In Episode 010 of the Your Financial Pharmacist Podcast, we take our very first question on the Ask Tim & Tim segment of the show.

Leighanne from Pennsylvania asks a question about whole life insurance as a strategy for building wealth and saving for college. Here is Leighanne’s question:

What do you think about whole life insurance adding to our financial portfolio as a way to build capital and save for the kids’ college?

Submit Your Question

Now that we have our first episode of the Ask Tim & Tim segment under our belt, we are itching to do some more.

Head on over to www.yourfinancialpharmacist.com and half-way down the home page you will see an ‘Ask Tim & Tim’ section to record your question.

On Episode 009 of the Your Financial Pharmacist Podcast, we launch our very first Debt Free Theme Hour. We interview Carrie Carlton, PharmD to discuss her journey of investing in real estate and how that helped her pay off $135,000 in student loans and be well on her way to achieve financial freedom.

Carrie Carlton, PharmD is a 2011 graduate of the University of Tennessee and currently works in the long-term care setting. Since graduating, she has managed to pay off $135,000 in student loans and acquire 18 rental properties.

Episode 009 Special Giveaway

Two lucky listeners of the Your Financial Pharmacist Podcast will be randomly selected to receive a real estate investing book that comes recommended by today’s guest, Carrie Carlton.

I’m going to get straight to the point with this post. I don’t want this important and potentially game changing message to get lost in any fluff. So, here it is.

You could be making a $1 Million (or maybe even more) mistake and aren’t even aware it is happening.

What?! There aren’t many things you read that can result in you making a small change for some BIG wins…this is one of those.

Whether you are saving for the future in a 401(k), Roth IRA or some other investment vehicle, I’m guessing that with the exception of some financial nerds reading this post, you don’t have a good idea of the ONE THING that is having a significant long term impact on your wealth building success….the fees associated with those investments.

In Tony Robbins’s books Money Master the Game and Unshakeable, he makes a very strong argument for how detrimental these fees can be to your overall financial success. If you haven’t read either of those books, I would suggest doing so as it will get you fired up to take action.

Even if you are not paying a financial advisor to manage your investments, when you account for expense ratios, transaction costs and other types of random fees that you and I aren’t really aware of, many funds (depending on the type of account) have fees that are north of 2%.

Is 2% a big deal? That’s the problem…2% can have a creeping effect that doesn’t make you realize the damage in the short term but will certainly have a significant negative long-term impact.

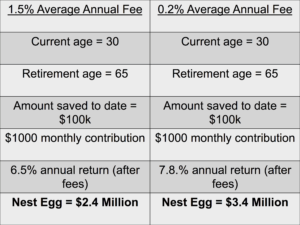

Check out the table below which highlights two different portfolios, one with a 1.5% average annual fee and the other with a 0.2% average annual fee. This calculation assumes the investor is receiving an 8% average annual rate of return less the annual fee.

Did you see the $1 Million mistake?

The investor with the lower-fee portfolio (0.2%) has a nest egg that is worth $1 Million more than the investor with the 1.5% fee portfolio.

Here is the amazing thing…the only difference in this example is the fee!

To compound this mind blowing reality, this difference may even be more for a lot of people reading this blog post over their saving years because their total fees may be even higher than the example used!

All other factors remain constant meaning that you, the investor, can make the same contribution with the same variables yet have a $1 Million greater result by ensuring you are in well-performing, low-fee funds. A Good example is an index fund. These are funds that track a specific market index (such as the S&P 500) rather than try to beat the market.

The following post was written by Tim Church, PharmD, BCACP, CDE. This is third and final post in a series about developing a net worth mindset.

If you haven’t already done so, make sure to check out last week’s episode of the Your Financial Pharmacist Podcast where Tim Baker, CFP and I interview Tim Church to talk about what he learned from going into $200,000 in debt, his work around co-authoring Seven Figure Pharmacist and his advice for pharmacists and pharmacy students on how to develop a millionaire mindset.

A Ramsey Solutions Master Financial Coach, Tim is passionate about helping people with their finances. You can follow him on Twitter @TimChurch85.

In Tony Robbins’s book Money: Master the Game, he describes the amazing story of Theodore Johnson, a UPS worker who never made more than $14,000/year during his career. Despite his meager salary, Johnson never saw this as a setback for achieving wealth.

Remarkably, at the age of 90 he had accumulated over 70 million dollars!

He didn’t accumulate this fortune by winning the lottery or receiving an inheritance. All he did was commit to contributing 20% of his paycheck and every Christmas bonus to his company stock. This enabled him to donate over 36 million to educational causes and set up a scholarship fund for children of UPS employees.

Theodore Johnson had a net worth mindset.

In Part 2 of this series, I discussed how present bias and the need to compare contribute to the phenomenon of lifestyle creep. While these are powerful forces against a net worth mindset, there are some strategies you can put in place to stay focused.

Strategies to maintain a net worth mindset

#1 – Create goals with a strong why.

Having specific, measurable goals with a deadline are important but if you don’t have a strong why behind them, they aren’t very meaningful. Suppose you want to become a millionaire by age 45. Why do you want to achieve that? Do you want the option of retiring early? Do you want to be able travel frequently? Do you want to start a scholarship fund? You may have a net worth goal in mind, but if you can’t determine why, it will be tough to stay motivated to achieve it. Here is a simple template you can use for writing your financial goals:

By <date to achieve goal> I want to <net worth or other financial goal you want to achieve> so that <why you want to achieve the goal>. To accomplish this, I will <steps you will take to make the goal become a reality>.

A hallmark of a net worth mindset is having goals that are bigger than your daily desires. When these are in place you will have ammo against the threats of present bias and comparing yourself to others.

#2 – Break unsupportive habits.

F.M. Alexander said “People do not decide their futures, they decide their habits, and their habits decide their future.”

Most of what we do on a daily basis is on autopilot through habits. This includes how we spend money. If you’re making daily trips for lattes, frequently eating out for lunch, having weekend shopping excursions, or participating in other activities that require spending, you may need break these habits. Check out this short video from Charles Duhigg, bestselling author of the book The Power of Habit, for information on how to break habits.

#3 – Automate contributions toward debt or savings.

You now know that present bias is your biggest threat to becoming wealthy. The longer you have access to money from your paychecks the more likely you are to spend it. Therefore, you need to protect yourself from yourself! The easiest way to do that is make your net worth contributions automatic.

If you want to make sure that a certain percentage of your income is going toward paying off debt or investing, have it automatically deducted from your paycheck or auto-debited from your checking account the same day your paycheck is deposited. This is really a great strategy if you want to allocate “extra” money toward debt that you typically would otherwise have in your hands after covering all of your living expenses.

You can fight lifestyle creep with this strategy by increasing contributions toward debt or savings any time you receive a raise by the same amount. If you never “see” the additional income and continue to have the same net paycheck, you will help fight the temptation of increasing your spending.

Net worth or live-for-today mindset?

If you want to live for today, are comfortable living with debt, and don’t care about securing your financial future, then a net worth mindset is not for you. However, if your goal is to build wealth, then it’s important to analyze how you are spending your money. Having a net worth mindset requires you to make good, consistent financial decisions that support growing your net worth.

Join the YFP Community!

What strategy or strategies can you implement that will help maintain a net worth mindset?

In Part 1 of this series, I discussed the idea of having a net worth mindset and how it can help you be successful with your finances.

Although I portrayed this as a simple philosophy, if you’ve always had a live-for-today type of mindset, it can be a tough transition. In addition, there are barriers and challenges that make it difficult to keep your net worth in focus.

Barriers to a Net Worth Mindset

In Seven Figure Pharmacist: How to Maximize Your Income, Eliminate Debt, and Create Wealth, I wrote about a pharmacist in her 30s named Serena. In 2012, with the help of a side job, she was earning an incredible income of over $140,000 per year, well beyond the national average salary at the time. From the outside it looked like she was doing well financially. She had a nice three bedroom townhouse, drove a newer Mercedes Benz, and was traveling all over the world. However, the reality was that she was broke. She had outstanding student loans, credit card debt, a 401(k) loan, and the value of her home was less than what she owed. Barely able to make all the minimum payments, she suddenly lost her side job, and her home went into foreclosure.

Lifestyle Creep

Parkinson’s Law is a well-known principle that basically says work will expand to fill the available time for completion which is why having deadlines are so important. When applied to personal finance, it translates to: your expenses will rise to the level of your income. In other words, no matter how much money you make, you will spend it.

Many people, like Serena, tend to adjust their lifestyle in step with their income. Instead of putting more money toward savings when income goes up with a raise or additional job, they buy bigger, better things and experiences. That’s why this application of Parkinson’s Law has also been referred to as lifestyle creep.

This is the big reason why many pharmacists, despite making a great income, are living paycheck-to-paycheck. When you’re living like that, it’s very difficult to contribute to your net worth.

There are two big reasons why lifestyle creep occurs: present bias and the need to compare.

#1 – Present Bias

Would you rather buy a $398 Kate Spade Cameron Street Marybeth handbag that you get to have today or put that same amount of money into a Roth IRA that you won’t see again until 30 years from now? (If you don’t like Kate Spade handbags, just substitute it with something you like). Which option is going to bring more happiness today?

By nature, we are very impulsive and make decisions that will make us feel good in the present instead of ones that promote some larger reward in the future, especially with our finances. This phenomenon has been to referred to as hyperbolic discounting or present bias. Although many have the goal to attain financial freedom, their behaviors often don’t align.

Paying off debt or saving money is not going to give you the same feeling you get when you purchase things off Amazon or bite into a burger (fun fact: Tim Ulbrich has never eaten a burger). There’s no dopamine surge when your employer automatically takes money from your paycheck and puts it in a retirement account. That’s why it can be tough to maintain a net worth mindset and why present bias is your biggest threat.

#2 – Comparing Yourself to Others

How many times a day do you get bombarded on social media by people in your network showcasing their exotic trips, new cars, exclusive restaurant outings, or how amazing their life is in general? Does it ever feel like they are trying to do everything bigger and better than you? How does this influence you?

There’s a lot of pressure to maintain a certain image, especially among your network, and many have a desire to impress and announce “I’ve made it!” typically through the demonstration of status symbols or experiences. As a result, people focus on upgrading their lifestyle to match or exceed others instead of their financial future.

This so called “keeping up with the Joneses” mentality, or in today’s society a Kardashian, is associated with the live-for-today mindset and can be very counterproductive to growing your net worth.

If you’re not reaching your goal percentage of income going toward net worth, identifying the barrier in your way is the first and most important step.

In part 3 of this series you will learn some tips and strategies to overcome these barriers.

What barrier(s) is(are) preventing you from increasing your contributions toward your net worth and why is it so tough to overcome?

A Ramsey Solutions Master Financial Coach, Tim is passionate about helping people with their finances. You can follow him on Twitter @TimChurch85. I’m pumped to announce that Tim Church will be joining the Your Financial Pharmacist team! You will be hearing a lot more from Tim on this blog as well as on the podcast and other exciting initiatives we have coming during the second half of 2017 and into 2018.

When I made the commitment to answer yes to one simple question, my financial picture changed and improved dramatically.

I went from feeling frustrated, overwhelmed, and uncertain about my finances to having a sense of relief and clarity. It helped me pay off my car 3 years before the term of the loan was up and has allowed me to live without car payments for over 4 years. It’s what set the stage for my wife and I to pay off $200,000 of student loan debt in only 2.5 years.

Have you ever wondered if you’re on the right track with your finances? While this whole money thing can seem complicated and confusing, the reality is that it’s quite simple. To be successful, you just need to be able to answer yes to one question. If you can answer yes to this one question then you’re on your way to not only achieving financial freedom but also some serious wealth.

Ok enough suspense.

The Question…

Do the majority of your financial decisions promote or grow your net worth?

If you answered yes, then you have a net worth mindset!

Net Worth

People often associate things like income, homes, cars, or clothes with their own or someone else’s financial state. Many pharmacists have the perception that their income alone qualifies them as “doing well” financially. However, income and visible assets only depict part of your financial picture, and unfortunately, in many cases, actually portray an illusion of wealth.

A good indicator of your overall financial health is your net worth, which is defined as:

Total value of your assets (things you own) minus your liabilities (things you owe).

Assets include anything of value such as savings, investment accounts, and real estate. Liabilities include credit card debt, car loans, student loans, or the amount owed on a mortgage.

A Net Worth Mindset

What is the lens through which your decisions with money are made? Is it one that’s completely focused on experiencing instant gratification or one that promotes attaining wealth? Having a net worth mindset means you are keeping your net worth in focus when making most of your financial decisions. It means your financial decisions are either helping you acquire and grow assets or crush debt.

How to Know if You Have This Mindset

On the surface, it may seem subjective whether or not most of your financial decisions are promoting your net worth. Answering yes to these two questions can objectively confirm a net worth mindset:

Is your net worth increasing every year or trending up over time?

Is the percentage of your yearly income spent growing your net worth more than the percentage you spend on nonessential expenses (e.g. clothes, eating out, vacations)?

The first question should be fairly easy to answer with some quick calculations. If you need a little help, Personal Capital is a great app that can help you determine your net worth and determine how it changes over time by consolidating all of your financial information.

You may argue that things you can’t control like the stock or housing market will affect the value of your assets thereby affecting your net worth. While that’s certainly true, more importantly is how much money you are putting toward saving/investing or paying off debt.

Question #2 may seem like an incredibly daunting task to determine. The good news is that you don’t need to go through all your bank transactions to get the answer.

One of the best things my wife and I did to better manage our finances is categorize all of our purchases with the help of the Mint app. By doing this consistently, the app is able to breakdown your spending for any time period. Seeing this breakdown over a month will give you an idea, but looking at a year or multiple years really illuminates your spending habits. From that breakdown you can easily determine the percentage of spending that promotes your net worth. Of note, if you have money that is taken directly from your employer and going to a retirement account such a 401(k) then you would need to add this into the calculation as well.

What a Net Worth Mindset is Not

I’m not suggesting that a net worth mindset means you have to only eat rice or Ramen noodles, shop exclusively at thrift stores, and never go on a vacation your whole life. I’m not suggesting it means you should just hoard money. That would be incredibly depressing and potentially detrimental to your health. Living an enjoyable life where you spend a portion of your money on food and entertainment in addition to your financial future can co-exist with a net worth mindset. That’s why the question asks if the majority not all of your financial decisions promote your net worth.

Based on how I described a net worth mindset, you could argue that it’s best to focus entirely on building assets (placing less emphasis on debt elimination). Although that’s one strategy, I truly believe getting rid of non-mortgage debt as quickly as possible is the fastest way to free up money and build wealth. Always remember that paying off debt will effectively increase your net worth.

In Part 2 of this series on net worth, you will learn the common barriers to having and maintaining a net worth mindset.

In the meantime, answer the following question by commenting below:

What is the one thing you can do that will help promote a net worth mindset?

The following post was written by Nate Hedrick, PharmD., a 2013 graduate of Ohio Northern University. By day, he works as a clinical pharmacist for the sales team at Medical Mutual. By night, he works with pharmacist investors in Cleveland, Ohio – buying, flipping, selling, and renting homes as a licensed real estate agent with Berkshire Hathaway. This experience has led to the creation of YFP’s Real Estate Concierge Services, a one-stop shop for getting you on the right track toward buying or selling your next home.

My wife and I met on a blind date in pharmacy school. We were set up by a mutual friend and despite an impending snowstorm and an exam I really should have been studying for, we went out to our local Mexican restaurant and had a fantastic time. We were crazy for going out in that blizzard and my transcripts can attest to the fact that I should have spent more time studying. Despite the risks, we made it home in one piece, I passed that exam (with a C), and I ended up meeting my best friend that night.

We made that date work despite nature and other obligations working against us.

Now, over 7 years later, we are blessed with two darling baby girls, a goofy dog, a wonderful home… and a mountain of debt.

Pharmacy school is expensive. So are homes. (So are dogs and kids come to think of it.) Looking back, our blind date is actually a great analogy for our early financial life together. We bought our first home pretty much the same way we handled our first date. We were jumping in with both feet regardless of other obligations. I had just finished residency, our friends and family owned homes, and we were tired of the “temporary feeling” we had from renting. We were driving out into that blizzard despite what the weather report said.

I certainly don’t regret our first date and I love the home my daughters get to grow up in, I just now realize that there was probably more we could have done to set ourselves up for success in both cases.

Just like we could have waited an extra night for better weather and would have still gotten married years later, we could have waited a little longer for our finances to get in order and still would have ended up with a great place to live. Hopefully, some of what I learned can help you whether you are about to buy your first home or your forever home.

#1 – The bank does not set your budget.

A pre-approval letter from the bank is not the same thing as how much house you can afford.

As pharmacists, we are lucky to make great salaries right out of school. However, this is a double-edged sword that often fools us into thinking we can take on a lot more debt than we probably should. When a bank calculates how you get pre-approved for, they use the “28/36 rule” for conventional financing. This means that no more than 28% of your gross income may go to your total housing expenses. Furthermore, no more than 36% of your gross income may go to all your debts. Using these numbers with a pharmacist’s salary will often result in a pre-approval that could have you looking outside your range. Check out the calculator below to estimate your monthly payment based on your projected loan and other costs.

Mortgage Calculator

While there are many ways you calculate your own home-buying budget, I recommend considering the “50/30/20 rule”. The idea is that 50% of your TAKE HOME income should go to your needs, 30% to your wants, and 20% to savings.

Needs are things like food, clothing, transportation, medical needs, student loans, mortgage (or rent), insurance, and property taxes. Wants include entertainment, vacations, charitable donations, and any extra you want to throw at your student loans or other debt. Savings include traditional savings accounts, extra retirement contributions, and wherever you stash your emergency fund.

Remember, this is take-home pay, which really should be what you bring in after taxes and after maxing out your 401k match through your employer. I like the 50/30/20 calculation because it is specific enough to illustrate what you can really afford but flexible enough to allow you to adjust certain things based on your individual needs. Regardless of the method you use, calculate the number for yourself instead of allowing your lender to fool you into looking for a house you really can’t afford.

#2 – Shop around for mortgage lenders.

When I was looking for a bank to get a home loan for our first house I had no idea where to begin. I ended up just asking my parents which bank they used for their mortgage and went with that. It seemed like too daunting of a task to tackle otherwise.

Despite the numerous choices, I encourage you to meet with at least 3 different lenders or utilize a mortgage broker when finding your first mortgage. Find someone who is comfortable with the loan product you intend to use (FHA, conventional, VA, USDA, etc.) and compare what other incentives or advantages they provide if you decide to use them as your loan servicer. If you aren’t sure what the differences or advantages are between the different types of loans, check out my website www.RealEstateRPH.com for an article that walk through each type.

You can go to multiple banks or individual lenders online but this requires you to submit documents multiple times and could take significant time and effort. Plus, the moment you provide your information, it’s often sold to third parties and then you get bombarded with annoying phone calls, text messages, and emails by multiple companies. Fortunately, there is a faster and easier way to compare rates and that’s why we partnered with Credible.

Not only do they have an outstanding user-friendly platform that lets you compare mortgage lenders within minutes, but you deal with them directly until the final stages of the process.

It can be extremely tempting to skip saving up a significant down payment for your first house. With loan products available that allow 3.5% down, why would anyone want to save up a full 20%?

While there are a number of reasons, the primary financial concern comes down to private mortgage insurance or PMI. Essentially PMI is insurance that protects the lender against individuals who default on their loan. The problem is that this monthly payment effectively buys you as the homeowner nothing but ends up costing you $100 per month or more. Luckily, this requirement is removed once you have reached 80% loan-to-value.

What the lender often neglects to tell you is that unless you submit a request at that 20% they can actually continue your PMI requirement up until your reach 78% loan-to-value. Although it might not seem like much, this 2% difference could equate to hundreds of dollars! If you do decide to put only 5% or 10% down, make sure you are paying attention for when you reach the 20% mark and are aware of the process your lender requires for waving PMI on time.

#4 – Don’t forget the hidden costs of buying a home.

Aside from saving enough for a down payment, you need to have some cash reserves set aside for all the little things that come with buying a home. Once you put an offer in, your first major expenses will typically be inspections. General home, pest, radon, sewer line, and other inspections are all important in making sure the home you are buying doesn’t have any major issues. Depending on which inspections you choose to have, you can expect to pay a few hundred to about $1,000.

Closing costs typically run between 2% and 4% of the cost of the loan. That means for a $200,000 house you need to have an extra $6,000 or so available on top of your down payment. The lender is required to give you a detailed breakdown of exactly what your closing costs will be before everything is due. The good news is, many times the closing costs can be negotiated into the purchase offer and actually paid by the seller. Your real estate agent can help with this. Property taxes, home insurance, and PMI (if you have to pay it) are often taken out monthly by your lender and put into an escrow account. This ensures the lender that these important payments are received each month and are on time.

Lastly, if your heater goes out in the middle of winter, you don’t have a maintenance department you can call like you do with a rental. Setting aside some additional funds for these unexpected costs is why an emergency fund is so important. Don’t drain your savings account with your down payment and forget to keep something in reserve for the unexpected.

#5 – Prepare for a lot of “hurry up and wait”.

If you are going to be getting any kind of loan for your new house, prepare yourself for the uncomfortable month that is underwriting. I understand it from the bank’s point-of-view, there is some serious legwork to be done when giving someone tens or even hundred of thousands of dollars. However, I have yet to experience a closing that didn’t involve some mix of “We need this document from X and Y in 24 hours or the whole deal is going to fall through.” Promptly followed by days of utter silence. It can certainly be nerve racking. My advice is to simply be prepared for it and don’t try to squeeze your closing date into a smaller time period than is advised by your Real estate agent or lender. Also, be as diligent as possible when it comes to document collection. Create a new folder on your computer for all your loan documents to live in during the underwriting process and gather all your financial information in that one space.

#6 – Don’t skip out on the home warranty.

I distinctly remember the moment during our negotiations that my wife and I told our Real estate agent we didn’t need a home warranty. The house we bought had just been redone and we were certain the appliances were new. I lived in that certainty for about 4 months before I had no way to wash my dirty laundry. Several hundred dollars later we had a working washing machine and a heap of regret. The average home warranty costs between $300 and $600. The average cost of a new washer is $700. The average cost of a new furnace is $4,000. Each of these (along with several other household appliances) are covered under most home warranties. A small price to pay for a lot of peace of mind. This is especially true when you consider that you can often negotiate for the seller to cover the home warranty for you.

#7 – Work with a real estate agent – its free! (sort of).

Being a real estate agent myself, I admit I might be slightly biased. However, even before I became licensed, I realized the advantages of working with a good real estate agent. For starters they have access to a lot more information than Zillow® or Realtor.com®. These websites work well for the initial home screening process but when it comes time to look seriously for a home, you need a more powerful tool. Each agent has access to a database of housing information specific to your area called the multiple listing service (MLS). Think of it like Lexi-Comp® compared to webMD®.

The best part is that they can give you limited access to this database for yourself if you simply ask. Through the MLS portal, your real estate agent can set up automatic searches that deliver updated listings directly to your inbox as soon as new information becomes available. Once you find a property you are interested in, your agent should help you set up showings, put in offers, negotiate with the seller, and generally help you navigate the complex buying process.

When it comes to contracts and offers, I also recommend finding an agent comfortable with DotLoop®. This online tool allows all the important documents to be drafted, signed, and delivered online. The convenience of being able to submit a signed offer from your pharmacy’s break room is hard to beat.

Finally, the best part is that all this help provided by a real estate agent is effectively FREE if you are a first time homebuyer. The commission for real estate transactions is generally paid by the seller and then split between the listing agent and your agent. This means you usually only pay a small office fee of a few hundred dollars to get the whole deal done! Not a bad price to pay for personalized service.

Finding an agent like I described above can be a challenging prospect. That’s why we’ve created our FREE Real Estate Concierge Services! Here’s how it works: Head on over to our real estate page and click on buy or sell a home. There, you can sign up for a free 30-minute callwith Nate. During that call, we’ll start by learning about your budget, wishes, and goals. Then Nate will connect you with one of our preferred local agents from a network of personally interviewed and vetted top-tier agents. This gives you a local expert to help you on your way. Throughout the whole process Nate will stick by your side, even after closing, in case you have any questions or need an extra opinion along the way. It’s as simple as that! Head on over to our Real Estate page and get started today!

#8 – Home ownership provides tax advantages, even for people that make “too much”.

Not many people would expect there to be disadvantages to making a six-figure salary right out of school. If there is a downside however, it has to be income tax and a significant lack of tax breaks. Even the meager deduction that is student loan interest is lost if you make more than $85,000 per year ($170,000 if married and filing jointly).

Luckily, real estate remains a refuge for limiting your taxable income. Since interest payments can be the largest component of your mortgage payment in the early years of owning a home, the biggest deduction for many people is mortgage interest. There is even an extra point-based deduction you can take the first year you buy your home. For example, if you paid two points (2%) to close on a $200,000 mortgage ($4,000), you can deduct the points as long as you put at least $4,000 of your own cash into the deal. And believe it or not, you get to deduct the points even if you convinced the seller to pay them for you as part of the deal.

Finally, you can also deduct local property taxes you pay each year.

All these combined deductions can add up to quite a lot come tax day. This advantage can even be taken several steps further when you talk about real estate investing and home depreciation, a complicated topic that is worth reading up on.

#9 – Plan to stay for a few years.

The real financial advantage to buying a home comes from slowly building equity by staying there for several years. Although it’s not always easy to predict where you are going to be in a few years (geographically and in life) try to make a five-year plan when deciding how and where you want to live. If you don’t want to be tied to a particular location, perhaps renting is a better idea. If you and your spouse want to have a large family, pick a location (and the number of bedrooms) that supports your plan for a few years down the road. Again, all of this is easier said than done.

My wife and I bought a home with three bedrooms thinking we could grow into them once we started a family. That plan started to fall apart when both of us ended up working from home. Just two years after buying out home we found ourselves with a master bedroom, a nursery, an office…and one of us at the kitchen table. Flexibility is really the answer if your original plan has to be scrapped. Eventually we worked out an extra office space in the basement and now my wife only works at home a few days per week. My advice is to have a plan, then be able to roll with the punches if and when things change.

#10 – Consider “House Hacking”.

How would you like to buy a home, live privately in your favorite part, and have someone else pay your mortgage for you? If this sounds to good to be true, I encourage you to start reading up on the concept of house hacking. The basic concept is to buy a home with 2-4 units, live in one of them and rent out the others. Ideally, these are long-term tenants that consistently pay you enough rent to cover all or most of your housing expenses.

The real beauty of house hacking becomes apparent when you learn that the bank treats the loan for a 4-unit home in the same way they treat a single-family residence. This means a single mortgage buys you not only your first home but also your first investment property. There are also easier ways to house hack if being a landlord isn’t your cup of tea. Renting out your extra bedrooms, transforming your basement into a rentable guesthouse, or even Airbnb are all simple ways to lower your house payments by having others pay your mortgage for you. No matter how you do it, if you don’t mind living with a guest or two, house hacking can be an incredible way to make your first home more affordable. To learn more about house hacking, check out Episode 130 with Craig Curelop, the Finance Guy for BiggerPockets and author of The House Hacking Strategy.

Ready to buy your own home?

Click HERE to access our Real Estate Concierge Services!