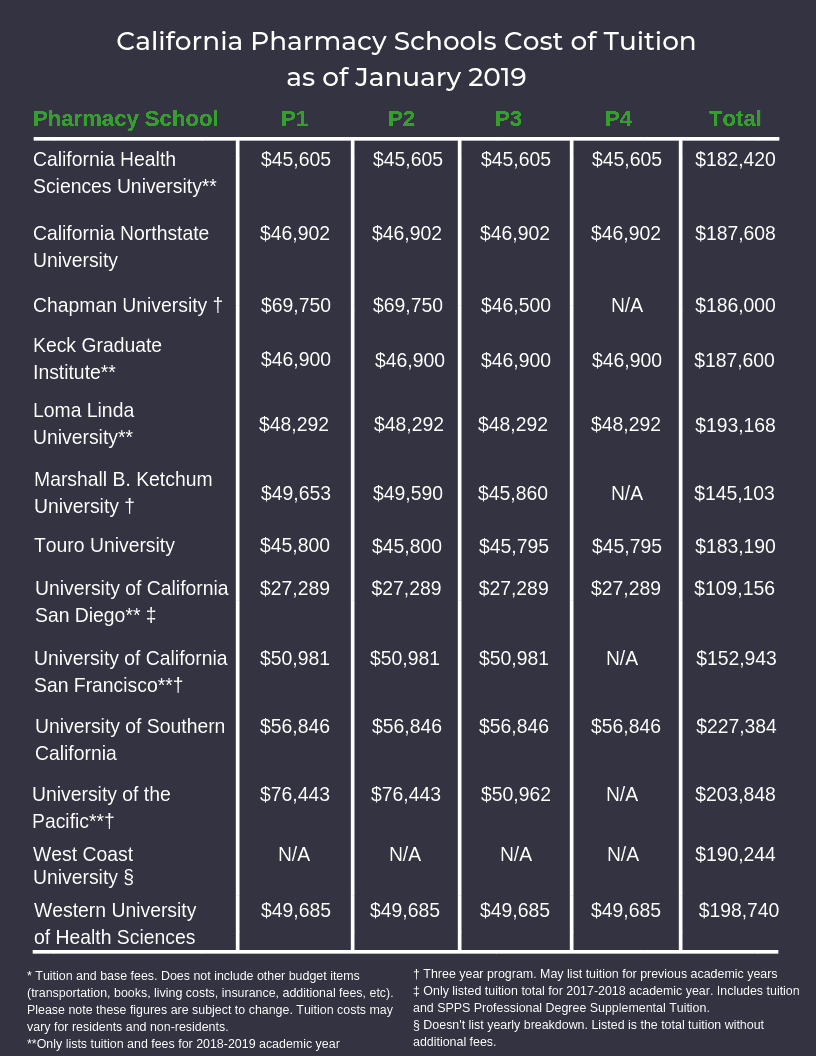

Unfortunately, for a California pharmacist, the effective salary can feel much lower secondary to high taxes and cost of living. Not only that, most pharmacy graduates will face much higher debt loads than the national average when adding in the cost of living. With this high debt to income ratio, it could be hard to make progress and even make minimum required payments on student loans. Below is the current cost for California pharmacy schools as of January 2019.

Consider a California pharmacist with $300,000 in student loans with a 7% interest rate. The default standard 10 year plan through the federal loan system would have a monthly payment of $3,483. Unless there’s spousal income or additional streams of revenue, making that kind of payment probably isn’t possible. Plus, even if one could make that payment, it would likely stretch the budget so much that it would be tough to put any money toward other financial goals like investing and purchasing a home.

If you currently don’t have an income because you have been affected by the CPJE scandal or you are between jobs and making a transition, check out the end of this post for tips for some temporary options.

So besides paying off student loans into retirement, let’s explore some other options.

Here are seven to consider.

1. Education Debt Reduction Program

Besides the loan repayment programs offered through the military, one of the most generous federal loan repayment programs is the Education Debt Reduction Program (EDRP) through the Veterans Health Administration (VHA). While not unique to those practicing in California, there are a large number of facilities within the state and therefore more potential opportunities.

Through the program, pharmacists can receive up to $120,000 over a 5 year period with a maximum of $24,000 per year. Unfortunately, this is not always available and depends on the need and difficulty in filling positions. EDRP was not available for my position when I joined the VA, but a lot of my friends, including Alex Barker of thehappypharmD.com, took full advantage of it.

Unlike some programs which provide direct student loan repayment, this is a reimbursement program. So if you pay $24,000 per year toward your loans, the VA would reimburse you $24,000. If you have a total student loan balance around $240,000, you would essentially be responsible for paying for half plus any interest. With balances less than that, it would make sense to make payments less than $24,000/year to enable you to maximize the benefit.

Job postings on usajobs.gov usually have this listed for VA positions if available but always check with human resources if you are interviewing.

2. Indian Health Service Loan Repayment Program

The Indian Health Service Loan Repayment Program (IHS LRP) offers up to $40,000 in exchange for a 2 year full-time service commitment working in an Indian health facility. This program can be extended annually if you continue your service until your entire student debt is paid. Currently, there is no max established.

This program is also not unique to California, but there a large number of Indian health facilities compared to other states. Similar to the EDRP, this program is also based on facility and provider-specific needs.

If you accept the IHS LRP award, you cannot receive any other awards from any other government entity that also requires a service commitment.

You can find job listings that offer the IHS LRP award on usajobs.gov.

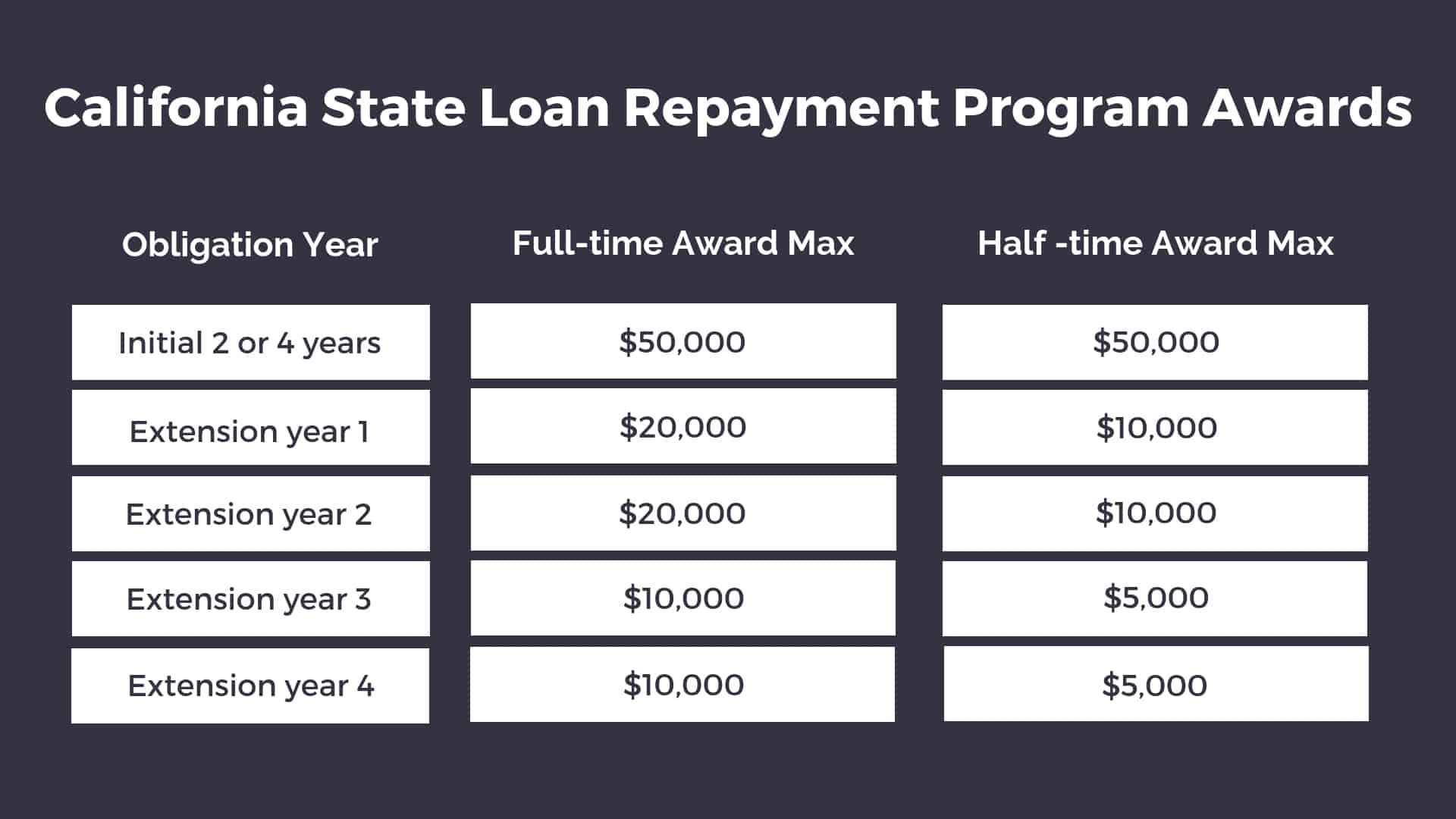

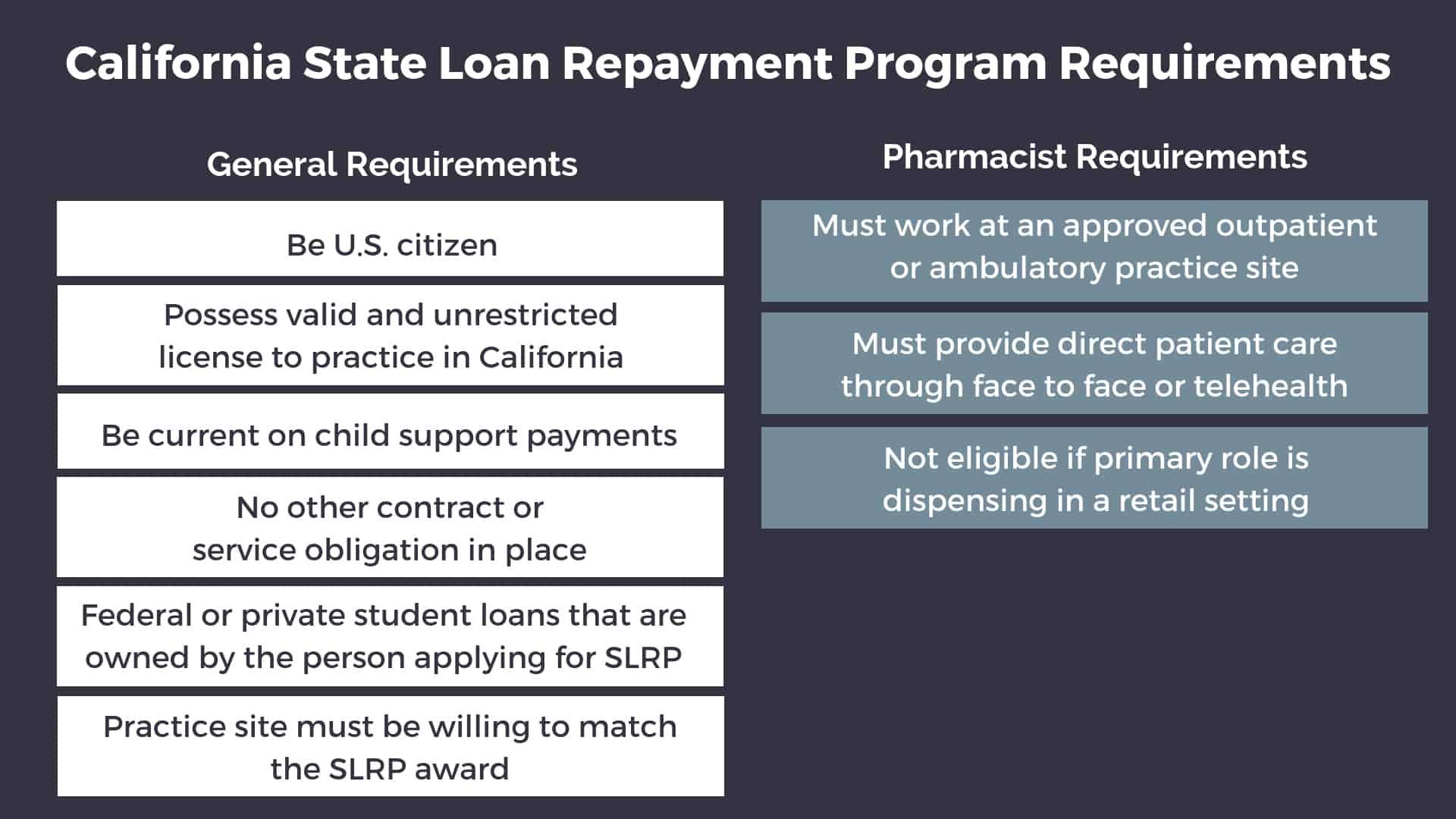

3. California State Loan Repayment Program

To increase the number of medical professionals in Health Professional Shortage Areas (HPSA), the state offers the California State Loan Repayment Program (SLRP). This program is open to several healthcare professionals, including pharmacists, who work for approved practice sites in shortage areas.

While this strategy may not completely eliminate your loans, it can help take out a big chunk. For full-time commitments of 2 years or half-time commitments of 4 years, you can receive up to $50,000. There are also extension grants with availability that varies year to year.

Besides the 2 or 4 year initial commitment to work at a practice site that qualifies under the SLRP program, there are other requirements you must meet with some being pharmacist specific.

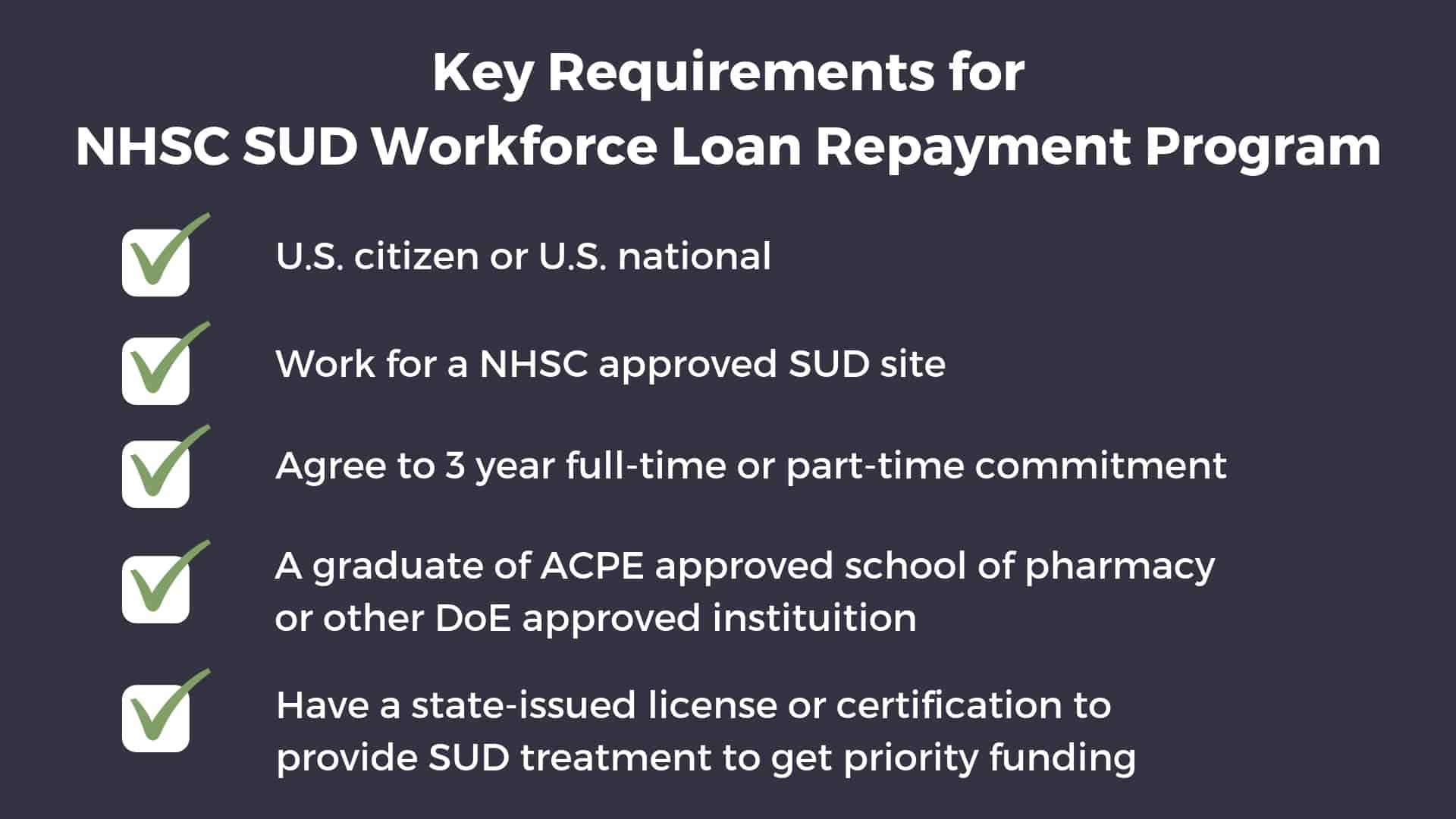

4. National Health Service Corp Substance Use Disorder Workforce Loan Repayment Program

As a measure to help battle against the unfortunate opioid epidemic, pharmacists were recently added as a qualifying clinician eligible for the NHSC Substance Use Disorder Workforce Loan Repayment Program with the main goal of assisting in the treatment of substance abuse in rural and underserved areas nationwide. To be eligible, you have to work at an approved NHSC site that provides Substance Use Disorder (SUD) treatment which includes Opioid Treatment Programs (OTP), Office-based Opioid Treatment (OBOT) Practices and Non-opioid Outpatient Substance Use Disorder Sites.

In addition, to receive priority funding you must have a state-issued license or certification to provide SUD treatment. A provider’s license or certification to provide SUD treatment must meet the national standard recognized by the NBCC; NAADAC, the Association for Addiction Professionals; or IC&RC.

There are two different service options available. The first is a 3 year full-time commitment (minimum of 40 hours/week and 45 weeks/year) which has an award of $75,000. The part-time option is also a 3 year commitment (minimum of 20 hours/week and 45/weeks per year) and has an award of $37,500.

This program is not specific to pharmacists in California but because the state has the most NHSC approved sites in the country at over 1700, there are likely a number of those that could qualify for providing SUD treatment.

For 2019, the deadline to submit your application is February 21st at 7:30 pm EST.

For more information on the NHSC Substance Use Disorder Workforce Loan Repayment Program, check out this video q and a recording You can also click here for the full guidance and requirements and to see if your site meets the qualifications.

5. Public Service Loan Forgiveness

If you work for a government organization, tax-exempt 501(c)(3) company, or a non-tax exempt non-profit (that meets qualifications), then you are eligible for the Public Service Loan Forgiveness program. This would apply to all Veteran Affairs, Indian Health Service, military, and other government pharmacists in addition to those who work for nonprofit 501(c)(3) hospitals.

After making 120 qualifying payments on Direct Loans over 10 years, you can have the remaining balance of your loans forgiven. Not only are they forgiven, but they are forgiven tax-free!

Although there’s a lot controversy surrounding this program, you can’t ignore the math.

Consider a single new grad that starts working for a non-profit hospital with an adjusted gross income of $135,000 and loan balance of $300,000 with a 7% interest rate. If the new grad pursues the PSLF program making 120 income driven payments through either the PAYE or REPAYE plan, the total estimated amount paid would be $149,524, less than half the total balance!

Because your monthly payments are based on your adjusted gross income, there are opportunities to lower them by contributing to tax-favored investments such as a traditional 401(k) and Health Savings Account (HSA). So essentially you can build wealth while paying less on your loans. Pretty cool right? You can learn more about ways to minimize your payments on episode 18 of the podcast.

If you want a step-by-step process on how to pursue PSLF check out this post.

6. Non-PSLF Forgiveness

Did you know that you can get your federal loans forgiven after making payments for 20-25 years? This is another strategy to get rid of your loans outside of the public service loan forgiveness program. With non-PSLF forgiveness, there is no employment requirement. However, you must have Direct Loans and make qualifying income-driven payments every month for 20 years under the PAYE or IBR new repayment plan or 25 years through the REPAYE plan.

Unlike PSLF, you will be taxed on any amount forgiven after that time period which is one key difference from PSLF. Let’s consider the same example of a pharmacist with an AGI of $135,000 with $300,000 in student loans that have a 7% interest rate. If paid over 20 years through the PAYE plan, the total amount paid would be estimated at $400,420. The amount forgiven would be $319,580. That amount would be considered income and so you would need to plan for a big tax bill along the way.

You may wonder why anyone would use this strategy given the amount of interest paid and tax implications. Depending on your debt load, it may actually be your best option. The reason is that you may not be able to make the payments on any of the non-income driven plans or any of the monthly payments on refinance offers. That’s why this strategy typically works best for someone with a very high debt to income ratio (such as 2:1 or higher).

With either forgiveness program, you cannot refinance your loans or you automatically disqualify yourself from the program. For more info on this check out the ultimate guide to pay back pharmacy school loans.

7. Refinance Through First Republic Bank

First Republic is not currently accepting applications for student loan refinancing.

Refinancing can be a solid move to save a ton in interest on your loans. With federal student loan rates at 6-8%, even a small change can lead to big savings, especially if you have a large balance.

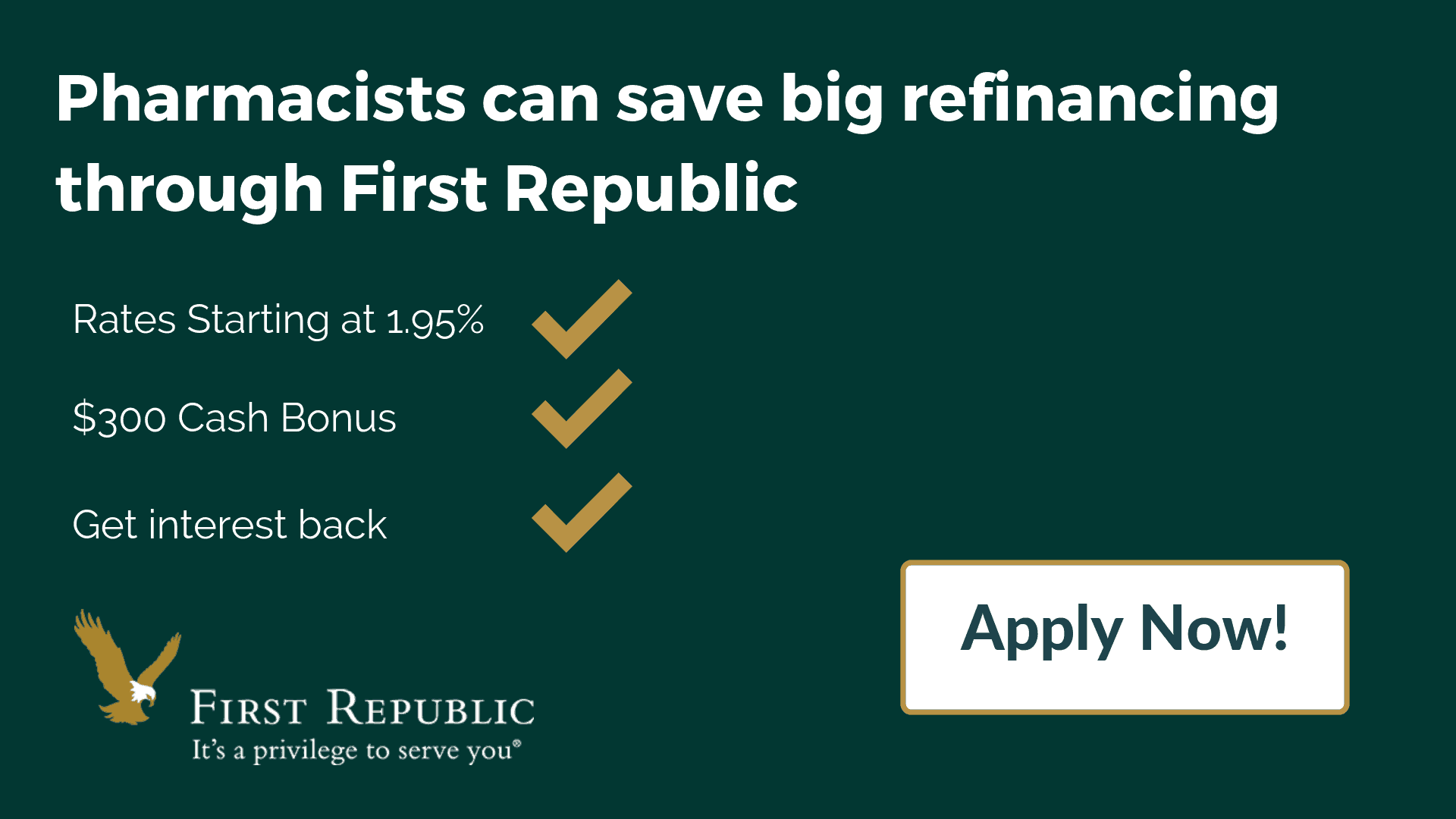

While many student loan refinance companies offer similar benefits, there is one in California that stands out: First Republic Bank.

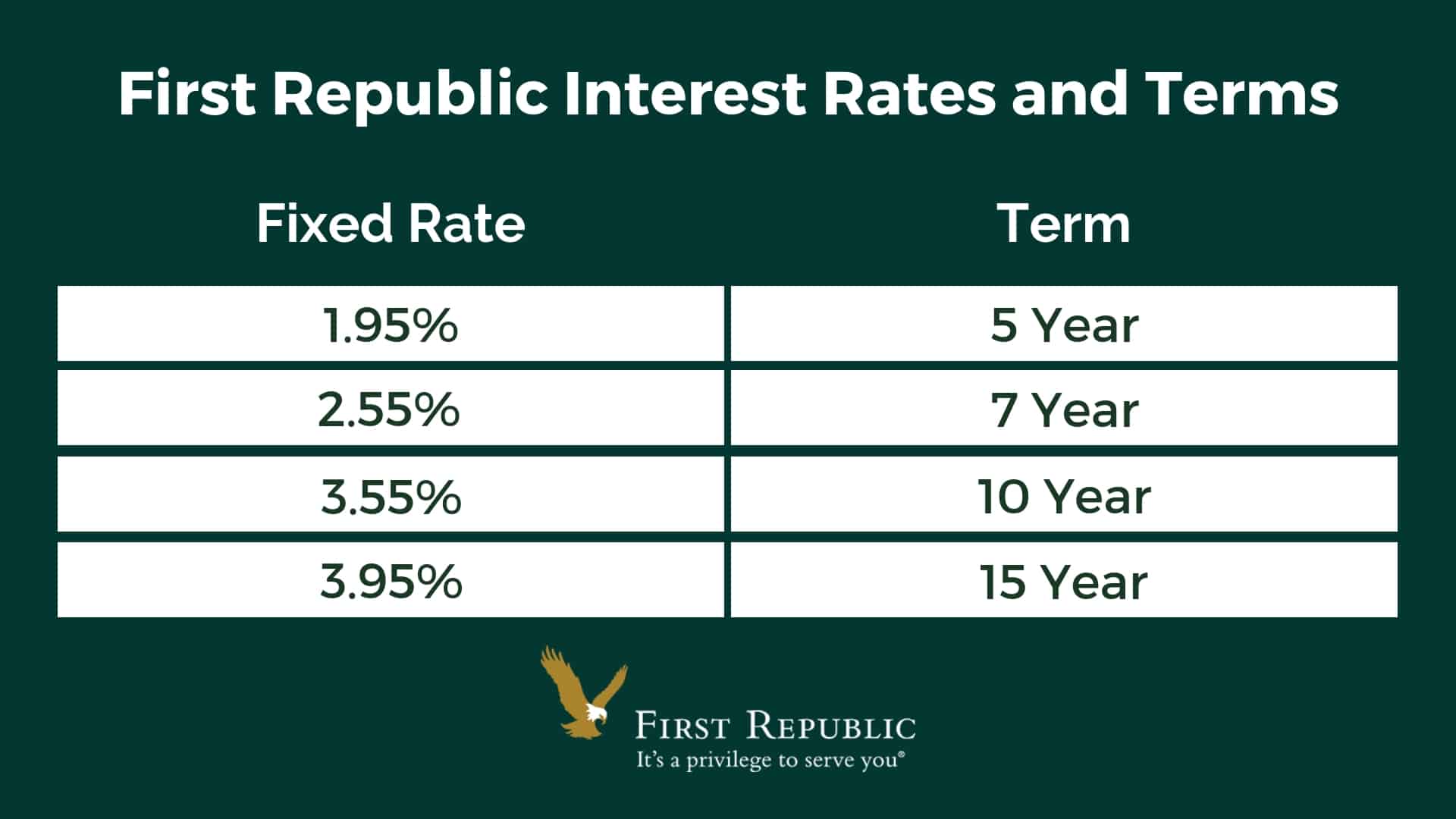

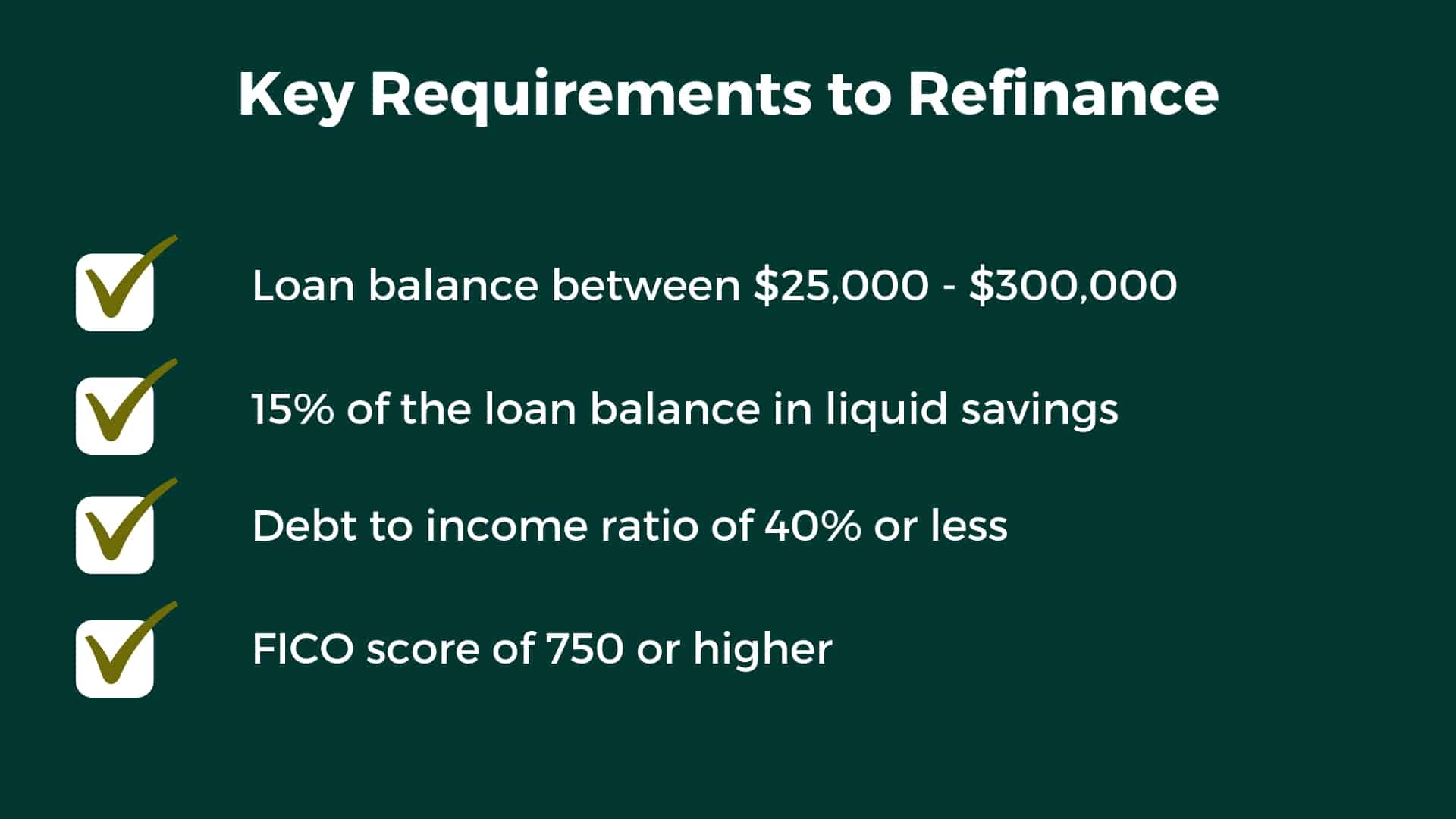

First Republic offers some of the lowest interest rates among lenders nationwide. They are fixed rates and unlike other companies which take your credit history, loan balance, and income to come up with a personalized percentage, First Republic’s rates are the same for everyone. You either qualify or you don’t.

First Republic is pretty conservative and doesn’t just loan money to everyone. You need to be in a relatively healthy financial position with proof beyond just a credit score. Most notably, you need to have 10-15% of your loan balance in liquid assets and a debt to income ratio that’s 40% of less.

Other requirements include the following:

Besides the requirements above, you have to live within 20-mile radius of a physical location. This bank is only available in very select cities and states but California happens to have the most physical locations.

First Republic Bank Locations

- Beverly Hills

- Burlingame

- Corona Del Mar

- Cupertino

- Danville

- Del Mar

- Encino

- Escondido

- Livermore

- San Jose

- Los Gatos

- La Jolla

- La Mesa

- Los Altos

- Los Angeles

- Manhattan Beach

- Menlo Park

- Millbrae

- Mill Valley

- Mountain View

- Napa

- Newport Beach

- Oakland

- Orinda

- Palm Desert

- Palo Alto

- Pleasanton

- Redwood City

- Sunnyvale

- San Diego

- San Francisco

- San Mateo

- San Rafael

- San Ramon

- Santa Barbara

- Santa Monica

- Santa Rosa

- St. Helena

- Studio City

- Walnut Creek

One of the other great benefits with First Republic bank is they will actually give you back the interest you paid up to 2% of the original loan balance if you pay off the loan within 4 years. That may be tough if you have a high balance but definitely a nice perk. The refinance program does not include any forbearance periods or income-driven repayment plans. However, you may be able to extend the term if needed. They also will not forgive the loan if you die or become disabled with a balance remaining so make sure you have adequate coverage. If you want to shop multiple companies to find the lowest cost and best value check out Policygenius.

If you refinance through this unique link, you can a $300 cash bonus. You can also email Andrew Gerber at [email protected] and he will make sure that you get the cash. Just say that Tim Church from Your Financial Pharmacist referred you. You can also learn more about First Republic here.

Even if you don’t meet the qualifications for First Republic, refinancing can still be a good move and there are several other reputable companies that offer great rates and terms. You can check out our partners our refinance page and get up to $750.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]What to do if you don’t have an income

As you probably know (and may unfortunately be affected by this), in October 2019, the California Board of Pharmacy has invalidated around 1,400 exam results for California Practice Standards and Jurisprudence Examination for Pharmacists (CPJE) because of a cheating scandal.

This has caused a significant delay in thousands of pharmacists being able to become fully licensed and practice in the state of California subsequently without an income. With the grace period for federal student loans ending soon for most, one of biggest questions is “What do I do about repayment?”

Fortunately, there are some options through the federal loan system that can help alleviate some of the stress with this situation or transitioning to another job.

If you are about to go into repayment for the first time, one of the best initial moves to make is to do a Direct Consolidation Loan. This will combine all of these loans into one with a weighted interest rate and be serviced by a single lender.

This will automatically convert and make essentially all loans eligible for one of the income-driven repayment plans that qualify for PSLF or non-PSLF forgiveness. While you could choose to put your loans into forbearance to avoid making any payments, interest will accrue while in this status which is why there are better options to consider.

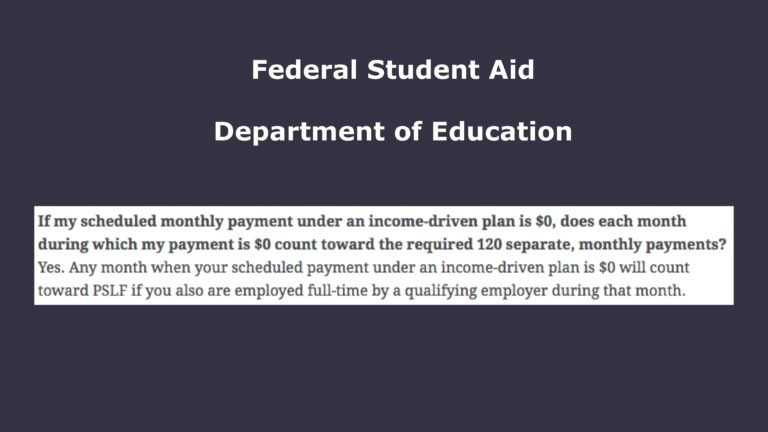

With the income-driven plans, you can report to the Department of Education that have you have $0 in taxable income if that is true, which will result in $0 payments. The good news is that $0 payments still count as “qualifying payments” whether it’s for PSLF or non-PSLF forgiveness. For PSLF they technically will not count though until you have started employment with a qualifying employer. However, based on the income-driven payment certification form, you would not have to report a change in income until you re-certify the following year.

As you are applying for the Direct Consolidation Loan, the optimal repayment plan will depend on a few things. If you’re planning to work at a for profit company such as a community pharmacy and may eventually refinance, REPAYE can be a good option.

Under REPAYE, for all Direct Unsubsidized loans, the government will pay 50% of the interest that accrues every month if your loan payment is less than the amount of the monthly interest. So let’s assume you have $160,000 in student loans at 7% interest. $933 in interest will accrue every month as soon as the grace period ends. If your payment is $0 (which would be the case if you have no current income), the amount of interest that would accrue would only be $466.

If you anticipate that your income will be half or less than half of your student loan balance, PAYE would be a good option because you can get forgiveness after making qualifying payments for 20 years as mentioned above.

If you anticipate working for the government or non-profit organization eligible for PSLF, PAYE or REPAYE will be good options. Since spousal income comes into play for PAYE depending on how taxes are filed (regardless for REPAYE), this would be a key consideration. Make sure you choose FedLoan Servicing as your service when you apply for your Direct Consolidation Loan given they are the exclusive servicer for PSLF.

Obviously, these moves are only going to work if you have federal loans. If for some reason you have private loans, you would have to work with your lender to see what options are available. Some offer income-based payment options, interest only payments, or some form of forbearance. Another potential option is to extend the loan as far out as possible (such as 20 years) to get the lowest monthly payment possible.

Conclusion

The cost to complete some California pharmacy schools is way beyond the median amount borrowed to attend private institutions. With big student debt combined with high cost of living and taxes, a California pharmacist could be starting their career in a tough financial position. Fortunately, there are some state-specific programs available to offer assistance and also federal programs that are especially good for those with very high debt-to-income ratios.