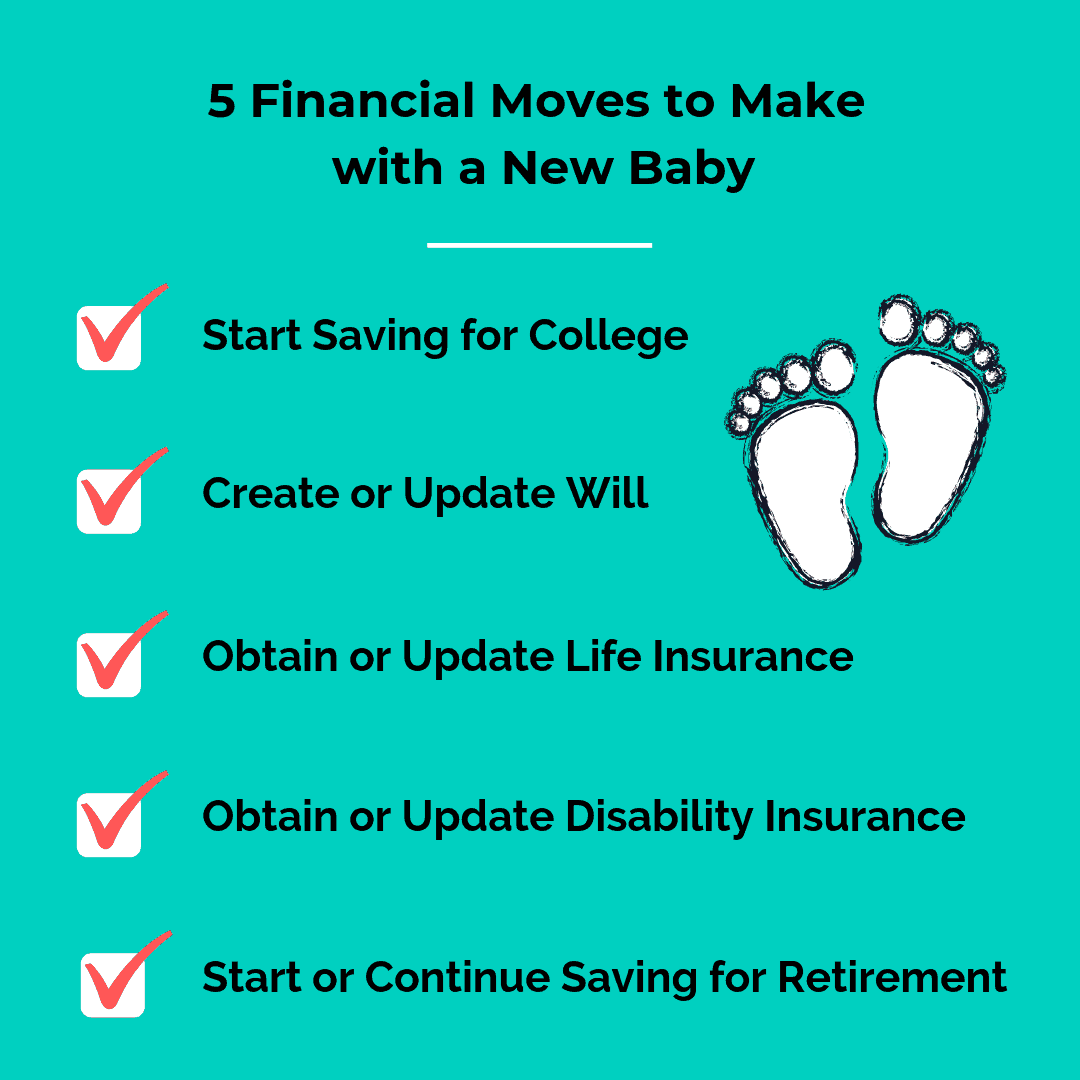

5 Key Financial Moves to Make with a New Baby

The following is a guest post by Karen Berger, PharmD. Karen is a pharmacist and medical writer in Fair Lawn, NJ. Her husband has been trying unsuccessfully to put her on a budget for many years.

This post contains affiliate links through which Your Financial Pharmacist may receive compensation

In an earlier post, we talked about how to prepare financially when expecting. Once your little one makes his or her big appearance, though, the financial planning is not over – it has just begun. Continue to work on those important financial moves we talked about earlier, and start to incorporate these additional tips.

Nothing can prepare you for life with a baby. Whether this is your first or fifth baby, the first few months are exhausting. You walk around on a few hours of sleep every night – getting more than four hours of sleep in a row is cause for celebration. You might not remember the last time you showered or sat down for an uninterrupted meal. Although it is the last thing on your mind, financial planning for new parents is key to ensuring a strong financial position for the upcoming years.

1. Start Saving For College

With the average cost of college for 2017-2018 at $20,770 for in-state public schools and $46,950 for nonprofit private schools (including tuition, fees, and room and board), and prices increasing every year, it is never too early to start saving for college. Don’t forget to multiply these numbers by six (years), the average length of time students take to earn a bachelor’s degree, and also by the number of children you have.

Having a monthly savings goal is a fantastic way to help your children pay for college. NerdWallet estimates that saving $500 a month, per child, earning 5%, should be adequate for you to cover $50,000 of college costs per year for four years once your child turns 18. Obviously if you’re planning to pick up the tab for potential graduate or professional school, you’re going to need to save a lot more. You can find calculator tools online to tweak the numbers to your personal situation. Often, saving for college will involve a combination of several of the strategies below:

529 College savings plan: The 529 is the most popular savings plan geared toward education; there are two types. The first type is the 529 investment savings account. With this plan, you invest with the same risk/return profile of other stock investments. Check your own state for tax breaks or matching funding before looking into 529 plans offered by other states.

The second type is the 529 prepaid tuition plan. This method locks in tuition costs and avoids the yearly increase in tuition. Paying for 6 semesters now, at today’s cost, will pay for 6 semesters in the future, even if the costs are higher at that time. These plans are starting to have more restrictions.

Pros of the 529 include: high contribution rates (plans typically allow up to $300,000 in lifetime total contribution), the ability to change beneficiaries, and the benefit of tax-free growth. Also, if the parent is the account holder, the 529 is considered a parental asset and it will have a minimal impact on financial aid as compared to other education savings options.

On the other hand, there are a few cons of the 529. It is strictly to be used for education, so if your child does not go to college, the money may be unavailable for other purposes. However, depending on the plan, you may be able to change the beneficiary or pay tax and a 10% penalty on the growth of assets. There is also the inherent stock market risk.

Savings Accounts & Other Low-Yield Options: Savings accounts are flexible, but provide little in the way of interest. Using a regular checking/savings account with the intent to save for college may backfire, as money may be tapped into and not replaced. Not only that, but because of inflation which is typically around 2-3% per year, you may actually be losing money keeping it parked here. Certificates of Deposit (CD) and US Savings Bonds are other options, but these are mostly out of favor due to low interest rates. Sometimes, a very conservative contributor may favor this option.

Roth IRA: A Roth IRA can be used as a combination retirement account and educational savings account. It allows you to invest with after-tax dollars while the earnings grow tax-free. Although this is typically used as a retirement account with a penalty for early withdrawals on any growth before 59 ½, if used for higher education, distributions can be taken tax- free and penalty-free. The biggest downside to this is that it could significantly reduce your overall retirement projections. In addition, the distribution must be made in the same year that the qualified expenses are paid. Another item to note is this distribution is considered to be income to the student and could reduce eligibility for need-based financial aid.

Coverdell Education Savings Account (ESA): This is like a smaller version of a 529: it offers tax-free withdrawals, and you can invest in the market. However, one of the biggest advantages is that you will have a lot more investment options to choose from, since you won’t be limited to what’s available to what a specific 529 plan offers. Contributions are limited to $2,000 per year, and until the beneficiary turns 18. ESA’s may offer more flexibility, and qualified expenses may include educational expenses from Kindergarten all the way through graduate school (529 plans also now allow up to $10,000 per year to pay for private elementary and post secondary school tuition).

Important to note with a Education Savings Account is that income limits apply, and depending on your salary/combined salary, you may not be able to participate. Currently, the income limit for a maximum contribution is $190,000 for a married couple filing joint returns, and contributions phase out at $220,000 in 2018/2019. The limit is $110,000 for those not filing a joint return.

If you are indeed eligible to contribute to an ESA, the cool thing is that you don’t have to choose between an ESA and a 529 – you can do both!

Trusts: These are structured as UTMA or UGMA. Assets are transferred to the child’s account and invested on his/her behalf until the child reaches the “age of trust determination,” which is between 18-21, depending on the state. As soon as the beneficiary becomes an adult, he/she can use the money however he/she wishes. As a custodial account, these assets are considered to be assets of the child/student and are included in calculating financial aid. These funds will stay in the custodian’s taxable estate until the child reaches the age of trust determination.

2. Make A Will

This is the happiest time of your life – who wants to think about something depressing like a will? Although it seems sad, a will is a very necessary part of life. Just think about the recent, unexpected passing of 90210 and Riverdale star Luke Perry from a stroke at the young age of 52. That was a major wake-up call for many people to get their affairs in order.

In your will, you will clearly and concisely state your wishes for the distribution of your assets after death, and appoint guardians for your children if both parents pass away. You will designate an executor, who will ensure the provisions of the will are carried out.

You can either hire an attorney to create your will or do it yourself. I would recommend hiring an attorney if you can afford to do so. The attorney handles all of the intricate details, making sure nothing is left out and can keep a copy on file. Attorneys may charge a flat fee or hourly rate, with an average cost of $300-$1000 for an uncomplicated will, or up to $10,000 if you have complex assets and an estate, or the need to establish a trust.

Many companies offer a very affordable legal plan for employees, where you contribute a small amount per paycheck for legal representation by participating attorneys. At the time, my husband and I were able to do both our will and closing on our house, and we did not have to pay anything above the regular paycheck contribution.

If you would rather create a will yourself, you can use an online program or software to make a will for less than $100. Requirements for witnesses or other specifications vary by state.

Another thing you need to do that falls under the “no fun, but necessary” category, that goes along with your will, is to create a living will, or advanced directive. This lets you set the terms for healthcare providers about the kind of health care you want or do not want to receive, in the event that you are unable to speak or make decisions for yourself. The living will sets forth your wishes on resuscitation, quality of life, and end of life treatment. The Durable Power of Attorney for Healthcare is a designated, trusted person who will make medical decisions for you in an emergency situation, in cases where the living will may not provide a clear answer. This person is there to fill in gaps that are not clarified by your living will, and cannot contradict your living will.

3. Obtain or Update Life Insurance

Now is the time to get a life insurance policy, if you do not have one already. Life insurance ensures that your beneficiaries (spouse, children) are financially taken care of if you die.

There are two types of life insurance:

- Term Life Insurance: This type of life insurance offers coverage for a specified period of time. It is less expensive than whole life insurance and has a predetermined guaranteed death benefit. Your premiums will increase at preset time intervals, such as every 10 years.

- Permanent Life Insurance: A number of policies such as whole life, cash value, and universal life, fall under this umbrella. This type of insurance has a death benefit that never expires as long as you pay your premium. In addition, there is typically a saving/investing plan baked in, which is one of the benefits that agents use frequently as a marketing tactic. The rates of return vary, depending on the policy, and they are generally filled with many different kinds of fees. Plus, these policies are often much more expensive than term policies. Because of these issues, the YFP team recommends that most people should keep their savings and investments separate and go for a term life insurance policy.

Once you determine the term (usually 10-30 years) that works best for you, you need to decide the amount of coverage. Financial experts often recommend that your death benefit be 6 to 12 times your annual salary. However, this may not be enough and a number of factors will come into play, including what you can afford, homeownership, and number of dependents. For a more tactical approach, you can check out this calculator.

4. Obtain or Update Disability Insurance

Would you be able to support yourself and your family, pay bills, and achieve your financial goals if you became disabled and couldn’t work anymore? If your answer is no, then you need disability insurance.

Do you know your most valuable asset? Surprisingly, it is not a material possession such as your house, but it is the ability to earn a living. Disability insurance pays a portion of your regular income if you are unable to work for an extended period of time due to illness or injury.

Although it seems unlikely, more than 1 in 4 20-year olds will have a disability for 90 days or more by age 67. Often, people think of worst-case scenarios and assume that they are immune, but something as “minor” as a back injury can put an otherwise healthy person on disability.

There are two types of disability insurance – short-term and long-term coverage. Both replace part of your monthly salary up to a certain amount, such as $10,000, during a disability. Some long-term policies also may pay for additional services, such as training to return to work.

Short-term disability replaces 60-70% of your salary, and pays out for several months up to one year, depending on the policy. It has a shorter waiting period, about 2 weeks, between the time of disability and the time when payments are made to you.

Long-term disability policies typically can replace up to 40-60% of your salary. With long-term disability insurance, benefits end when the disability ends. If the disability continues, benefits end either after a certain number of years or at age of retirement. There is a longer waiting period, usually 90 days, between the time of disability and the time when payments are made

Disability insurance can get pretty complex as there are a number of riders and definitions that vary between companies. Besides your age, occupation, term, benefit amount, and waiting period, these riders will play a huge part in the cost of your policy. To get a better understanding of these and what to expect, you can check out this free guide.

How do you sign up for disability insurance? First, look at your workplace. Often, employers include coverage and contribute towards the premium. Even if your employer does not pay towards your coverage, you can often buy your own coverage through the employer’s insurance broker at a discounted group rate. You can also check with professional pharmacist associations. Another way is to buy an individual plan through a broker or directly through an insurance company. Your Financial Pharmacist offers a helpful service through Policygenius that shops multiple companies to find you the best disability insurance policy.

5. Start or Continue Contributing Toward Retirement

Although retirement may seem far away, and college savings for your children may be at the front of your mind, it is an inevitable event that requires planning. I always remember Suze Orman telling callers on her radio show, “You can take out loans for college but you can’t take out loans for retirement.” The sooner you start saving, the longer your money has to grow. Be sure to contribute to your company’s 401(k) plan, and if your company has a match, try to at least contribute that much since it’s basically free money. The maximum 401(k) contribution limit for 2019 is $19,000 unless you’re over 50 in which you can add an additional $6,000.

Even If your company does not offer a 401(k), or you are self-employed, you can open up an IRA (individual retirement account). For 2019, your total contributions to all of your IRA’s cannot exceed $6,000 if you are under 50 years old, or $7,000 if you are age 50 or older.

Besides an IRA or 401(k), a Health Savings Account (HSA) is another great way to save for retirement as it has triple tax benefits. It lowers your taxable income, grows tax-free, and can be distributed tax-free if used for qualified medical expenses. Despite its name, your contributions do not have to sit in a simple savings account, but can actually be invested aggressively. In order to get access to an HSA, you have to have a high deductible health plan (HDHP).

These financial moves to make with a new baby may not be the most exciting things to do and they can come with a high cost, but they will help you sleep better at night, knowing that you are taking care of your family. Now, here’s to hoping your new bundle of joy sleeps through the night!

Financial planning for a baby, and in general, life events, can be overwhelming. Often it is best to bring in an experienced financial planner to help you plan and prepare. If you are looking for some extra help, you can click here to book a free call with the YFP Planning financial planning team.

Current Student Loan Refinance Offers

[wptb id="15454" not found ]